Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

New York Honey (NY Honey) is stocked at 162 licensed dispensaries across New York, with the deepest coverage in New York, Rochester, Queens, Schenectady, and Albany. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

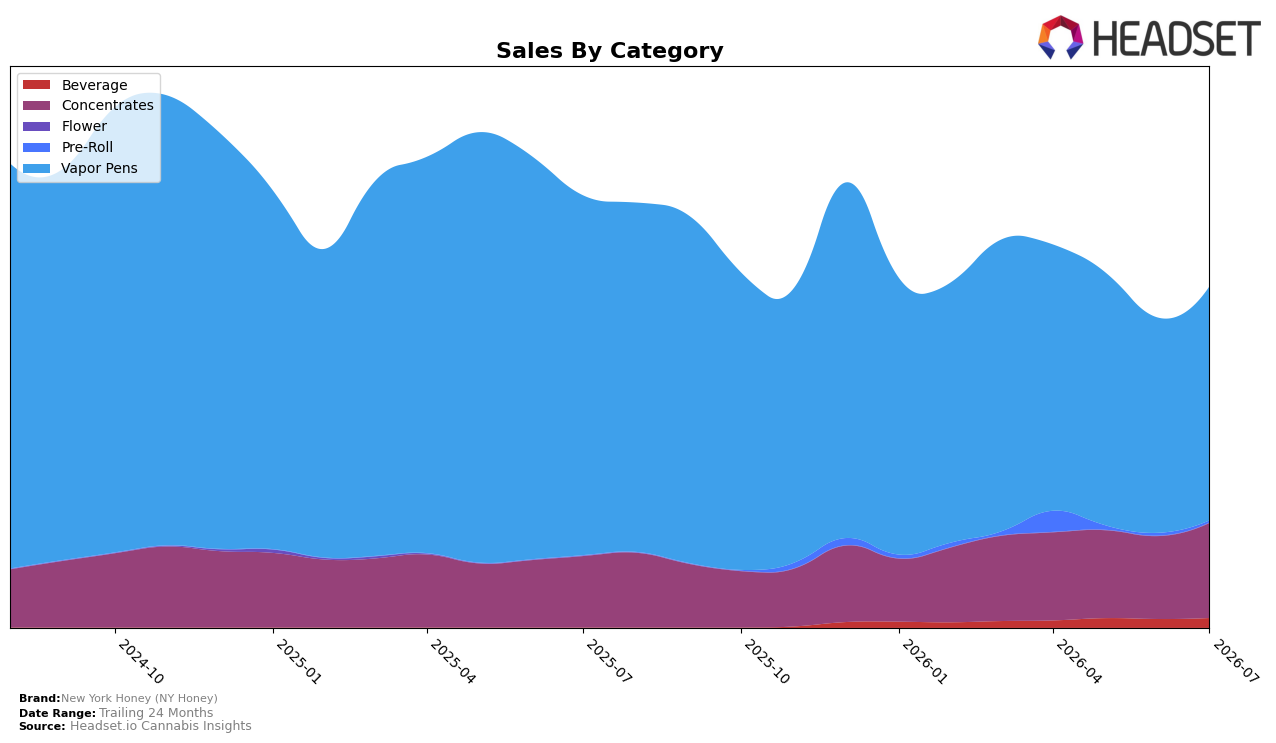

New York Honey (NY Honey) concentrated 68.83% of July 2026 sales in Vapor Pens while Concentrates accounted for 27.88%, a mix that widened away from Pre-Roll at 0.50% and Beverage at 2.79%. Vapor Pens declined 35.00% year over year but rose 8.75% month over month, whereas Concentrates expanded 33.24% year over year and 14.71% month over month, pulling the average price down 15.87% year over year to $36.14. Beverage added 11.63% month over month without a reported year-over-year base, and Pre-Roll fell 28.89% month over month with no year-over-year benchmark; combined, these shifts left overall brand sales down 21.15% year over year despite July 2026 momentum in two core formats. The pattern implies a pivot toward higher-growth Concentrates alongside a stabilization in Vapor Pens, with the brand’s statewide Vapor Pens rank at 24 in New York setting a ceiling that Concentrates growth can offset if the current month-over-month trajectory holds.

The divergence between a 33.24% year-over-year gain in Concentrates and a 35.00% year-over-year decline in Vapor Pens, combined with respective month-over-month gains of 14.71% and 8.75%, implies that New York Honey (NY Honey) is migrating volume toward formats with faster unit velocity at slightly higher average prices. With Vapor Pens still at 68.83% share and ranked 24 in New York, the brand’s immediate positioning hinges on leveraging Concentrates’ 27.88% share to backfill the Vapor Pens year-over-year drag while the 11.63% Beverage lift and 28.89% Pre-Roll dip remain too small at 2.79% and 0.50% share, respectively, to move total performance. This mix indicates a near-term strategy centered on price-sensitive recovery in Vapor Pens and incremental share capture in Concentrates, aiming to counter the 21.15% brand sales decline and reposition the portfolio toward categories with current month-over-month tailwinds.

Competitive Landscape

New York Honey (NY Honey) sits at rank 24 in July 2026, sliding 10 positions year over year from rank 14, and down 3 places versus April 2026 when it was rank 21; the brand’s prior peak at rank 11 in May 2025 contrasts with this two-step decline pattern that includes both a -10 YoY rank change and a -3 quarter-on-quarter rank change. In the same July 2026 period, Fernway rose from rank 3 to rank 1 with a 46.8% YoY sales increase, while Jetty Extracts jumped from rank 22 to rank 4 on 199.3% YoY sales growth, indicating competitor mobility upward as NY Honey moves from the low teens into the mid-20s; this divergence implies that without a reversal in share capture, NY Honey’s trajectory points to further rank pressure as faster-advancing rivals widen the gap.

Notable Products

Apple Berry Distillate Disposable (2g) posted the steepest movement in July 2026 with a -12.9% month-over-month drop while sitting at rank 9, contrasting with Mimosa Distillate Cartridge (1g) up 27.5% at rank 3 and Blueberry Muffin Distillate Disposable (1g) up 30.9% at rank 6. Blue Dream Distillate Cartridge (1g) held rank 1 with +13.3% MoM and Barry White Distillate Cartridge (1g) was rank 2 with +14.1% MoM, while Golden Ticket Distillate Disposable (1g) slid -7.6% at rank 4 and Strawberry Cough Distillate Cartridge (1g) fell -8.1% at rank 5. Vapor Pens account for eight of the top ten, but the split trajectory—three cartridges gaining double digits while two disposables decline and one 2g disposable drops -12.9% despite $35,066 in sales—indicates format sensitivity within the same category. The pattern implies New York Honey (NY Honey) is consolidating leadership around 1g cartridges while larger 2g disposables require pricing or flavor resets to avoid ceding share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.