Where to Buy

Packs Cannabis (MO) is stocked at 78 licensed dispensaries across Missouri, with the deepest coverage in KCMO, St. Louis, Columbia, Joplin, and Springfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

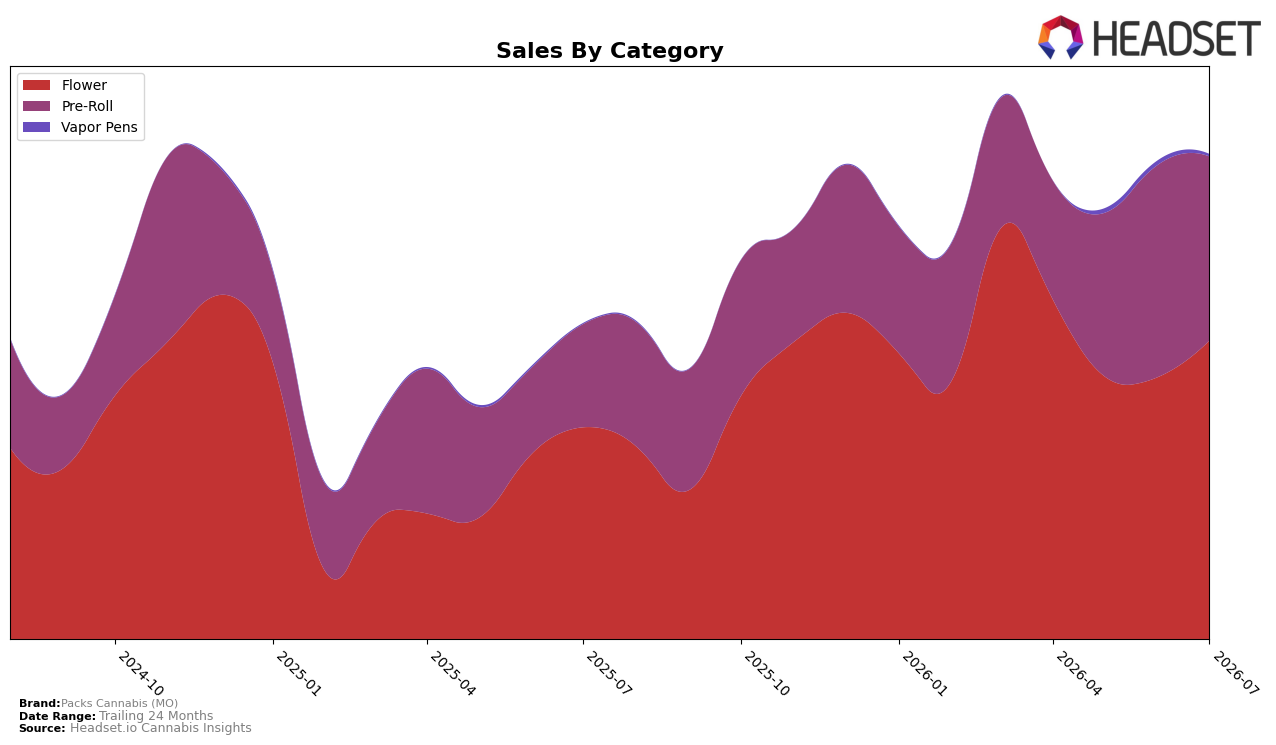

In July 2026, Packs Cannabis (MO) concentrated 61.58% of sales in Flower with year-over-year growth of 41.05% and month-over-month growth of 13.96%, while Pre-Roll held 37.97% share with a higher year-over-year gain of 78.68% but a month-over-month decline of 13.30%. Vapor Pens remained a fringe contributor at 0.44% share, spiking 177.84% year over year but falling 49.65% month over month. The brand’s overall sales grew 53.68% year over year alongside an 11.15% decline in average price, and its July Flower rank in Missouri was 23. The pattern implies a deliberate tilt toward volume: price compression paired with double-digit Flower growth and a pullback in Pre-Roll momentum suggests the mix is stabilizing around Flower scale rather than chasing edge categories.

The shift toward Flower—up 13.96% month over month versus a 13.30% month-over-month drop in Pre-Roll—signals a repositioning around mid-priced core items, with the 11.15% average price decline widening the accessible base while protecting July 2026 rank 23 in Missouri Flower. Despite Vapor Pens’ 177.84% year-over-year surge, its 0.44% share and 49.65% month-over-month contraction indicate limited strategic weight relative to the 61.58% Flower and 37.97% Pre-Roll split. The implication is that Packs Cannabis (MO) is prioritizing share defense in Flower through pricing and distribution depth, using Pre-Roll as a growth lever year over year but accepting month-over-month volatility to maintain throughput in the primary category.

Competitive Landscape

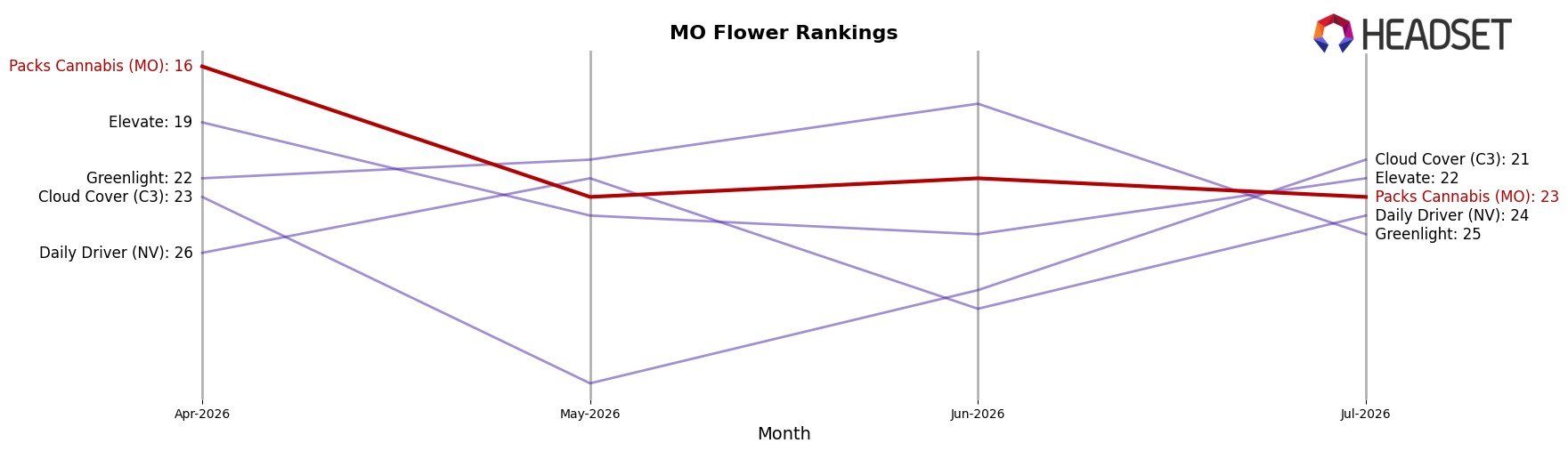

Packs Cannabis (MO) sits at rank #23 in Missouri Flower for July 2026, a 1-place improvement from rank #24 year over year, yet down 7 positions from rank #16 in April 2026 and off its March 2026 peak of #13; meanwhile, Flora Farms held #1 with a 0-place YoY change despite a -1.3% YoY sales shift, and Sinse Cannabis advanced from #4 to #2 alongside roughly +9.0% YoY sales growth, indicating Packs Cannabis (MO) is stabilizing year over year but ceding mid-tier ground quarter to date while top players consolidate or climb.

Notable Products

California Zkittlez Pre-Roll 2-Pack (1g) marked the steepest movement with a -4.0% month-over-month change while holding rank 5, contrasted by Kush Breath Pre-Roll 2-Pack (1g) up 21.9% at rank 9. Mai Tai Pre-Roll 2-Pack (1g) rose 14.9% at rank 6, and the concentration is clear with nine of the top ten SKUs in Pre-Roll while the lone Flower item, California Raisins #2 Smalls (7g), sits at rank 10 with $91,040 in July 2026. The pattern implies Packs Cannabis (MO) is consolidating around Pre-Roll velocity, using modest MoM gains at ranks 6 and 9 to offset a mid-pack dip at rank 5 and signaling a mix tilted toward quick-turn, lower-weight formats over bulk Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.