Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

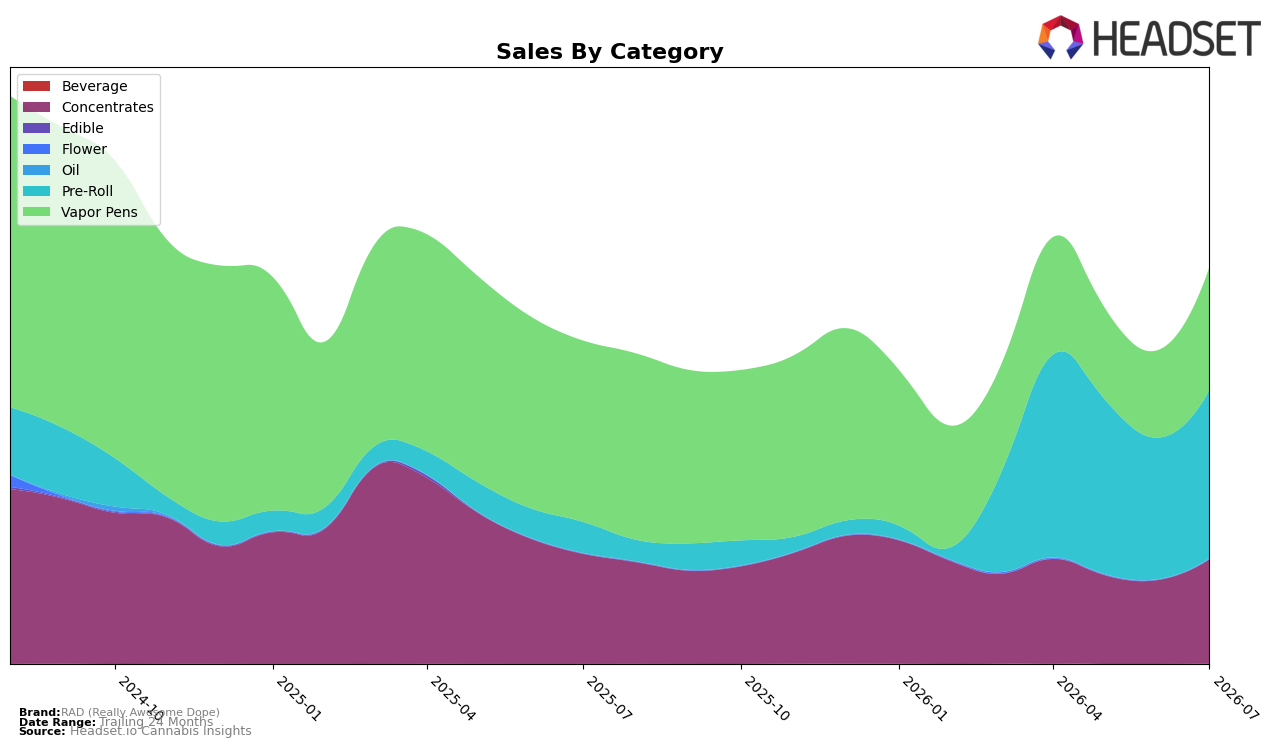

RAD (Really Awesome Dope) shifted its mix in July 2026 toward Pre-Roll at 42.53% share, with Pre-Roll sales up 449.45% year over year and 19.01% month over month, while Vapor Pens held 31.05% share with a -32.29% year-over-year change but a 40.48% month-over-month rebound. Concentrates accounted for 26.32% share with a -5.24% year-over-year dip and a 24.28% month-over-month lift, and Beverage, though just 0.08% share, rose 300.97% year over year as Edible fell 10.35% year over year to 0.02% share. With an average price up 5.99% year over year to $28.95 and the brand ranked 36 in Vapor Pens in Saskatchewan, the pattern indicates a pivot where rapid Pre-Roll expansion and short-term Vapor Pen recovery are compensating for category-specific headwinds, concentrating growth into inhale-led formats.

The combination of a 42.53% Pre-Roll share alongside a 31.05% Vapor Pen share suggests RAD (Really Awesome Dope) is recalibrating toward value-per-hit formats, as evidenced by month-over-month gains of 19.01% in Pre-Roll and 40.48% in Vapor Pens despite a -32.29% year-over-year decline in the latter. The 24.28% month-over-month rise in Concentrates paired with a modest -5.24% year-over-year decline implies a stabilizing third pillar, while a 300.97% year-over-year uptick in Beverage from a 0.08% share base and a 10.35% year-over-year contraction in Edible signal limited near-term contribution from non-inhalables. Given the 36 rank in Vapor Pens in Saskatchewan and a brand-level 22.81% year-over-year sales increase against a -43.58% two-year trajectory, the implication is a near-term reliance on Pre-Roll-led acquisition with Vapor Pens as the swing factor for share recovery, while price inflation of 5.99% year over year narrows room for premiumization without further mix shifts.

Competitive Landscape

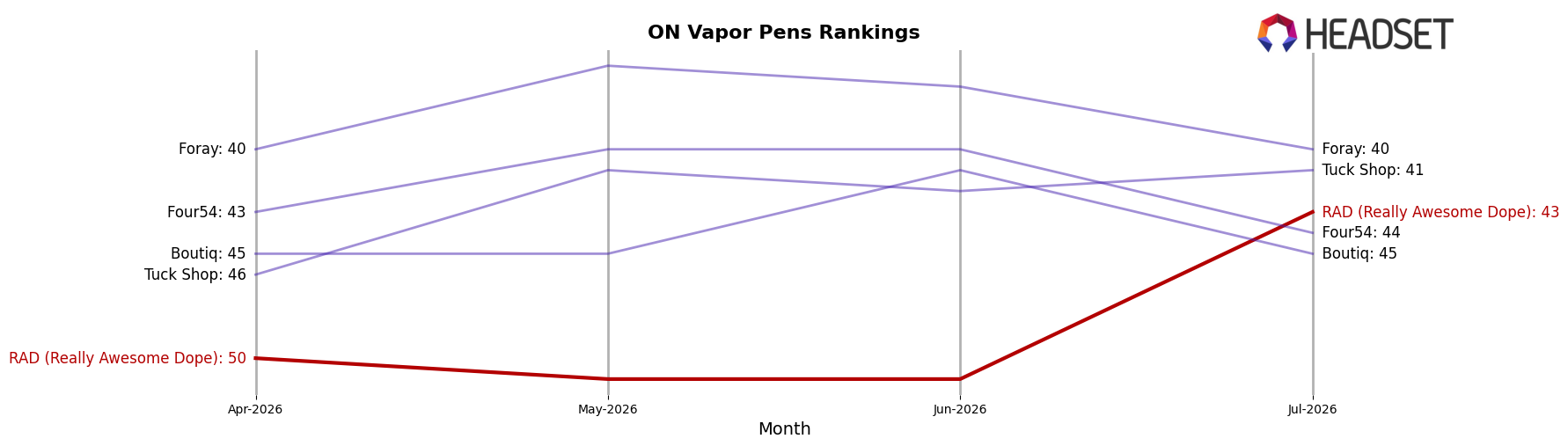

RAD (Really Awesome Dope) sits at rank #43 in July 2026, slipping 4 positions year over year from #39 and improving 7 positions since April 2026’s #50, while still trailing its October 2024 peak of #32; meanwhile, Spinach climbed from #4 to #1 with 144.7% YoY sales growth and BoxHot moved from #2 to #3 despite 4.6% YoY growth, indicating that RAD’s downward YoY rank change contrasts with competitors gaining or consolidating top-5 positions. Compared to Back Forty / Back 40 Cannabis holding near the top by moving from #1 to #2 with 9.3% YoY growth and General Admission declining from #3 to #4 on an 19.0% YoY sales drop, RAD’s mid-pack slide from #39 to #43 alongside a recent quarter rebound from #50 signals share pressure from ascending leaders and limited spillover from underperformers; the rank trajectory implies RAD is stabilizing off its quarterly low but is unlikely to re-approach its #32 peak without capturing trade-down or value-driven switchers from competitors losing momentum.

Notable Products

Blue Razz Distillate Cartridge (1g) posted the month’s headline move with an 85.5% MoM surge to rank 2, while Fruity Gobbstomper Distillate Cartridge (1g) also advanced 54.2% to rank 4, signaling a decisive tilt toward Vapor Pens in July 2026. Skullcrushers 70's - Iced Raspberry Infused Pre-Roll 3-Pack (1.35g) held rank 1 with an 18.4% MoM gain as Pre-Rolls still anchor the top spot, yet two Vapor Pens now sit inside the top four versus Pre-Rolls occupying ranks 1 and 3, indicating the mix is pivoting to inhalable oil formats. With four of the top ten as Pre-Roll SKUs but two rapidly rising Vapor Pens, the product set points to RAD (Really Awesome Dope) leaning into higher-velocity cartridges while defending flagship infused Pre-Rolls, implying near-term merchandising should prioritize cartridge depth without diluting the Pre-Roll halo.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.