Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

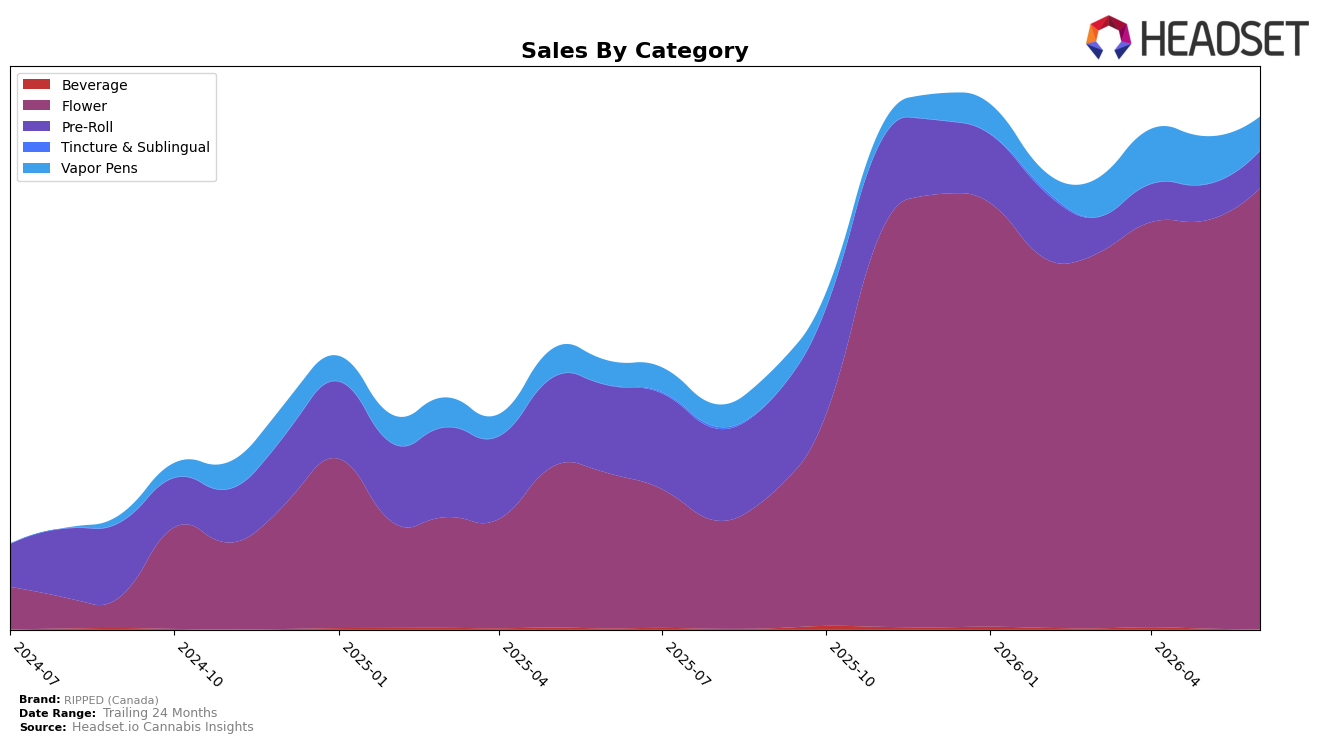

RIPPED (Canada) concentrated 86.21% of June 2026 sales in Flower, with category sales up 184.86% year over year and 8.16% month over month, while Pre-Roll fell 57.87% YoY but inched up 3.80% MoM to 7.20% share. Vapor Pens held 6.59% share with 40.05% YoY growth but dropped 29.61% MoM, and June 2026 average price rose 126.21% YoY to $31.34 alongside Flower’s higher average price of 45.13. The pattern implies a deliberate tilt toward higher-priced Flower driving overall June 2026 growth, while Pre-Roll’s multi-quarter contraction and Vapor Pens’ sharp MoM pullback suggest de-emphasis outside the core.

Within Flower, a June 2026 rank of 22 in New York places the brand below the lead pack, and the 8.16% MoM Flower growth versus a 29.61% MoM decline in Vapor Pens indicates a prioritization that risks single-category exposure. The 91.31% overall sales growth YoY alongside a 126.21% YoY jump in average price implies mix-led and pricing-led expansion concentrated in one category, which positions RIPPED (Canada) as a premium-leaning Flower specialist whose near-term gains depend on sustaining share above 86% while stabilizing sub-7% Pre-Roll and sub-7% Vapor Pens to avoid volatility.

Competitive Landscape

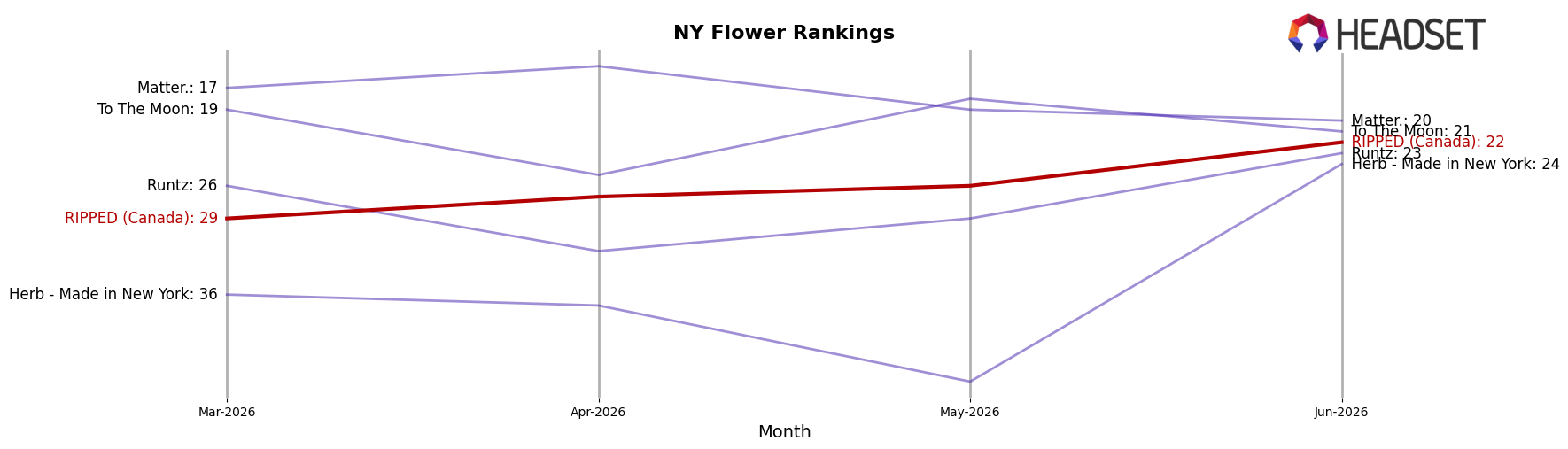

RIPPED (Canada) sits at rank #22 in New York Flower for June 2026, improving 7 positions from #29 in March 2026 while remaining 3 spots below its peak at #19 from November 2025; this upward shift coincides with category leaders tightening their grip, as Find. climbed to #1 with a 3-rank YoY gain and RYTHM moved up 10 ranks to #5, whereas Dank. By Definition slid despite holding #3 amid a -50.7% YoY sales change. Against this backdrop, Leal advanced 7 ranks to #2 with a 44.4% YoY sales increase while Rolling Green Cannabis holds #4 with a 2-rank YoY improvement and a -7.1% YoY sales change, indicating that RIPPED (Canada)’s recent climb is recovery-driven rather than leadership-displacing and implies a trajectory toward the teens is plausible but requires share capture from faster-advancing top-5 incumbents.

Notable Products

Indica Pre-Roll (1g) posted the largest shift with a 76.1% month-over-month gain to rank 4 in June 2026, while the prior leader Rolls Pre-Roll 3-Pack (1.5g) fell 19.0% but still held rank 1, indicating volatility at the format level rather than a wholesale category exit. Sativa Blend (3.5g) surged 58.4% to rank 3 as Sour x Papaya Milled (7g) declined 20.8% at rank 5, and four of the top ten are Flower SKUs despite three Flower entries dropping between 9.2% and 17.1%, implying a bifurcation where value or blend-led Flower gains offset weakness in legacy milled or infused lines. Blue Imagination Milled (7g) grew 8.7% at rank 2 while White Widow Infused Ready To Roll (14g) slipped 15.9% to rank 10, suggesting June 2026 demand concentrated in lighter weight or non-infused options even as heavier 14g formats retained presence via rank positions 8–10. The pattern implies RIPPED (Canada) is tilting toward accessible formats and lighter Flower packs that deliver faster velocity, with Pre-Roll momentum acting as a hedge against softness in larger infused Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.