Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Natty Rems is stocked at 215 licensed dispensaries across Colorado, with the deepest coverage in Denver, Colorado Springs, Boulder, Longmont, and Aurora. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

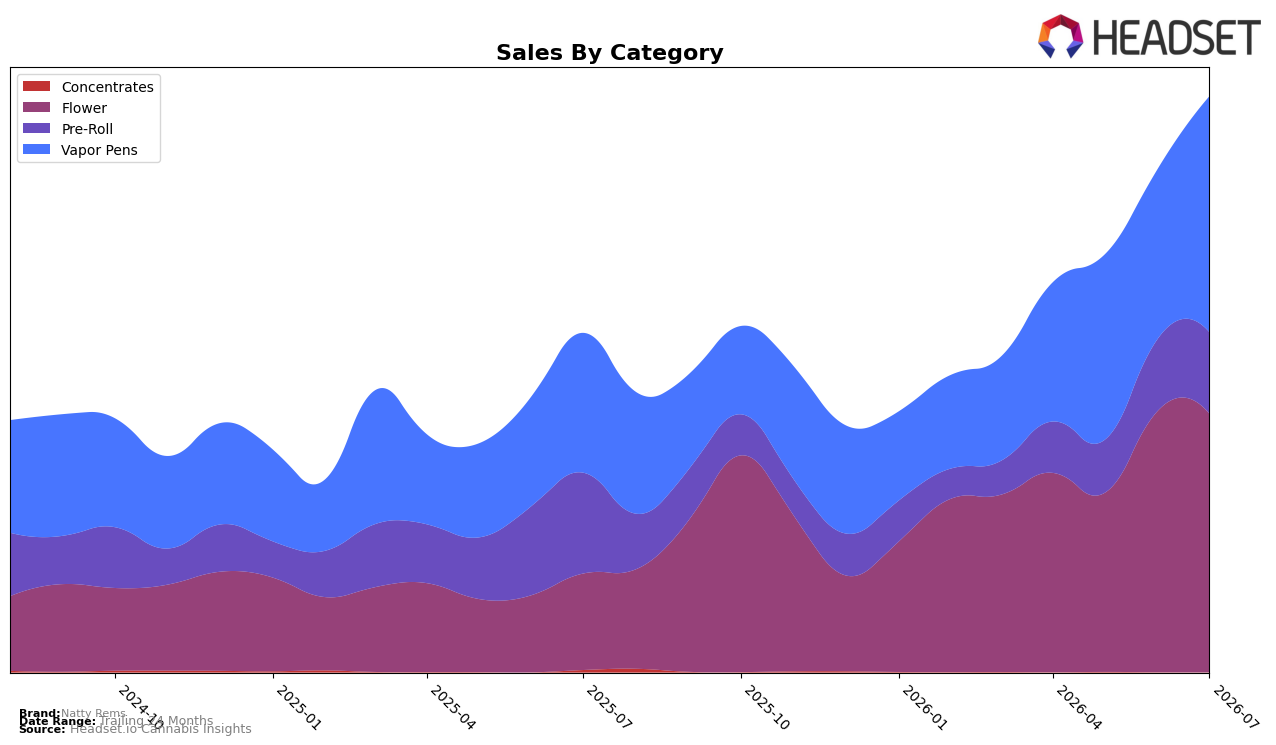

In July 2026, Natty Rems concentrated 44.90% of sales in Flower and 40.98% in Vapor Pens, with Pre-Roll at 14.12%, indicating a two-category core that now accounts for 85.88% of mix. Flower surged 168.50% year over year but slipped 1.15% month over month, while Vapor Pens advanced 68.96% year over year and jumped 38.90% month over month; Pre-Roll declined 19.23% year over year yet grew 12.98% month over month. With average price up 13.36% year over year to $11.20 alongside a Flower average price of $8.48 and Vapor Pens at $33.35, the mix shift broadens ticket size without over-reliance on price. The pattern implies a pivot toward a dual-engine portfolio where Vapor Pens supplies near-term momentum and Flower anchors volume, positioning Natty Rems to manage volatility in Pre-Roll without diluting overall growth.

Holding a rank of 5 in Flower in Colorado alongside a 44.90% mix share in that category signals defensible shelf presence, while the 38.90% month-over-month climb in Vapor Pens suggests incremental share capture potential against higher-priced formats without abandoning Flower’s scale. A 69.88% brand sales year-over-year increase coupled with a 1.15% month-over-month dip in Flower and a 12.98% month-over-month rise in Pre-Roll indicates the brand can rotate demand between inhalable formats to stabilize aggregate growth. The implication is that Natty Rems is shifting from single-category dependence toward a balanced positioning where rank in Flower supports credibility and Vapor Pens growth provides runway for premium-per-unit expansion.

Competitive Landscape

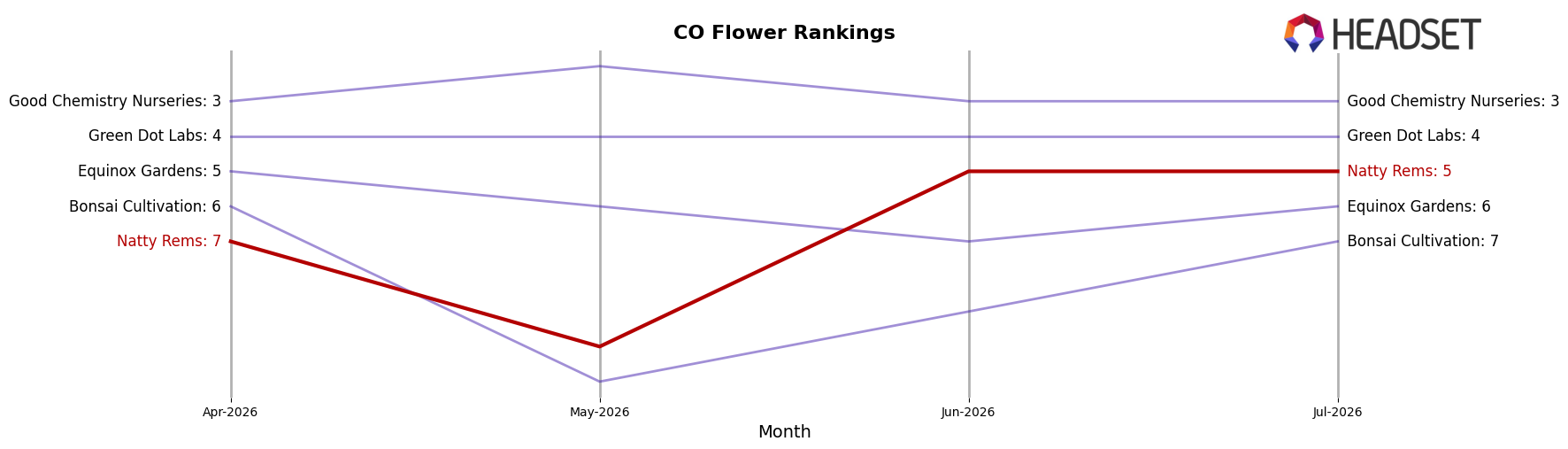

Natty Rems sits at rank #5 in July 2026, a 18-position climb from #23 year over year, and a 2-spot improvement from #7 in April 2026; this places the brand at its peak rank of #5 in July 2026 and narrows the gap to Green Dot Labs at #4, while Seed & Strain Cannabis Co. moved up from #2 to #1 and Good Chemistry Nurseries slipped from #1 to #3 with a -8.7% sales change; the rank ascent alongside a competitor’s decline implies Natty Rems is converting share from legacy leaders and is positioned to contest a top-3 slot if momentum from April 2026 to July 2026 persists.

Notable Products

Golden Goat (Bulk) led the month with a -20.3% month-over-month decline while still holding rank 1, and Jungle Cake (Bulk) slipped a milder -3.8% at rank 9, indicating volume concentration at the top even as the lead SKU contracted; with Flower occupying eight of the top ten ranks, the category mix remains heavily weighted toward bulk formats. Garlic Apples (Bulk) climbed +42.1% to rank 4 while Vader (Bulk) advanced +31.6% at rank 10, contrasting the Golden Goat (Bulk) retreat and pointing to intra-portfolio substitution within Flower. The absence of a reported MoM change for Golden Goat (3.5g) at rank 2 alongside a $96,737 tally for Golden Goat (Bulk) suggests pricing-tier bifurcation between bulk and packaged formats. Overall, the pattern implies Natty Rems is tilting toward a diversified Flower portfolio where gains in secondary bulk SKUs offset flagship volatility, reinforcing a strategy of depth over single-SKU dependence.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.