Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

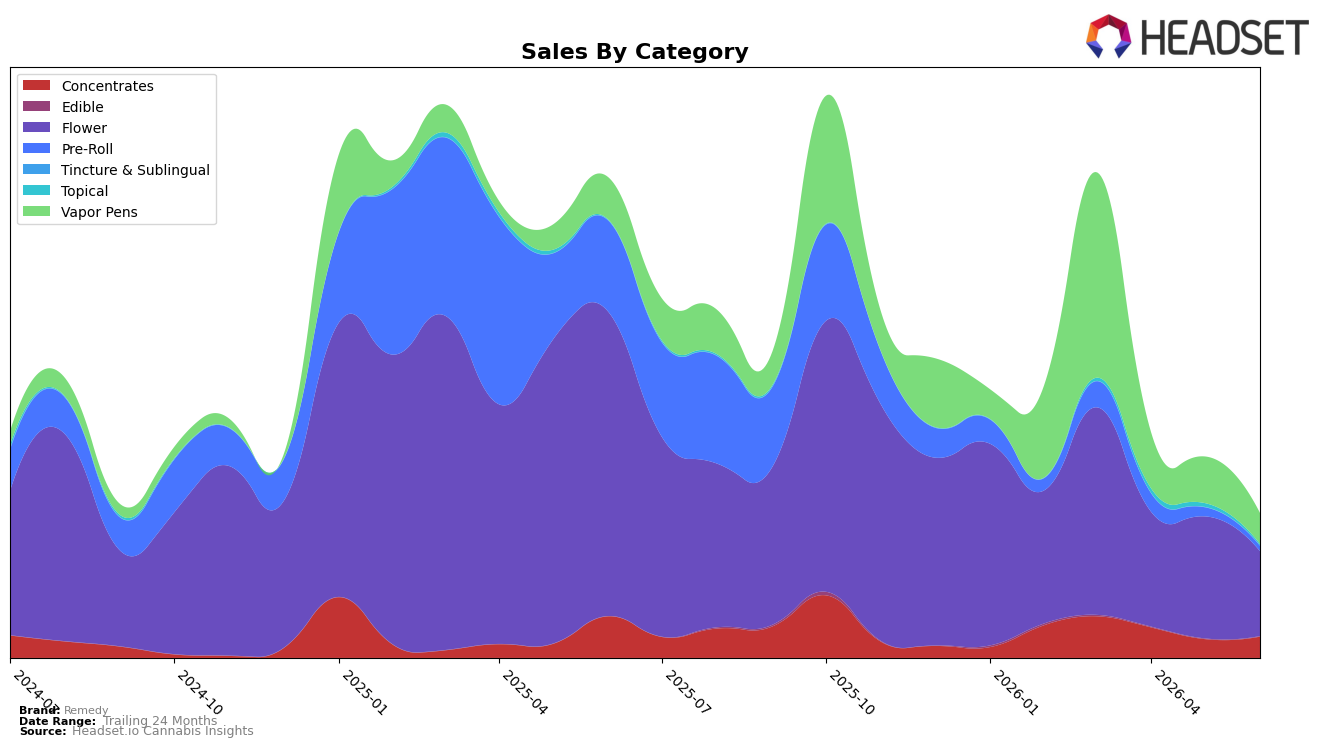

In June 2026, Remedy’s mix is dominated by Flower at 59.29% share, but the category posted a 72.17% year-over-year decline and a 30.47% month-over-month drop, pulling overall performance down alongside a 63rd rank in Flower within Nevada. Vapor Pens hold 21.47% share with a 27.00% year-over-year contraction and a sharper 33.81% month-over-month fall, while Concentrates at 14.72% share bucked the monthly slide with a 13.32% month-over-month increase despite a 49.11% year-over-year decline. Pre-Roll has thinned to 3.53% share after a 94.45% year-over-year and 42.87% month-over-month reduction, and Topical’s tiny 0.84% share carried a 198.72% year-over-year surge but a 66.19% month-over-month pullback. The pattern implies that Remedy’s exposure to two shrinking anchors—Flower and Vapor Pens—overwhelms smaller bright spots, concentrating risk in categories with steep year-over-year erosion.

These shifts point to a positioning pivot: the 13.32% month-over-month gain in Concentrates against double‑digit month-over-month drops in Flower (30.47%) and Vapor Pens (33.81%) suggests headroom in a lower-priced, value-accessible format, supported by an overall 34.30% average price lift year over year that may be pressuring high-ticket segments. With Flower still at 59.29% share and ranked 63rd in Nevada Flower, maintaining that weight likely prolongs decline, whereas reallocating mix toward Concentrates and pruning Pre-Roll after a 94.45% year-over-year collapse could reduce volatility. The implication is that Remedy’s defensible positioning in June 2026 is to de-emphasize premium-priced inhalables where price sensitivity is evident and lean into Concentrates as the stabilizer while testing small, low-risk bets in Topical given its 198.72% year-over-year lift despite a 66.19% month-over-month reset.

Competitive Landscape

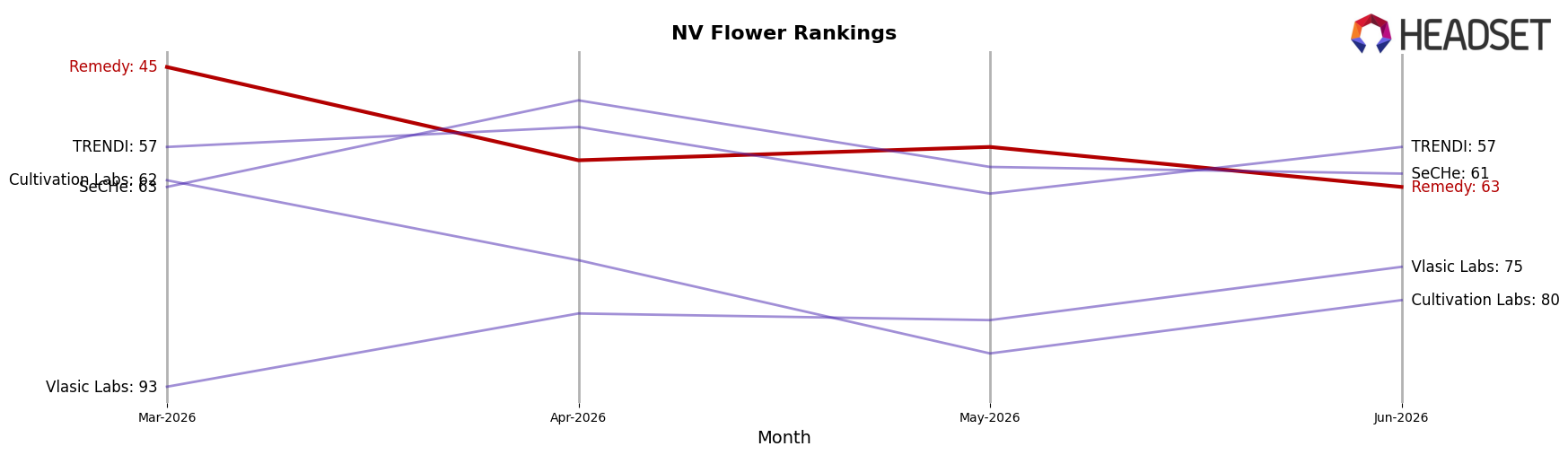

Remedy ranks #63 in NV Flower in June 2026, sliding 28 positions year over year from #35, and down 18 spots since March 2026 from #45, while its historical peak was #33 in May 2025; by contrast, STIIIZY held at #1 year over year with a 5.2% sales increase, and FloraVega / Welleaf climbed from #22 to #3 alongside a 260.4% sales surge, indicating that Remedy’s downward rank momentum coincides with competitors either consolidating leadership or accelerating into the top tier, implying that Remedy’s trajectory points to loss of share concentration toward leaders and fast-rising challengers unless course-corrected.

Notable Products

Wedding Cake (3.5g) posted the steepest movement in June 2026 with a -55.1% month-over-month drop and slid to rank 5, while Las Vegas Kush Cake (3.5g) held rank 1 despite a -18.2% decline. Bio-Jesus (3.5g) advanced with +23.3% MoM at rank 4, and OG 18 (3.5g) added +5.8% at rank 3, indicating mixed traction within Flower where six of the top ten SKUs concentrate. The presence of three Concentrates in ranks 2, 8, and 9, including Sticky Icky Live Resin Badder (0.05g) at +24.8% MoM and $2,295 in sales, offsets Flower volatility but does not yet reorder the leaderboard. The pattern implies Remedy is leaning on premium Flower equity for scale while newer Concentrates provide incremental stability rather than primary growth engines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.