Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

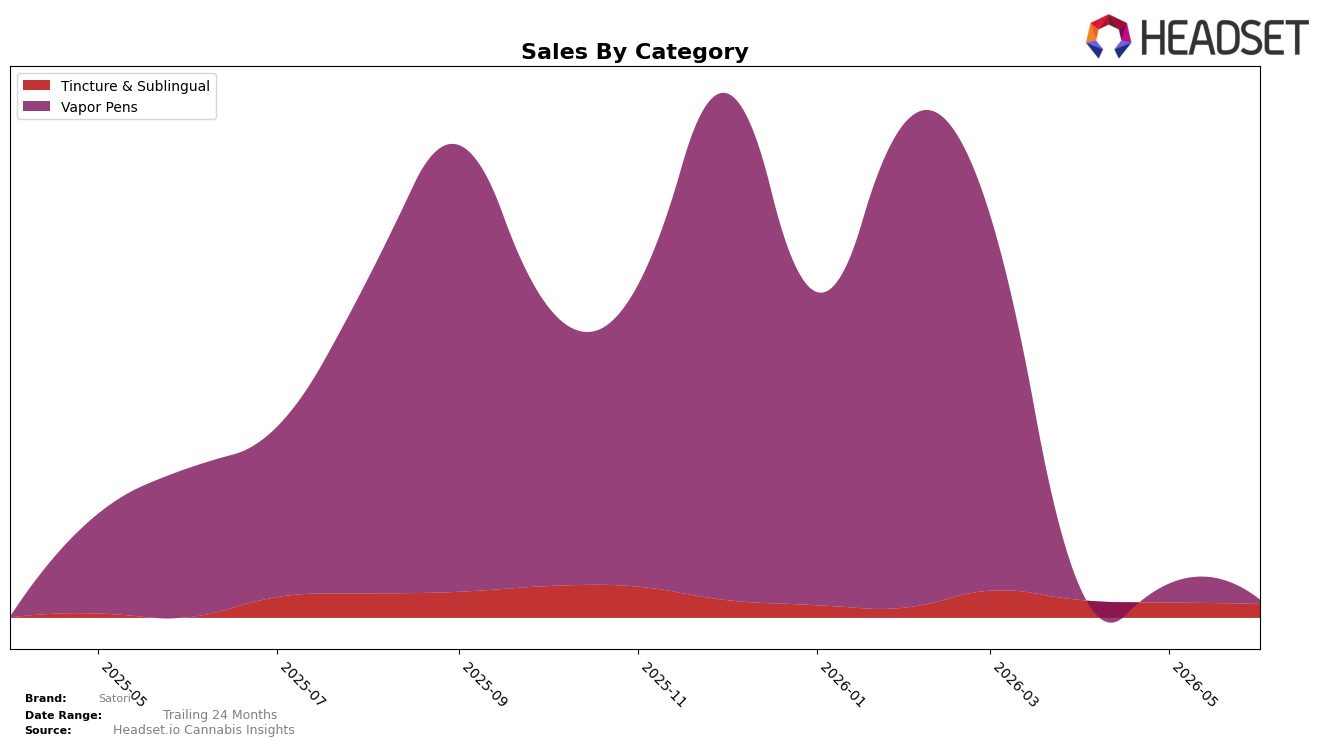

Satori’s category mix in June 2026 is concentrated in Tincture & Sublingual at 68.14% share alongside Vapor Pens at 31.86% share, with year-over-year divergence: Tincture & Sublingual up 264.70% YoY while Vapor Pens fell 94.45% YoY. Month over month, Tincture & Sublingual declined 7.01% and Vapor Pens dropped 63.28%, and the average price rose 27.04% YoY to $63.85. The pattern implies a pivot from Vapor Pens toward higher-priced Tincture & Sublingual where unit velocity likely compresses but revenue mix concentrates, with New York exposure orienting the brand toward medical-adjacent formats rather than inhalables.

The shift toward Tincture & Sublingual at 68.14% share alongside a 94.45% YoY decline in Vapor Pens positions Satori closer to a niche wellness use case than mainstream inhalable demand, despite a 63.28% MoM contraction in pens that usually anchor trial. With overall brand sales down 83.14% YoY and category average prices split at $70.01 for Tincture & Sublingual versus $53.74 for Vapor Pens, the mix now favors higher ticket but slower-turn items, which can depress rank visibility in New York Vapor Pens where rank data are absent. The implication is a defensive posture: protect margins via Tincture & Sublingual pricing while accepting reduced shelf momentum in Vapor Pens, requiring channel tactics that treat pens as awareness drivers rather than volume core.

Competitive Landscape

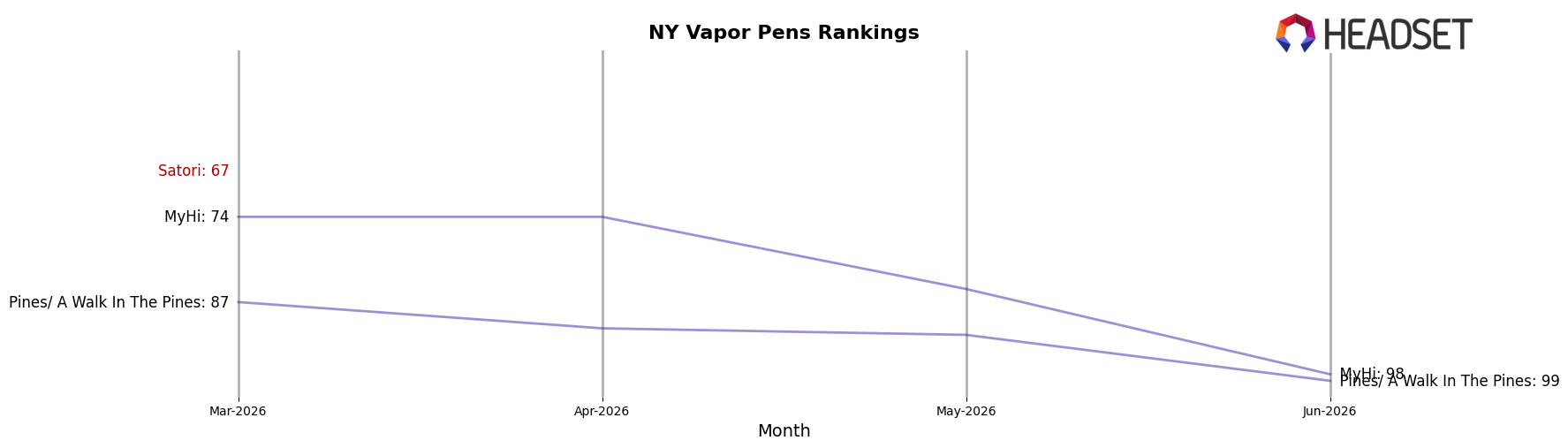

Satori sits at rank #180 in June 2026, down 96 positions year over year from #84, and 113 positions below its recent peak rank of #53 in February 2026; versus three months ago, the drop from #67 to #180 adds a 113-rank slide within the quarter, indicating accelerated share loss. In the same period, Jaunty held rank #1 despite a -18.1% year-over-year sales change, while Jetty Extracts moved from approximately rank #23 a year ago to #5 with a 238.2% sales increase, signaling that the growth engine has shifted toward faster-scaling rivals. The pattern implies Satori’s trajectory is one of declining competitive relevance in New York Vapor Pens unless its rank stabilizes or reverses amid leaders consolidating at #1–#5 and mid-pack challengers accelerating.

Notable Products

Berry Delight Rosin Disposable (0.5g) posted the steepest decline in June 2026 at -68% MoM, sliding to rank 3, while Strawberry Candy Live Rosin Disposable (0.5g) fell -64% MoM to rank 2, indicating that Vapor Pens momentum compressed sharply at the very top of the list. THC Water Soluble Enhancer Elixir Tincture (600mg) held rank 1 with a -7% MoM dip and approximately $3,237 in sales, and with four of the top five SKUs in June 2026 being Vapor Pens, the category still concentrates share even as individual pen SKUs retrench. The pattern implies Satori is overexposed to volatile pen formats, suggesting a pivot toward the steadier Tincture & Sublingual leader could stabilize the mix.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.