Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Pro Gro is stocked at 321 licensed dispensaries across Michigan and Washington, 320 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Monroe, Grand Rapids, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

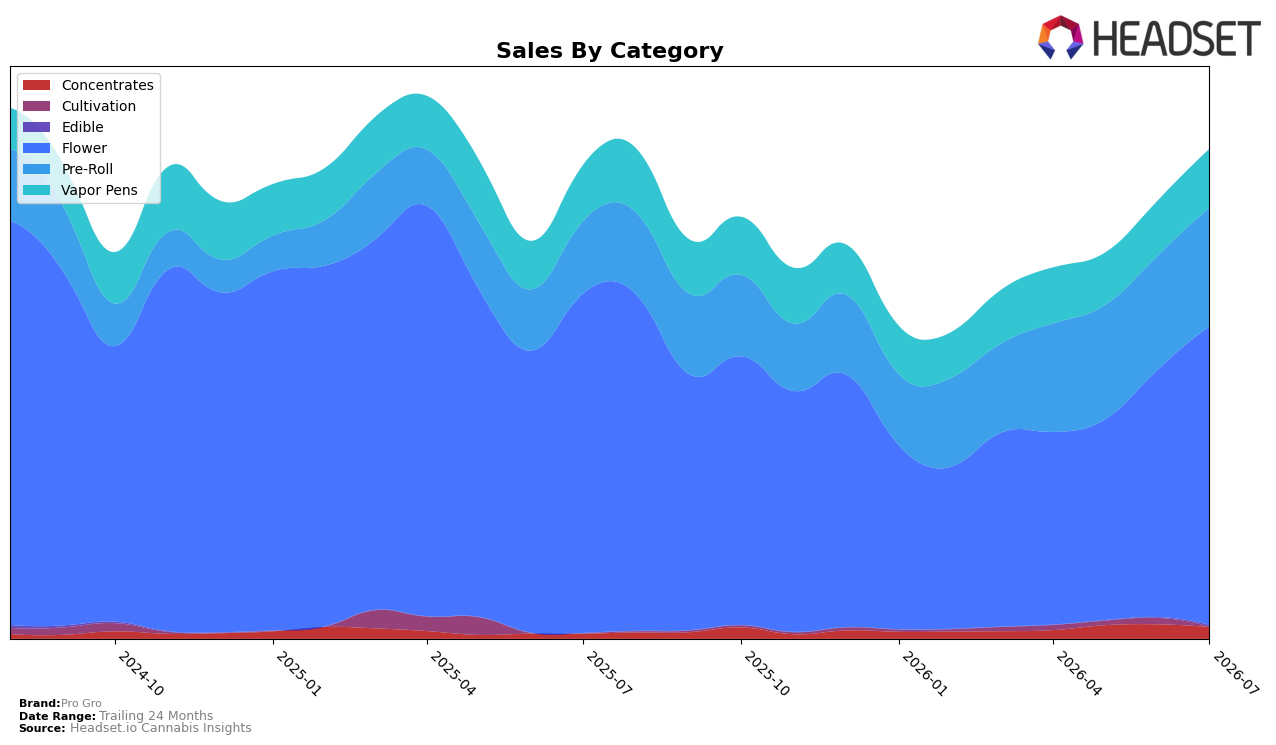

Pro Gro’s category mix in July 2026 concentrated 61.10% of sales in Flower, where sales declined 12.04% year over year but rose 20.58% month over month, while Pre-Roll expanded to 24.27% share on 63.96% YoY growth and a 4.07% MoM uptick. Vapor Pens held 11.99% share with 4.50% YoY growth and 6.92% MoM growth, and Concentrates, at 2.34% share, spiked 139.63% YoY but fell 19.42% MoM; Edible remained small at 0.30% share with a 250.42% MoM surge. With brand-level sales up 3.39% YoY but down 11.39% over 24 months and the average price down 20.53% YoY to $11.49, the pattern implies Pro Gro is shifting volume into lower-priced or smaller-format categories to offset Flower volatility while protecting near-term unit throughput.

The July 2026 mix change implies a positioning pivot toward value-accessible inhalables: Pre-Roll’s 24.27% share on 63.96% YoY growth coupled with Vapor Pens’ 11.99% share and 6.92% MoM growth points to broader basket entry even as Flower’s 12.04% YoY decline drags category incumbency. The 139.63% YoY spike in Concentrates alongside a 19.42% MoM pullback suggests opportunistic wins that are sensitive to promo or assortment cadence, while the 250.42% MoM jump in Edible at 0.30% share hints at test-and-expand rather than core scale. Taken together with a 5th-place Flower rank in Michigan and a 20.53% YoY drop in average price, the mix points to a strategy trading price for share across inhalables to stabilize overall sales while ceding premium positioning in flagship Flower.

Competitive Landscape

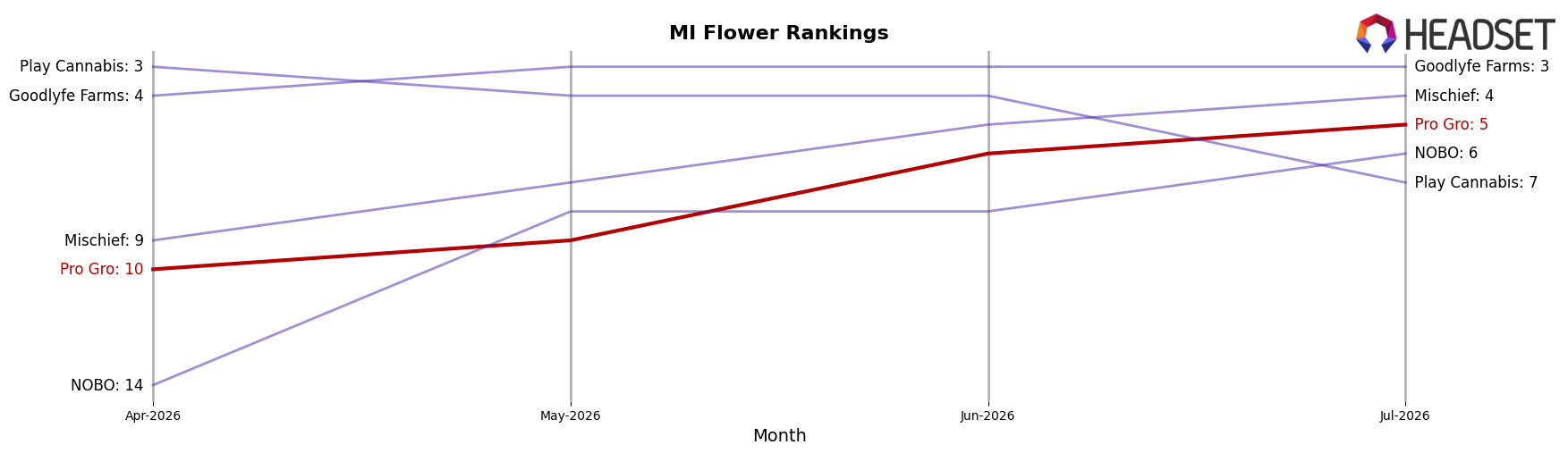

Pro Gro sits at rank #5 in MI Flower in July 2026, down 2 positions year over year from #3, and up 5 slots since April 2026 when it was #10; that swing suggests share recapture within the quarter despite a longer-run slide. Against competitors, High Minded holds #1 while posting a -12.46% year-over-year sales change, and Mischief moved from #10 to #4 year over year with a 59.39% sales increase, indicating Pro Gro is gaining sequentially but ceding ground to faster risers. Further, Goodlyfe Farms advanced to #3 with 36.83% growth while Society C stayed at #2 with a 0.28% uptick, placing Pro Gro between a contracting leader and expansionary mid-pack peers; the pattern implies Pro Gro’s rank trajectory is stabilizing in the mid‑top tier but requires acceleration to avoid being bracketed by competitors expanding at double‑digit rates.

Notable Products

Lunar Lemon Pre-Roll (1g) posted the standout move with a 115.8% month-over-month gain to rank 2 in July 2026, while Moonbow #112 Pre-Roll (1g) fell 66.5% but still held rank 1. Ice Cream Cake Pre-Roll (1g) rose 14.8% at rank 9 and Super Boof Pre-Roll (1g) added 10.5% at rank 4, indicating momentum is skewing to a few rising SKUs rather than broad uplift. With all ten top products in the Pre-Roll category and Red Runtz Pre-Roll (1g) slipping 1.9% at rank 7, the mix concentrates revenue in a single format with a volatile leader-follower dynamic that points to a need for depth in fast-moving flavor profiles. The pattern implies Pro Gro is steering toward amplification of breakout Pre-Roll variants while managing sharp downswings in prior leaders to stabilize category share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.