Market Insights Snapshot

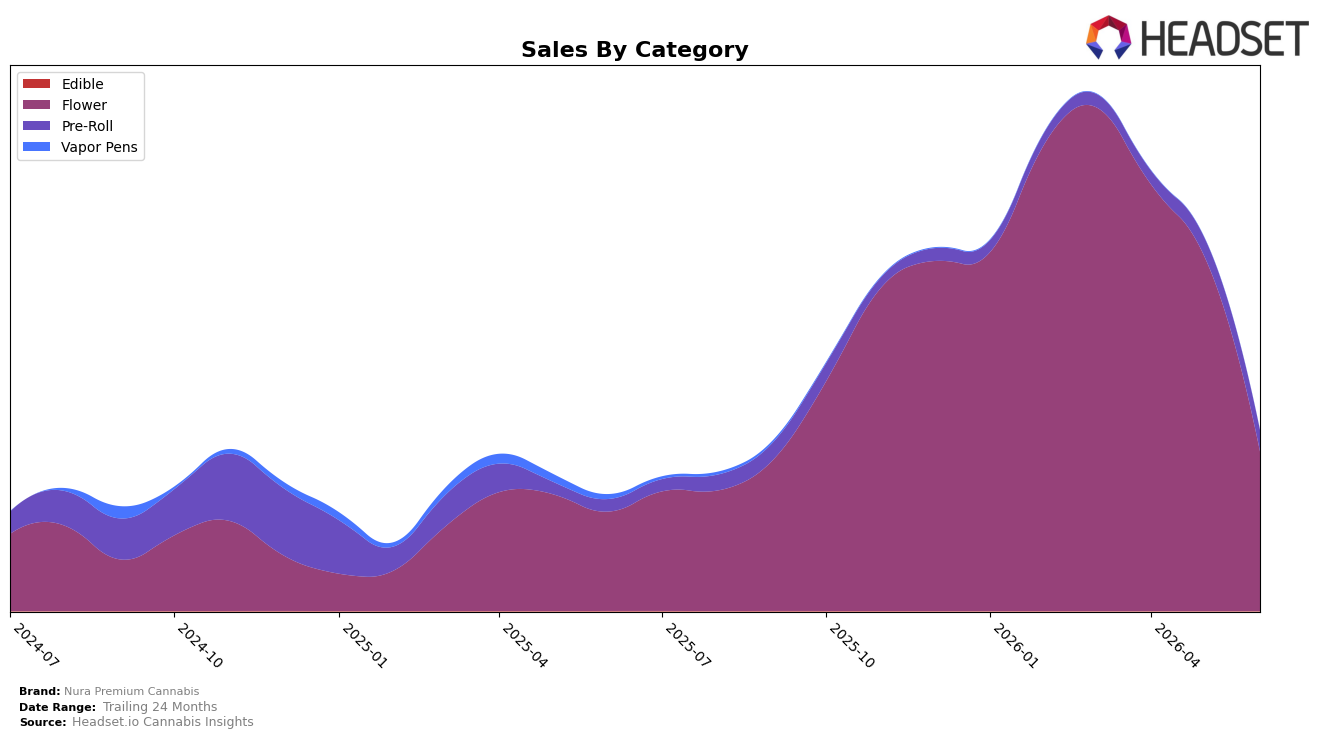

In June 2026, Nura Premium Cannabis concentrated 88.32% of sales in Flower and 11.68% in Pre-Roll, with Flower up 60.94% year over year but down 55.00% month over month, while Pre-Roll rose 73.86% year over year and 13.72% month over month. Average price rose 31.78% year over year to $15.48, with Flower priced at a premium average of 21.43 and Pre-Roll at 5.00, and overall brand sales advanced 55.90% year over year alongside a 24‑month lift of 66.69%. In Michigan Flower, the brand held rank 28, and the mix’s month-over-month whiplash—Flower contracting 55.00% while Pre-Roll expanded 13.72%—implies a demand shift where heavier reliance on Flower magnifies volatility that Pre-Roll is partially offsetting.

The sharp month-over-month contraction in a category with 88.32% share combined with a 31.78% year-over-year price increase suggests price-led revenue support but exposure to volume swings, while a 13.72% MoM gain in an 11.68% share Pre-Roll points to a stabilizer that could cushion rank pressure at position 28 in Michigan Flower. With Flower’s 60.94% YoY growth still driving the 55.90% brand YoY lift but producing a 55.00% MoM pullback, the pattern implies the brand’s positioning leans into premium-priced Flower for scale and uses Pre-Roll momentum for near-term resilience, indicating that incremental mix shift toward Pre-Roll could moderate rank volatility without abandoning Flower-led identity.

Competitive Landscape

Nura Premium Cannabis sits at rank #28 in MI Flower in June 2026 after a YoY climb of 26 positions from #54, yet it has fallen 24 spots from March 2026 when it peaked at #4, indicating volatility across the spring-to-summer window. In contrast, High Minded held #1 both YoY and in June 2026 despite a -13.7% sales YoY change, while Goodlyfe Farms advanced from #5 to #2 on +44.1% sales YoY, suggesting that top-tier share is consolidating even as leaders post mixed growth. The shift from #4 in March 2026 to #28 in June 2026, alongside a YoY rank improvement of 26 places, implies a rebound story that lacks month-to-month persistence, pointing to a brand that can break into the top five but has not yet converted that spike into sustained competitive position.

Notable Products

Blue Biscotti (Bulk) posted the steepest decline at -77.7% month over month while holding rank 5, and Pure Detroit Runtz (Bulk) fell -20.1% at rank 3. Donkey Butter (3.5g) dropped -42.6% at rank 4, and G13 (Bulk) slid -42.7% at rank 6. With eight of the top ten being Flower SKUs and several posting declines over -40%, the mix implies Nura Premium Cannabis is overexposed to bulk and eighth Flower volatility in June 2026 and may need to rebalance toward steadier formats.

Spyder Mon OG Infused Pre-Roll (1.1g) led the lineup at rank 1 with $28,203, contrasting with Grape Pie Gelato (Bulk) at rank 10 down -44.1% month over month. Black Cherry Gelato (Bulk) at rank 2 and Blue Gushers (Bulk) at rank 7 lacked reported month-over-month changes, while Ice Cream Cake (Bulk) at rank 8 also had no MoM figure. The pattern suggests leadership is concentrated in a single Infused Pre-Roll while Flower spans ranks 2 through 10, pointing to a strategy shift toward premium pre-rolls to counter Flower drawdowns.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.