Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

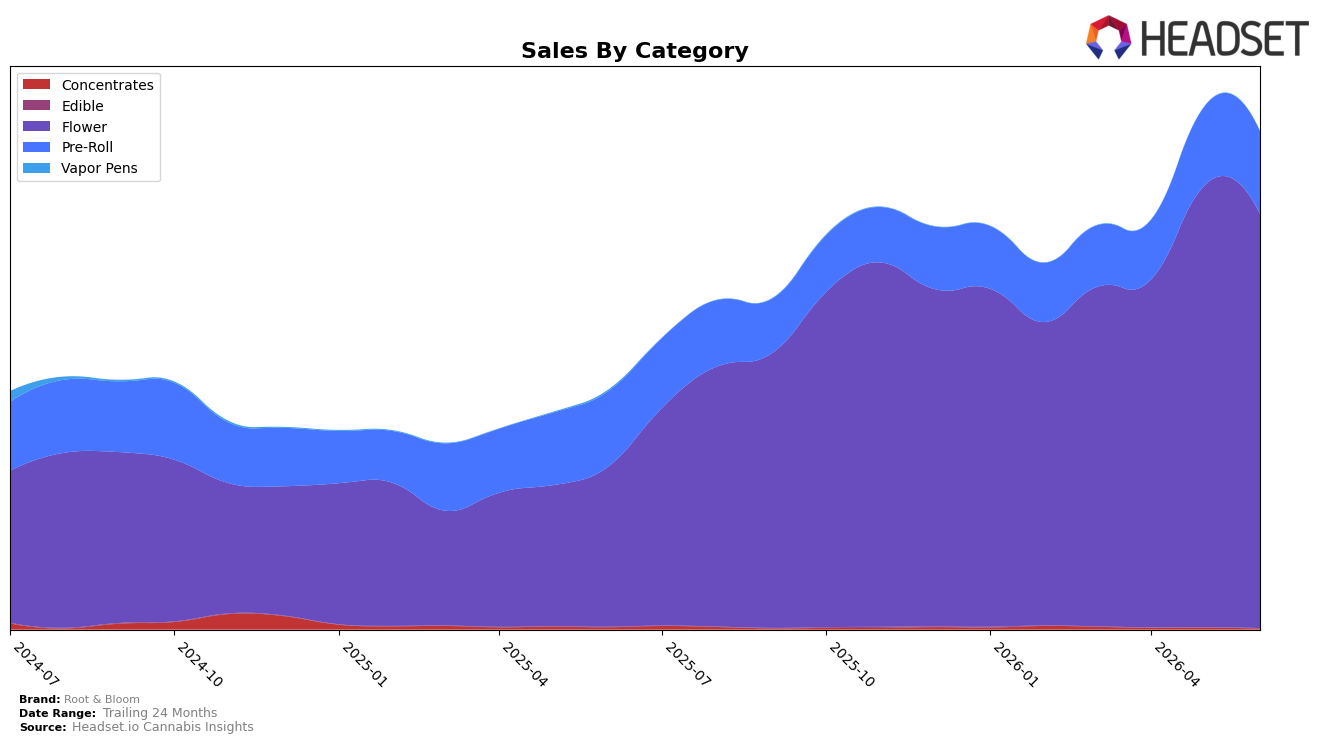

In June 2026, Root & Bloom concentrated 83.27% of sales in Flower with a 158.87% year-over-year gain but a -6.32% month-over-month dip, while Pre-Roll held 16.59% share with 9.84% year-over-year growth and a 4.76% month-over-month increase; Concentrates fell to 0.14% share with -65.55% year-over-year and -55.83% month-over-month declines. With average prices up 29.04% year over year to $24.87 and Flower’s average price at 44.38, the mix is skewing toward higher-ticket Flower even as sequential Flower volume softens; the pattern implies Root & Bloom is trading up within Flower in Massachusetts while leaning on Pre-Roll’s month-over-month lift to buffer volatility.

Holding rank 5 in Flower in Massachusetts alongside an 83.27% category share points to defensible shelf presence, but the -6.32% month-over-month in Flower against a 4.76% month-over-month rise in Pre-Roll suggests exposure to short-term demand swings concentrated in a single category; the implication is a positioning that prioritizes premium Flower leadership with selective Pre-Roll expansion. The 108.75% brand sales year-over-year increase alongside a 97.05% 24‑month rise indicates durable trajectory, yet the -55.83% month-over-month and -65.55% year-over-year declines in Concentrates signal limited traction in that niche; the pattern implies near-term gains will depend on sustaining Flower price realization while growing Pre-Roll’s 16.59% share to reduce single-category risk.

Competitive Landscape

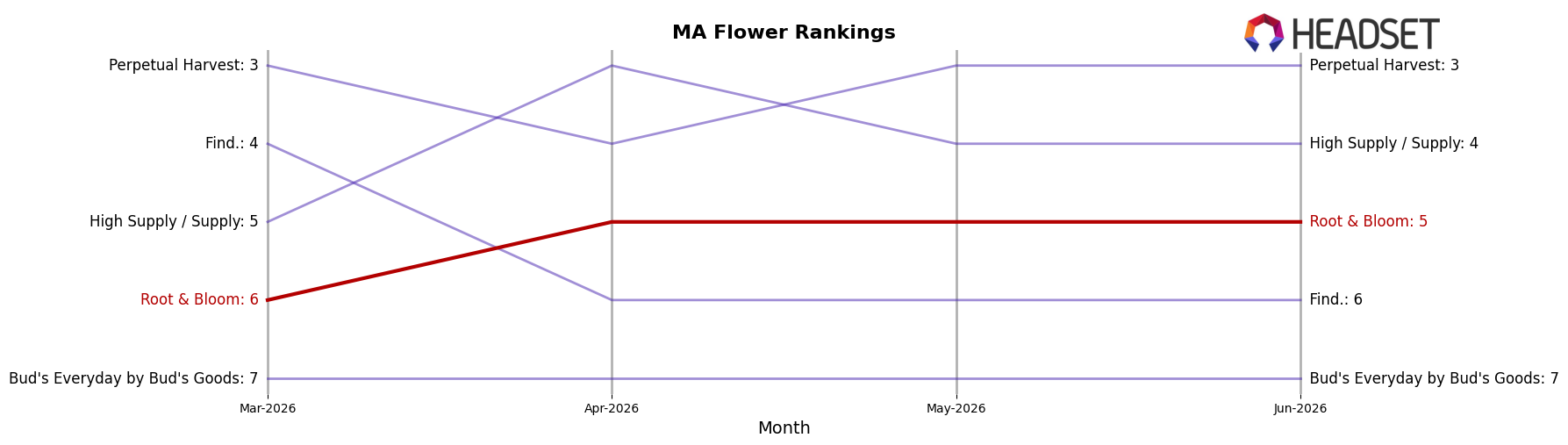

Root & Bloom is currently ranked #5 in Massachusetts Flower, up 11 places year over year from #16 to #5 and improving 1 position since March 2026 from #6 to #5, reaching its peak in June 2026; meanwhile, Farmer's Cut moved from #3 to #1 with 32.4% YoY sales growth and High Supply / Supply advanced from #5 to #4 with 16.7% YoY growth, while Simply Herb slipped from #1 to #2 with a 1.6% YoY sales decline. These shifts place Root & Bloom as the fastest rank climber among the current top five (+11 vs. +2 for Perpetual Harvest and +4 for High Supply / Supply), indicating that its recent ascent is driven more by share capture than category tailwinds and implying a trajectory toward sustained top-five presence if gains persist.

Notable Products

Gelato Punch Pre-Roll (1g) posted the standout move in June 2026 with +76.6% MoM to rank 3, while Durban Margy Pre-Roll (1g) fell -15.7% to rank 5, indicating volatility clustered within the same format. Wedding Cake Pre-Roll (1g) held rank 1 despite a -1.3% MoM dip, and Lemonhead Delight Pre-Roll (1g) advanced +15.4% at rank 2, while three Flower SKUs sat lower with Wedding Cake (3.5g) at rank 7 (-6.8%), Cherry Pie OG (3.5g) at rank 9 (-8.1%), and Ghost Dawg (3.5g) at rank 10 (-15.0%). With six of the top ten as Pre-Rolls and multiple gains concentrated in that set, the mix implies Root & Bloom is tilting toward Pre-Rolls as the near-term volume engine at the expense of Flower, even as flagship names persist across both formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.