Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

TasteBudz (CO) is stocked at 198 licensed dispensaries across Colorado and Oregon, 177 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Boulder, Pueblo, and Aurora. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

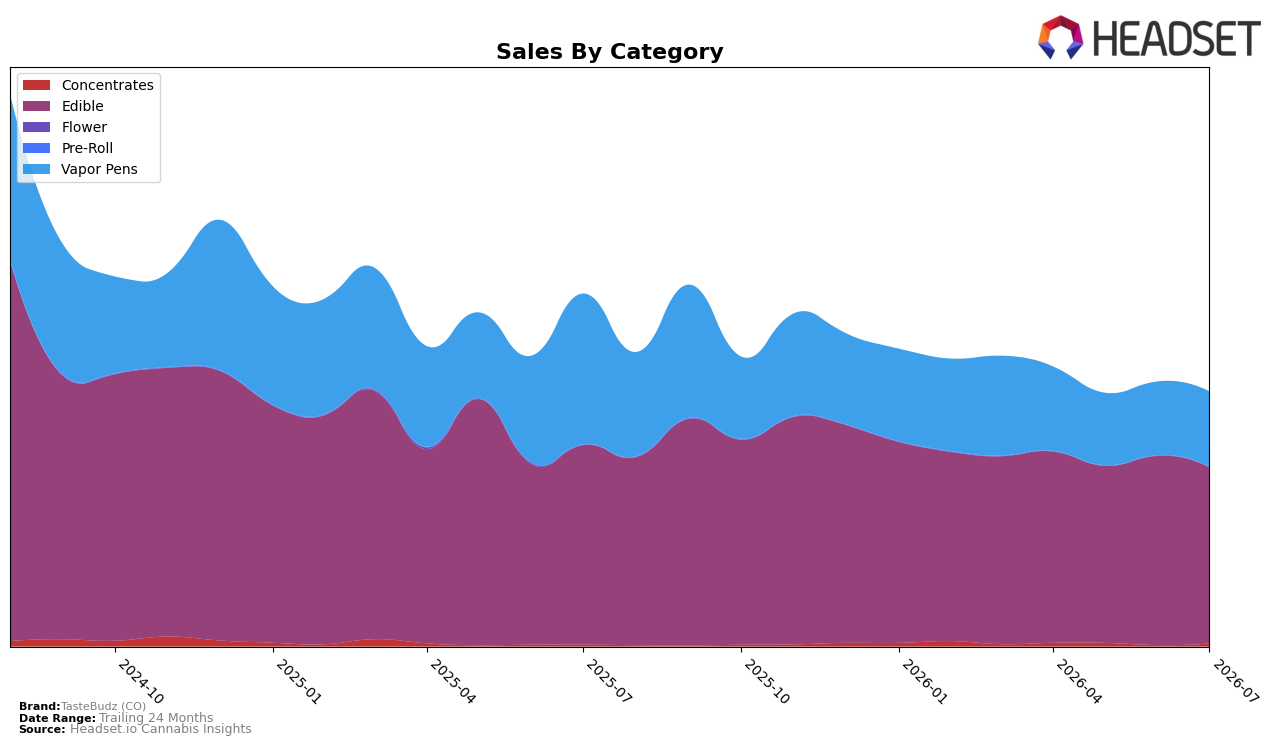

In July 2026, TasteBudz (CO) concentrated 69.34% of sales in Edible, where sales fell 11.75% year over year and 6.94% month over month, while Vapor Pens held 29.58% share with a 50.15% YoY decline but a 2.22% MoM uptick. Concentrates remained a niche at 1.08% share, yet expanded 69.67% YoY and 133.89% MoM, with the brand’s average price down 22.78% YoY against an Edible average price of $14.13. Taken together with an overall brand YoY sales change of -27.83% and a 24‑month decline of 56.22%, the mix shift implies reliance on Edible drag is outweighing small-pocket growth in Concentrates, setting the stage for incremental reallocation rather than wholesale category exit.

Positionally, anchoring at rank 8 in Edible in Colorado while Edible share sits at 69.34% suggests the brand’s core placement is vulnerable if the 6.94% MoM drop persists alongside a 50.15% YoY hit in Vapor Pens. The 2.22% MoM rise in Vapor Pens combined with a 133.89% MoM surge in Concentrates at only 1.08% share points to a barbell opportunity: defend the Edible base to preserve rank while selectively scaling higher-velocity SKUs in Vapor Pens and Concentrates to offset the -27.83% YoY brand decline; the practical implication is portfolio pruning in Edible and targeted price-pack architecture where MoM momentum is visible.

Competitive Landscape

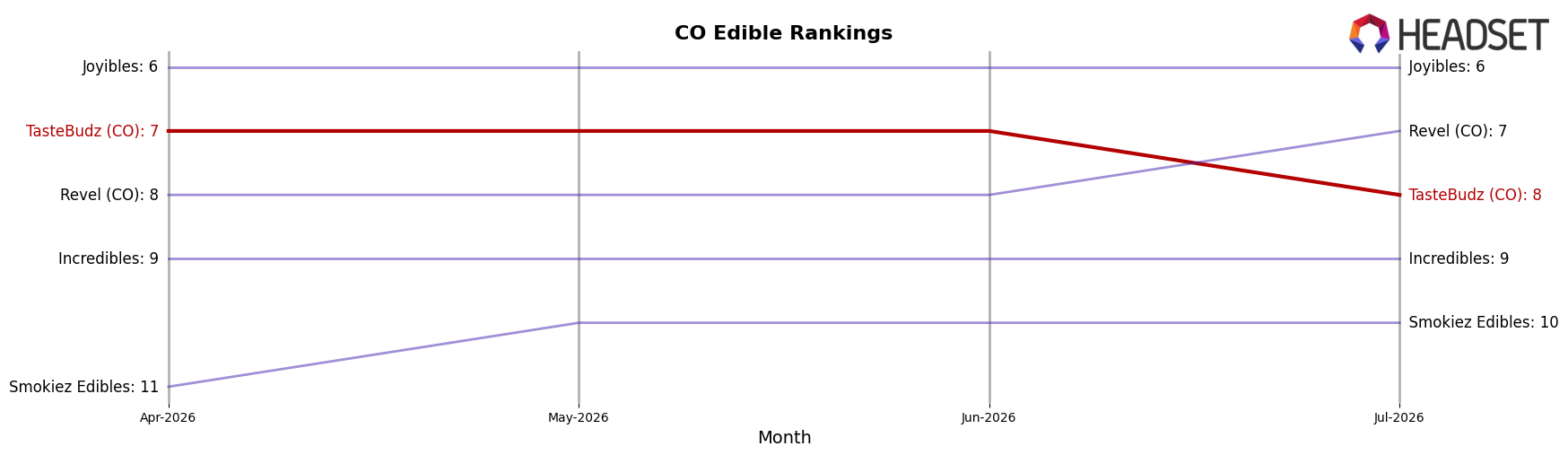

TasteBudz (CO) sits at rank #8 in CO Edible in July 2026, down 1 position year over year from #7, and also 1 spot lower than its April 2026 rank of #7; meanwhile its peak of #5 in January 2025 is 3 places ahead of today, indicating a two-step slide from peak to current. Competitive movement reinforces this shift: Wyld holds #1 despite a -24.4% YoY sales change, while Dialed In Gummies climbed from #3 to #2 on +15.8% YoY sales, and Wana slipped from #2 to #3 with a -16.2% YoY change; against that backdrop, TasteBudz (CO) moving from #7 to #8 while the category leader contracted and a challenger advanced implies share is being redistributed toward faster-growing rivals rather than lifted by category tailwinds.

Notable Products

Hybrid Assorted Fruit Flavors Rosin Gummies 10-Pack (100mg) posted the steepest decline at -33.98% and slid to rank 7, while Indica Tropical Punch Live Rosin Gummies 10-Pack (100mg) fell -32.45% to rank 10; by contrast, Sour Green Slapple Gummies 10-Pack (100mg) rose 19.30% to hold rank 1. Nightly Rituals - CBD/CBN/THC 1:1:1 Blueberry Lavender Rosin Gummies 20-Pack (100mg CBD,100mg CBN,100mg THC) dropped -21.37% yet still sat at rank 2, and Strawberry Lemon Fade Gummies 10-Pack (100mg) gained 10.58% at rank 3; nine of the top ten are Edible SKUs, concentrating the lineup in one category. The split between double-digit declines in several rosin SKUs and gains in core fruit flavors implies a tilt toward mainstream edible profiles over niche rosin-led variants for July 2026, with pricing headroom suggested by $72,574 on the leading wellness-format multi-cannabinoid pack.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.