Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

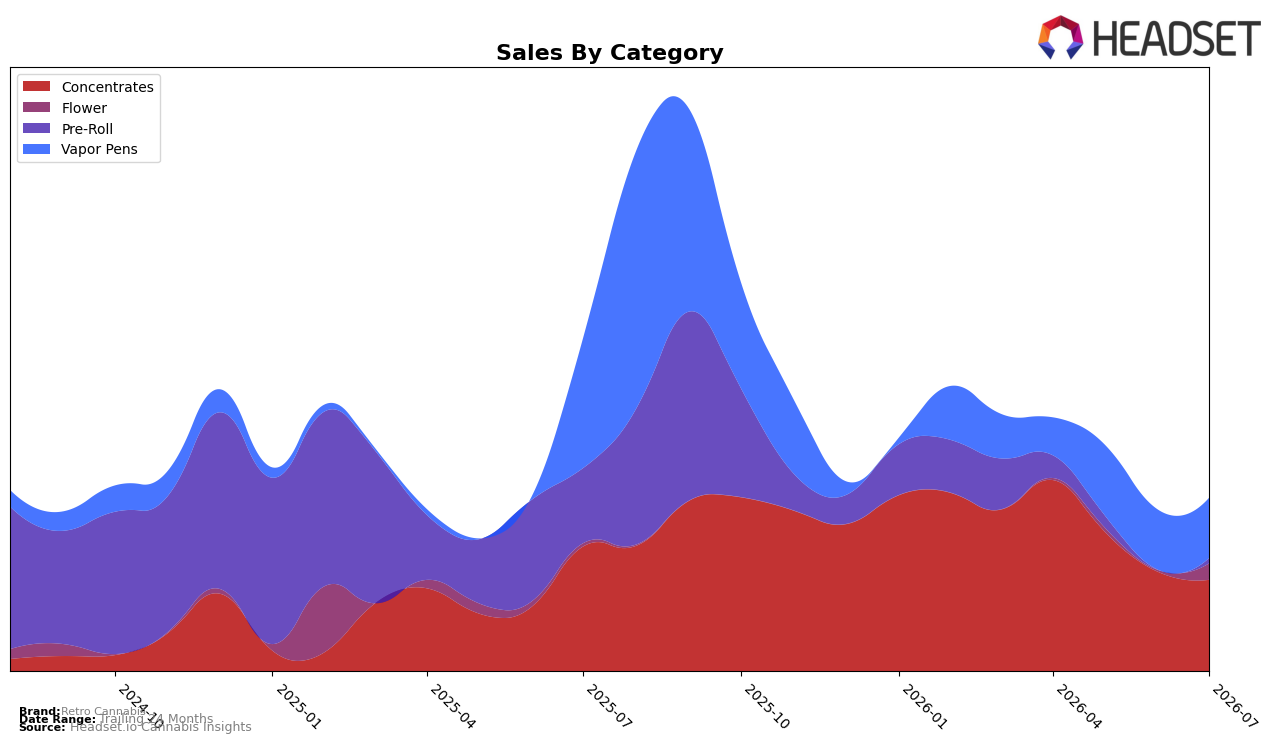

In July 2026, Retro Cannabis concentrated 52.93% of sales in Concentrates with a year-over-year decline of 26.64% and a month-over-month drop of 8.15%, while Vapor Pens held 34.76% share with a 53.64% YoY contraction but a 0.10% MoM uptick. Flower expanded to 9.36% share on a 429.28% YoY surge and a 921.73% MoM spike, whereas Pre-Roll slipped to 2.95% share with a 93.19% YoY fall and no reported MoM change. With the brand’s average price up 8.58% YoY to $30.50, the mix shows a pivot away from Vapor Pens and legacy Pre-Roll toward a higher-volume, lower-price Flower entry and a still-dominant but shrinking Concentrates base, implying resource reallocation from stagnant formats to recovering and scalable ones.

The mix shift implies Retro Cannabis is defending category breadth to offset a 47.99% YoY brand sales decline while maintaining exposure to its highest-share anchor in Concentrates and selectively rebuilding through Flower. Holding rank 37 in Vapor Pens in Saskatchewan while Vapor Pens’ share sits at 34.76% and declines 53.64% YoY suggests the brand’s competitive posture in that format has weakened, and the 0.10% MoM lift is insufficient without the 921.73% MoM acceleration in Flower and an 8.15% MoM pullback in Concentrates; the pattern implies near-term positioning will hinge on sustaining Flower’s momentum while stabilizing Concentrates to prevent further rank erosion in Vapor Pens.

Competitive Landscape

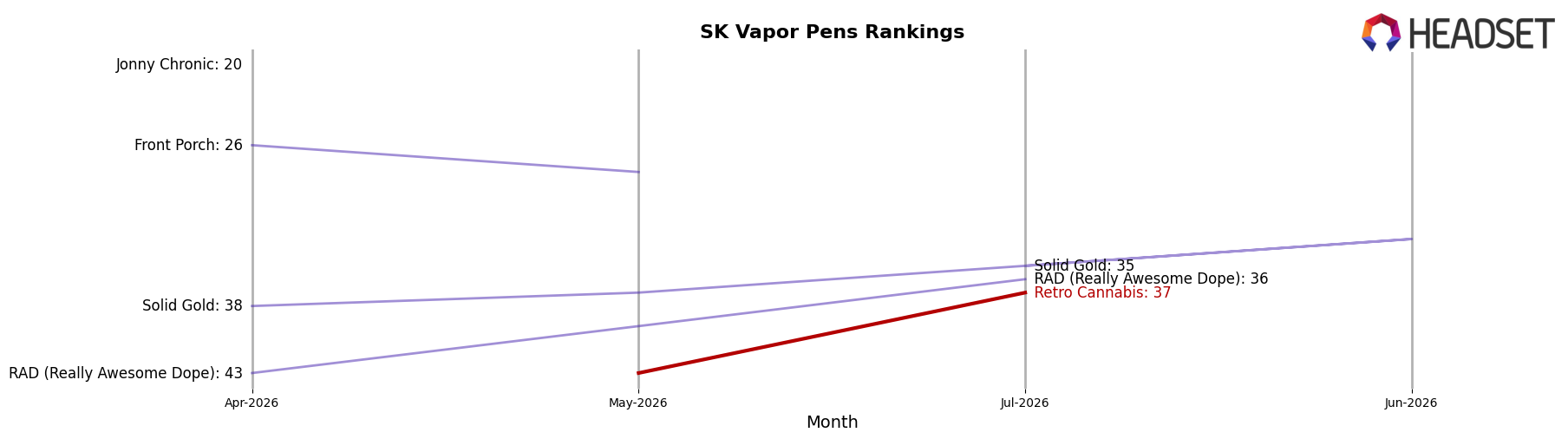

Retro Cannabis ranks #37 in SK Vapor Pens in July 2026, down 7 positions year over year from #30 and up 14 positions versus April 2026 when it sat at #51; against its historical ceiling of #26 in September 2025, the current slot is 11 ranks lower, while the market’s top tier is consolidating as Spinach holds #1 with 18.9% year-over-year sales growth and JC Green Cannabis Company jumps from #17 to #5 on 116.2% growth. Compared with Back Forty / Back 40 Cannabis steadying at #3 with 33.0% growth and Sticky Greens slipping at #4 with a 36.4% decline, Retro Cannabis’s rebound from #51 to #37 over three months alongside a 7-place year-over-year drop signals mid-pack volatility: recent momentum exists, but reclaiming the #26 peak likely depends on outpacing fast-rising incumbents rather than merely avoiding decline.

Notable Products

Blockbuster Nights (3.5g) surged 919.9% month over month to rank 4 in July 2026, while Pink Kush Honey Oil (1g) jumped 110.1% as Concentrates also posted a 58.4% lift for Honey Oil Infused Hash (2g); by contrast, R2 Full Spectrum Honey Oil Syringe (1g) fell 35.5% to rank 2. CBD/THC 1:1 Perfect Harmony Full Spectrum Cartridge (1g) held rank 1 despite a 4.0% decline, and Vapor Pens depth was mixed as R2 Full Spectrum Honey Oil Cartridge (1g) rose 29.8% at rank 6. Four of the top ten are Concentrates SKUs, indicating the brand’s momentum is tilting toward oil-based formats even as the top Vapor Pen acts as a stabilizer. This product mix implies Retro Cannabis is leaning into value-accretive oils while using a breakout Flower SKU to diversify traffic and reduce category risk.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.