Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Oceana Gardens is stocked at 84 licensed dispensaries across Michigan, with the deepest coverage in Detroit, New Buffalo, Ann Arbor, Adrian, and Bay City. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

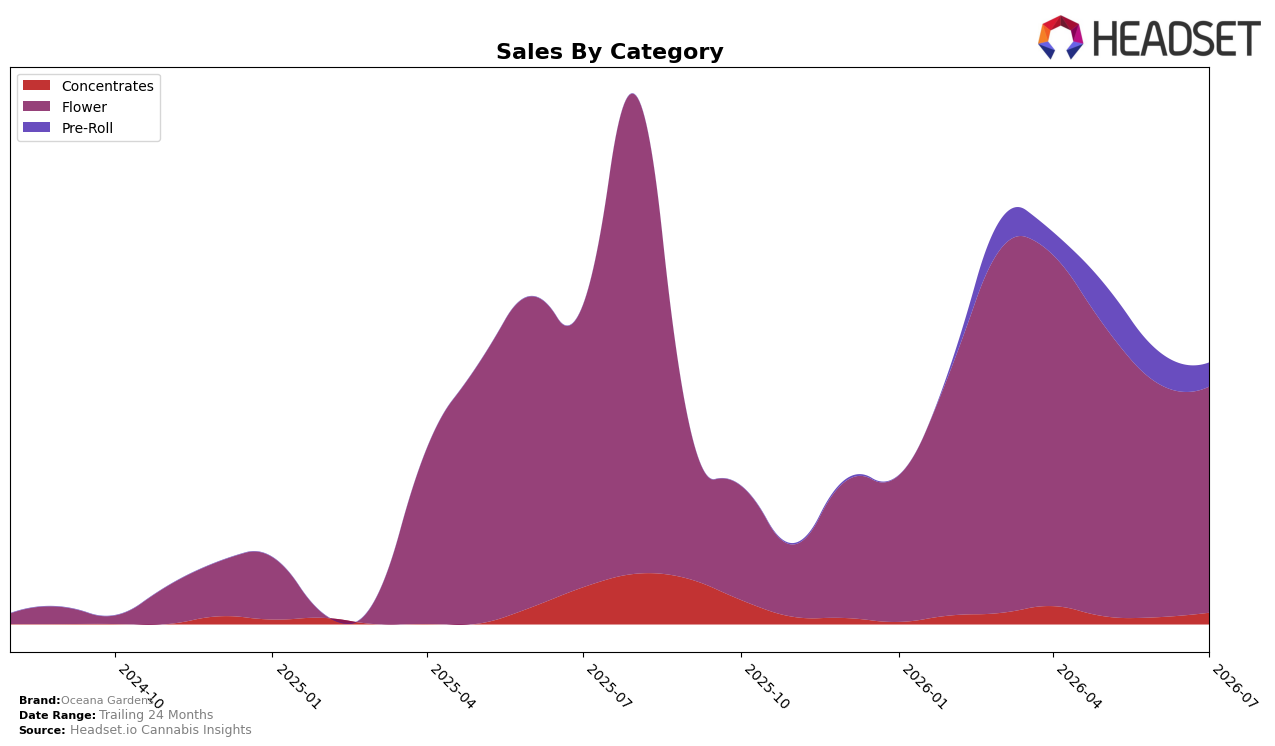

Oceana Gardens in July 2026 concentrated 86.54% of sales in Flower, down with a -19.94% year over year change and a -3.39% month over month pullback, while Pre-Roll held 9.12% share with a -26.47% month over month decline and Concentrates at 4.34% share swung +65.48% month over month despite a -69.21% year over year drop. The brand’s Flower position in Michigan ranked 43 in the category, and average price fell -19.27% year over year as overall brand sales declined -18.16% year over year, implying a mix still anchored in Flower but with volatility at the edges that is reshaping both price expectations and category exposure.

The contrasting moves—Concentrates surging +65.48% month over month off a -69.21% year over year base and Pre-Roll retreating -26.47% month over month while Flower slips -3.39% month over month—imply a tactical pivot opportunity toward higher-velocity niches without abandoning the 86.54% Flower core. With rank 43 in Michigan Flower and a -19.27% year over year price reduction alongside a -18.16% year over year sales decline, the pattern suggests price-led defense in Flower combined with selective Concentrates expansion could improve positioning by capturing incremental share where month over month momentum is positive while mitigating exposure where month over month softness is pronounced.

Competitive Landscape

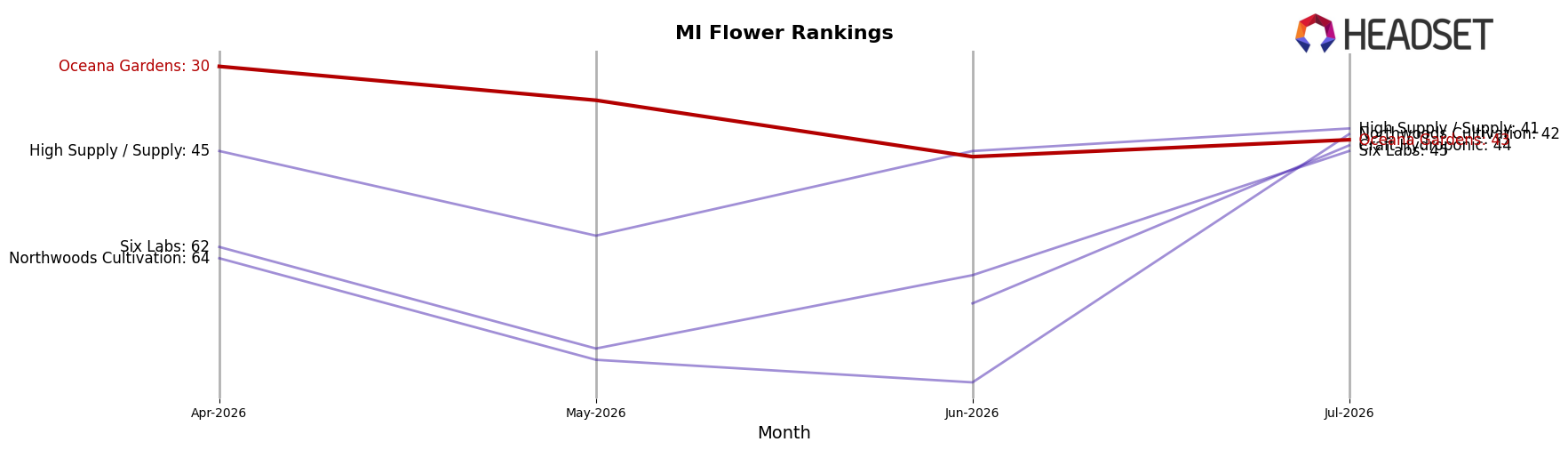

Oceana Gardens sits at rank #43 in MI Flower in July 2026, down 3 spots year over year from #40 and 13 spots from April 2026 when it was #30, while its best position was #23 in August 2025; in contrast, Goodlyfe Farms moved up from #5 to #3 as sales grew 36.8% and Mischief climbed from #10 to #4 with 59.4% YoY sales growth, whereas Pro Gro slipped from #3 to #5 as sales fell 12.0% and category leader High Minded held #1 despite a 12.5% YoY sales decline; this pattern implies Oceana Gardens is being outpaced by faster-growing mid-pack risers and needs a catalyst to reverse a downward rank trajectory that has extended from April 2026 to July 2026.

Notable Products

Hella Jelly Pre-Roll (1g) surged 71% month over month to rank 1, while Apple Pie Pre-Roll (1g) fell 52% and Chicken N' Waffles Pre-Roll (1g) declined 49%, consolidating leadership at the very top and compressing the middle of the lineup. Four of the top ten are Pre-Roll SKUs, yet three of those posted double-digit drops between 14% and 52%, indicating mix volatility even as the category anchors visibility at ranks 1 through 5.

Bigfoot Glue Pre-Roll (1g) slid 19% to rank 2, contrasting with Bigfoot Glue (28g) in Flower, which inched up 3.8% at rank 9, suggesting consumer trade-up toward larger Flower formats despite Pre-Roll softness. Donutz (Bulk) in Flower declined 10% at rank 8, but the presence of two Orange Cream Pop Flower sizes inside the top ten alongside a steady $58,671 Bigfoot Glue (28g) indicates Flower depth counterbalancing Pre-Roll swings; taken together, the product mix points to a pivot toward larger-pack Flower as the steadier volume engine while a single breakout Pre-Roll carries headline momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.