Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Pacific & Pine is stocked at 66 licensed dispensaries across Washington, with the deepest coverage in Seattle, Spokane, Tacoma, Des Moines, and Kelso. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

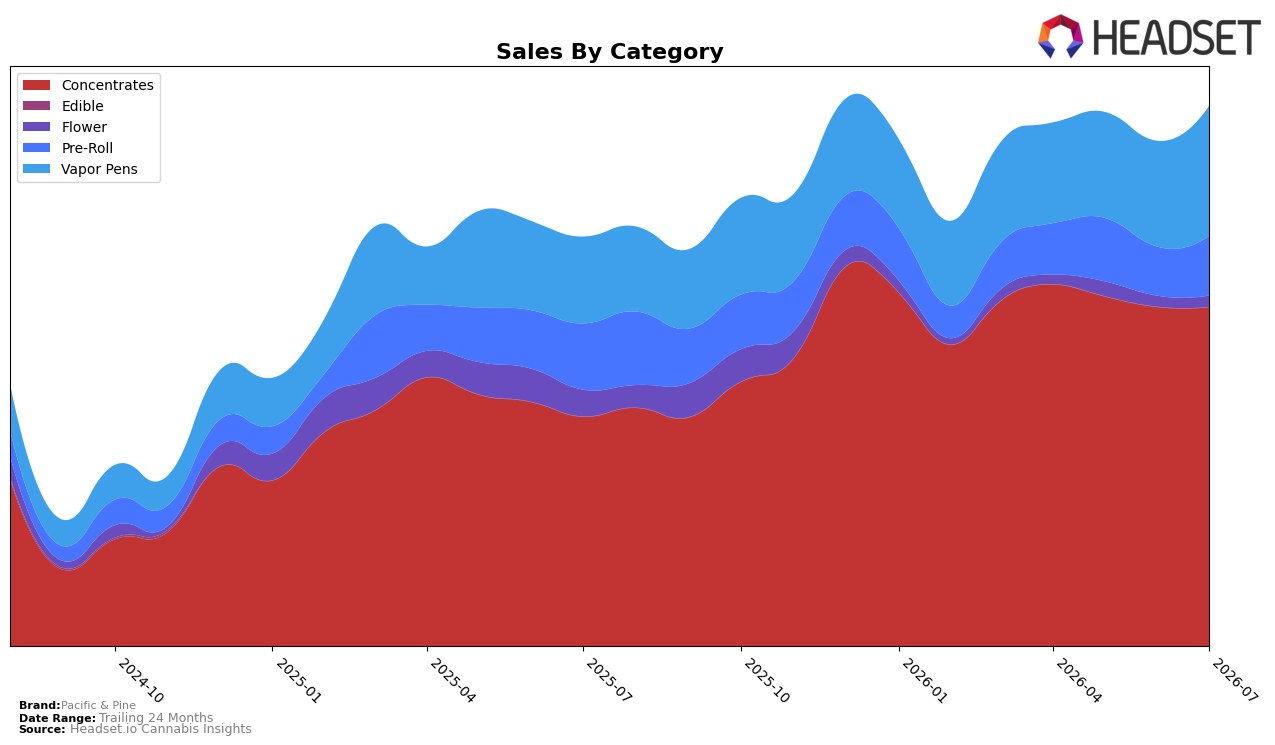

Pacific & Pine concentrated 62.86% of July 2026 sales in Concentrates with year-over-year growth of 47.88% but a month-over-month dip of 2.61%, while Vapor Pens held 24.11% share with 49.90% YoY growth and a 22.94% MoM lift; Pre-Roll at 10.99% share declined 10.04% YoY yet climbed 21.60% MoM, and Flower at 2.04% share fell 58.46% YoY with a 2.84% MoM uptick. The brand ranked 9 in Concentrates in Washington and lifted average price 5.42% YoY to $17.08, indicating a mix-led price effect as higher-priced Concentrates at $19.04 and Vapor Pens at $18.72 expand while lower-priced Pre-Roll at $9.37 retrenches; the thesis is that share consolidation in higher-value inhalables is offsetting softness in legacy Flower and pressuring breadth for Pre-Roll.

With Concentrates sliding 2.61% MoM while Vapor Pens surged 22.94% MoM and Pre-Roll rose 21.60% MoM, the month’s growth engine shifted toward faster-turn inhalables, and holding rank 9 in Washington Concentrates alongside a 47.88% YoY lift there implies room to trade up within the tier while defending mix against categories with 10.04% and 58.46% YoY declines. The implication is that Pacific & Pine’s pricing power (+5.42% YoY) can be sustained if Vapor Pens continues to take incremental share from 24.11% while Concentrates maintains a top-10 footprint at 62.86% share, but the strategy requires pruning low-velocity Flower at 2.04% share and selectively rebuilding Pre-Roll where the 21.60% MoM suggests promotional elasticity rather than structural recovery.

Competitive Landscape

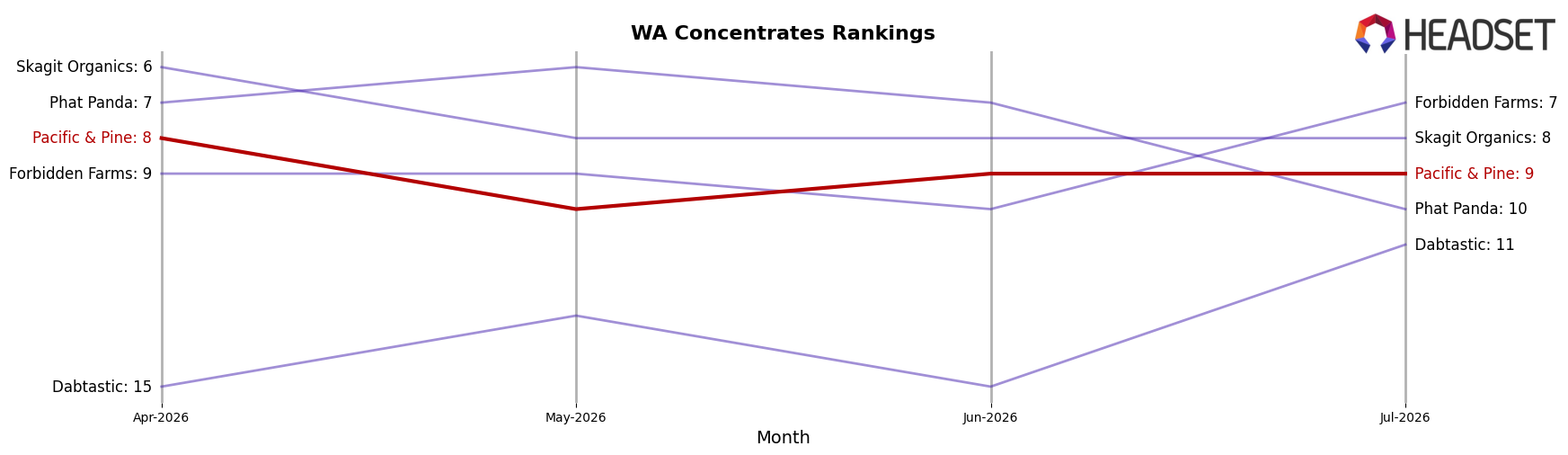

Pacific & Pine is currently ranked #9 in WA Concentrates, up 9 positions year over year from #18, but down 1 rank from #8 in April 2026 to #9 in July 2026, indicating a near-peak pullback since its April 2026 peak rank of #8 and a 1-position slide from #8 three months ago to #9 now; meanwhile, Dabstract moved from #4 to #3 with a 5.16% sales YoY change while Pacific & Pine ceded one spot quarter-over-quarter, and Constellation Cannabis advanced from #7 to #4 with 18.93% YoY sales growth as Pacific & Pine stalled below the top 8, which implies that Pacific & Pine’s rank trajectory is improving year over year but drifting month to month as faster-climbing rivals compress the path back into the top 8.

Notable Products

Purple Pineapple Live Hash Rosin (1g) posted the steepest decline at -40.3% MoM while holding rank 8, whereas Tahoe Cure Live Rosin (1g) delivered the largest gain at +65.4% and climbed to rank 5; this divergence implies shoppers are rotating within the lineup rather than expanding the category. Blueberry Diesel Solventless Live Hash Rosin (1g) stayed at rank 1 with a -2.1% MoM dip as Super Boof Solventless Hash Cold Cured Rosin (1g) advanced +28.4% at rank 2, indicating leadership is stable but the runner-up is compressing the gap on momentum. Nine of the top ten are Concentrates SKUs, and the single raw dollar anchor at $17,537 for Super Boof confirms that mix lift is concentrated in solventless formats rather than spread across forms. The product mix points to Pacific & Pine leaning into solventless differentiation and flavor churn to defend top ranks while pruning underperforming strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.