May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

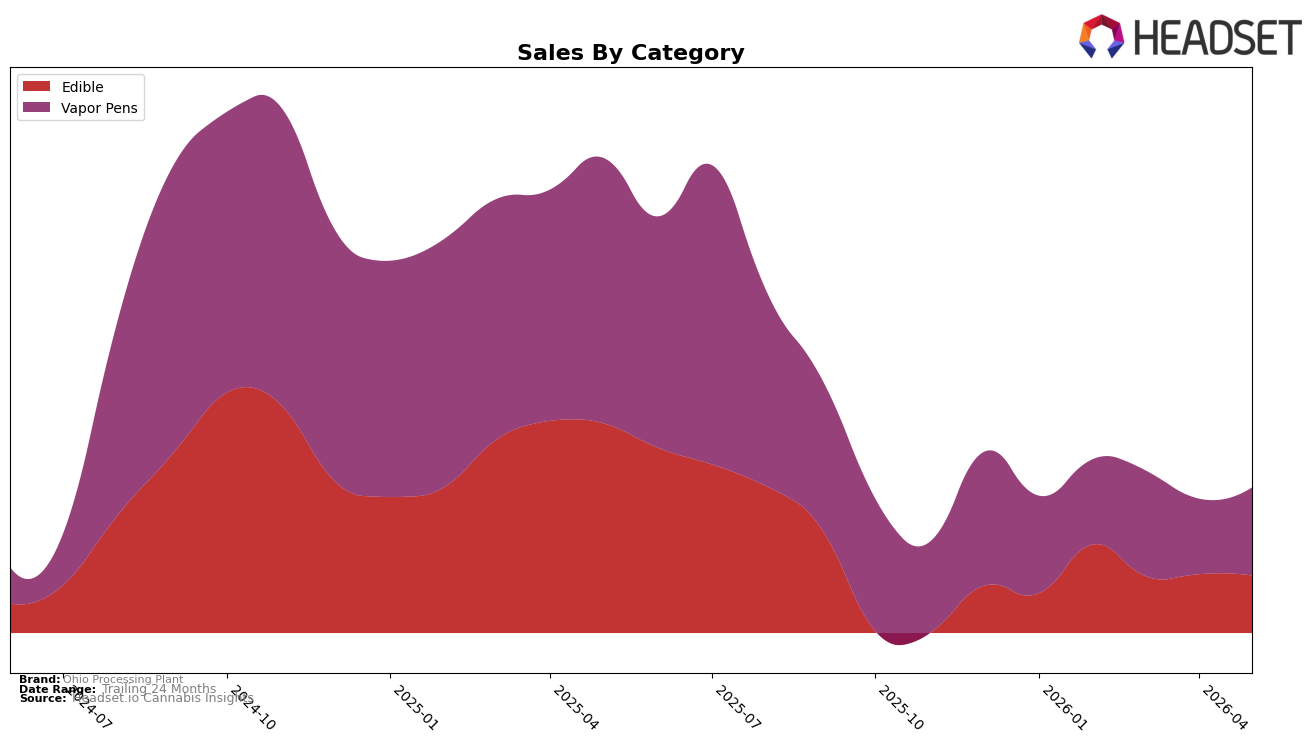

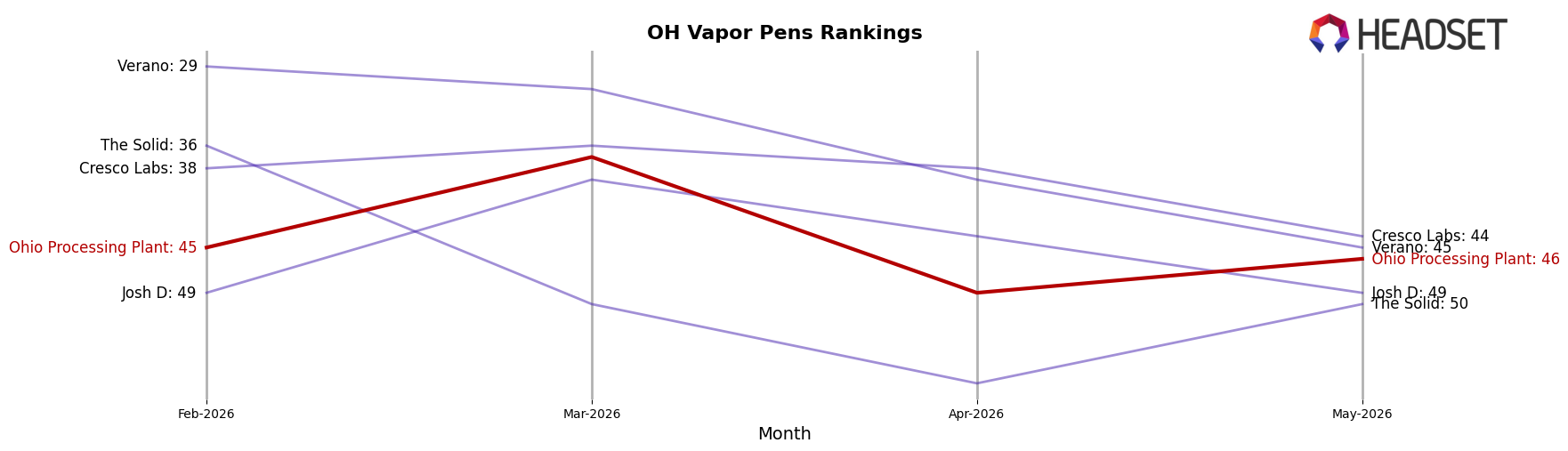

In May 2026, Ohio Processing Plant concentrated 60.55% of sales in Vapor Pens and 39.45% in Edible, with Vapor Pens up 16.47% month over month while Edible slipped 2.14% month over month. Year over year, both categories contracted, with Vapor Pens down 66.87% and Edible down 72.68%, aligning with a brand-level sales decline of 69.43% even as average price fell 15.79% year over year. Within Ohio Vapor Pens, the brand held rank 46, indicating mid-to-lower shelf presence relative to the state set. The mix tilt toward Vapor Pens alongside category-divergent MoM trends implies a short-term pivot to pen-led volume recapture while Edible drag continues to cap total recovery.

The 21-point gap between Vapor Pens’ MoM growth (+16.47%) and Edible’s MoM decline (−2.14%), combined with a 5.81-point YoY outperformance of Vapor Pens versus Edible (−66.87% vs. −72.68%), signals a defensive concentration in faster-rebounding inhalables despite a rank of 46 in Ohio Vapor Pens. With an average price at $19.49 and category prices diverging (Vapor Pens at $24.39 vs. Edible at $14.89), mix is skewing toward higher-ticket units to offset volume erosion, yet category-wide YoY compression suggests price cuts alone are insufficient to regain prior scale. This pattern implies near-term share protection via Vapor Pens focus while Edible requires format or pack-size repositioning to avoid further mix dilution.

Competitive Landscape

Ohio Processing Plant sits at rank #46 in May 2026, down 25 positions year over year from #21, and 1 place lower than February 2026’s #45, while still far from its February 2025 peak at #18; in contrast, Certified (Certified Cultivators) rose to #1 from #2 with a 51.9% YoY sales increase and Rove advanced to #4 from #12 on 106.5% YoY growth, indicating Ohio Processing Plant’s relative share is being displaced as faster-rising rivals gain rank and visibility; the implication is a prolonged slide in competitive position unless mix, pricing, or distribution shifts re-accelerate velocity from a #46 base despite category leaders consolidating up to 8 ranks faster.

Notable Products

Blueberry Gummies 11-Pack (220mg) posted the largest month-over-month gain at +58.2% to rank 4 in May 2026, outpacing Buper Soof Distillate Disposable (1g) at +55.9% in rank 3 and Red Raspberry Gummies 10-Pack (100mg) at +54.3% in rank 5. Mixed Berry Gummies 10-Pack (100mg) was the steepest decliner at -14.6% while holding rank 2, creating a split within the Edible lineup where three SKUs rose more than +50% as one fell by double digits. Vapor Pens concentrated the leaderboard with four of the top ten, including the rank-1 Cosmic Zing Flexcell Distillate Disposable (1g), but Edibles supplied the outsized percentage swings, with Pink Lemonade Gummies 10-Pack (100mg) also up +55.8% in rank 7. The mix implies Ohio Processing Plant is benefiting from surging Edible demand to complement a rank-led Vapor Pens franchise, pointing to balanced growth that can buffer volatility within individual SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.