Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

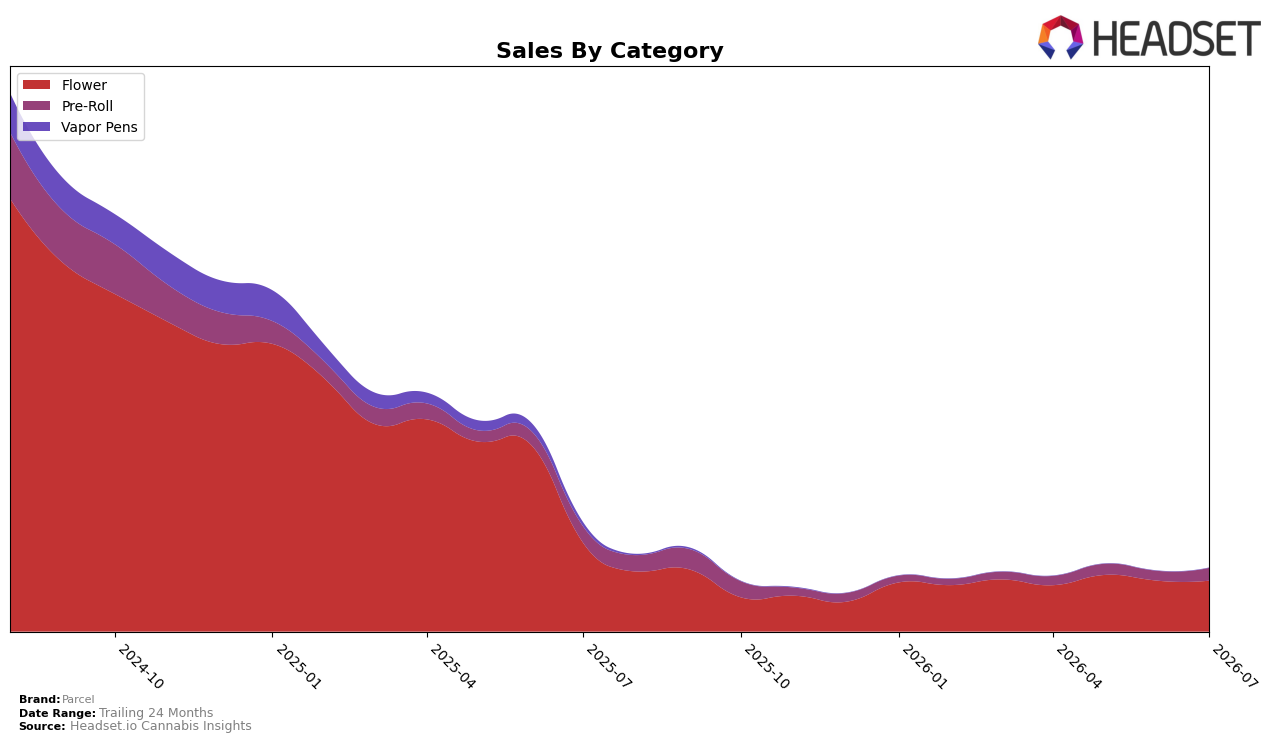

In July 2026, Parcel’s category mix concentrated 80.38% of sales in Flower and 19.62% in Pre-Roll, with Flower down 42.95% year over year and up 0.02% month over month, while Pre-Roll declined 22.89% year over year and rose 31.13% month over month; overall brand sales fell 42.03% year over year and average price ticked up 0.63%. Within Flower, average price sat at $53.15 versus $11.42 in Pre-Roll, and the brand held rank 62 in Flower in Ontario, signaling that July 2026 mix stability masks rotation toward faster-moving Pre-Rolls; the pattern implies Parcel is relying on Pre-Roll momentum to counter Flower contraction without materially shifting total share yet.

The surge of 31.13% month-over-month in Pre-Roll alongside a 0.02% uptick in Flower and a 42.95% year-over-year Flower decline points to a consumer trade-down or occasion-shift that favors lower-price, higher-velocity formats even as overall average price rose 0.63%. With 80.38% exposure still in Flower and a rank of 62 in Ontario for Flower, the mix leaves Parcel over-indexed to a segment with steeper year-over-year declines, implying that sustained repositioning toward Pre-Roll could lift rank and stabilize sales if the July 2026 Pre-Roll trajectory persists while Flower remains a drag.

Competitive Landscape

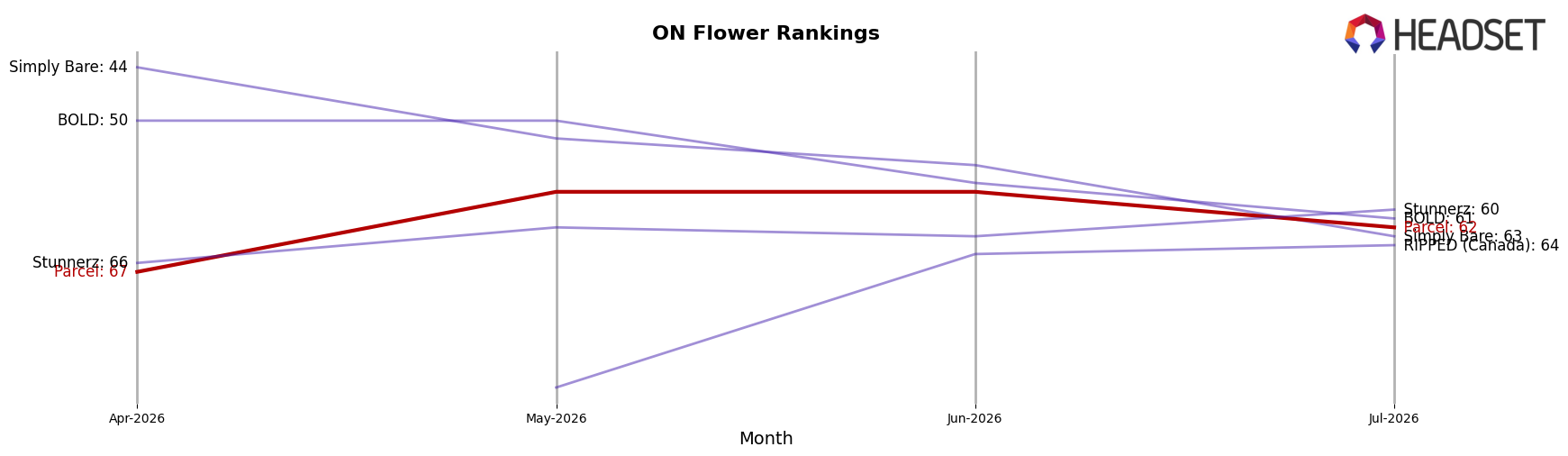

Parcel is ranked #62 in ON Flower in July 2026, down 8 positions year over year from #54 and up 5 positions versus April 2026’s #67, while its historical peak was #24 in August 2024 and is now 38 ranks lower; meanwhile, Shred climbed from #2 to #1 and Spinach advanced from #4 to #2 as Back Forty / Back 40 Cannabis slipped from #1 to #4, indicating leaders consolidated share at the top. With top competitors posting double-digit year-over-year sales changes—31.1% for Spinach and 17.2% for Shred—while a prior #1 fell 3 ranks, Parcel’s descent from its August 2024 peak and current mid-pack recovery pattern imply a brand caught between accelerating incumbents and a softening former leader, making sustained rank gains contingent on outpacing the recent 5-rank quarter-over-quarter lift.

Notable Products

Indica Sweet Notes Pre-Roll 2-Pack (1g) posted the standout movement in July 2026 with a 31% month-over-month gain while holding rank 1, contrasted with Sweet Notes (14g) inching up just 5% at rank 2, indicating momentum skewed toward value-sized pre-rolls over bulk flower. With two of the top two positions split between Pre-Roll and Flower, the category mix suggests diversification rather than concentration, and the $184,028 in sales tied to Sweet Notes (14g) did not translate into rank advancement despite its 5% lift. The absence of ranked positions for Grape Cream Cake (14g) and other Flower extensions alongside rank 1 dominance for a Pre-Roll signals portfolio gravity shifting toward convenience formats over traditional flower. Together, the pattern implies Parcel is tilting toward accessible pre-roll formats to drive velocity while keeping flagship flower as a scale anchor, prioritizing repeat purchase ease over large-pack trade-up.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.