Where to Buy

Runtz is stocked at 202 licensed dispensaries across New York, Florida, and 3 other states, 185 of them in New York, with the deepest coverage in New York, Buffalo, Queens, Rochester, and Brooklyn. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

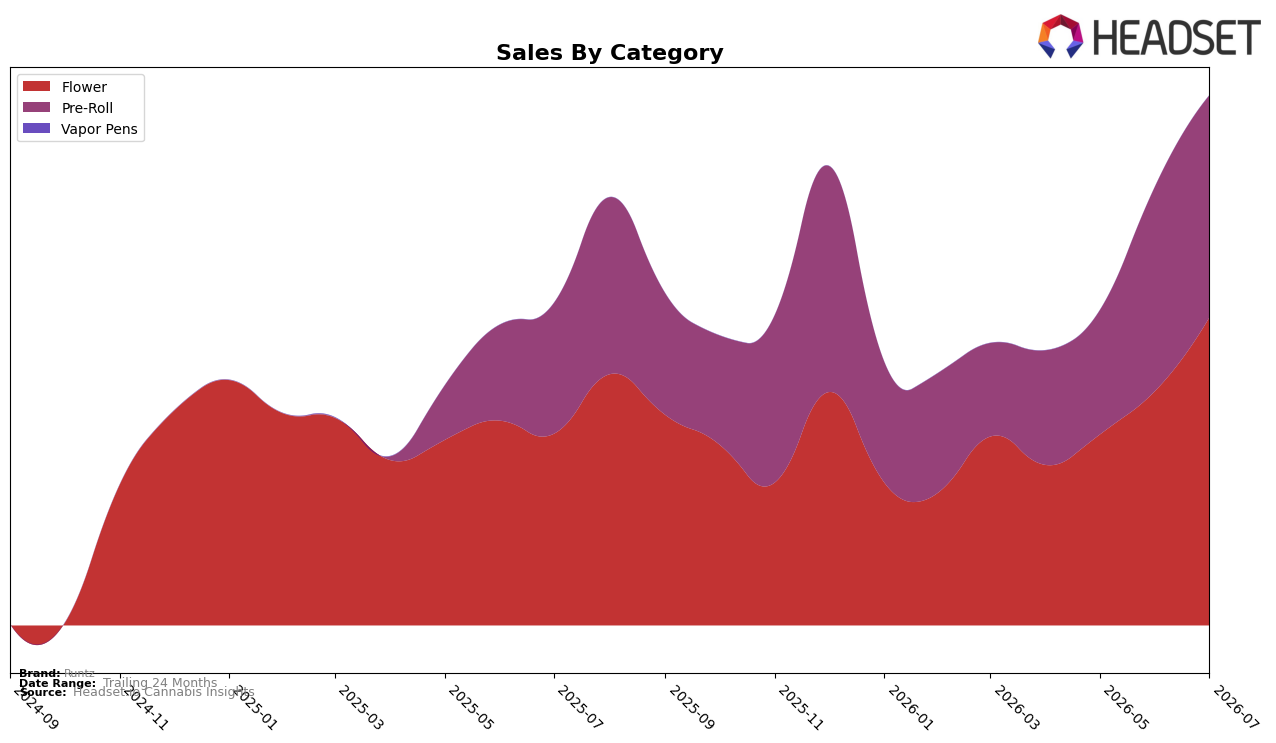

Runtz’s mix in July 2026 concentrated 58.10% of sales in Flower (ranked 18 in New York Flower) versus 41.90% in Pre-Roll, with Flower up 60.75% year over year and 31.14% month over month while Pre-Roll rose 69.75% year over year and 8.23% month over month. The brand’s average price dipped 1.25% year over year to $28.27 even as total brand sales climbed 64.40% year over year, implying volume-led growth with Flower’s faster month-on-month acceleration overtaking Pre-Roll’s slower sequential gain.

The mix shift and pacing imply Runtz is leaning into Flower to drive incremental share and rank gains, as a 31.14% month-over-month lift in Flower against an 8.23% month-over-month lift in Pre-Roll suggests resource or promotional weighting toward higher-ticket units. Given a 60.75% year-over-year rise in Flower against a 69.75% rise in Pre-Roll but a lower brand-level average price by 1.25%, the positioning trend points to widening the entry points via Pre-Roll to recruit while relying on Flower’s scale to anchor category visibility and support movement from rank 18 upward in New York.

Competitive Landscape

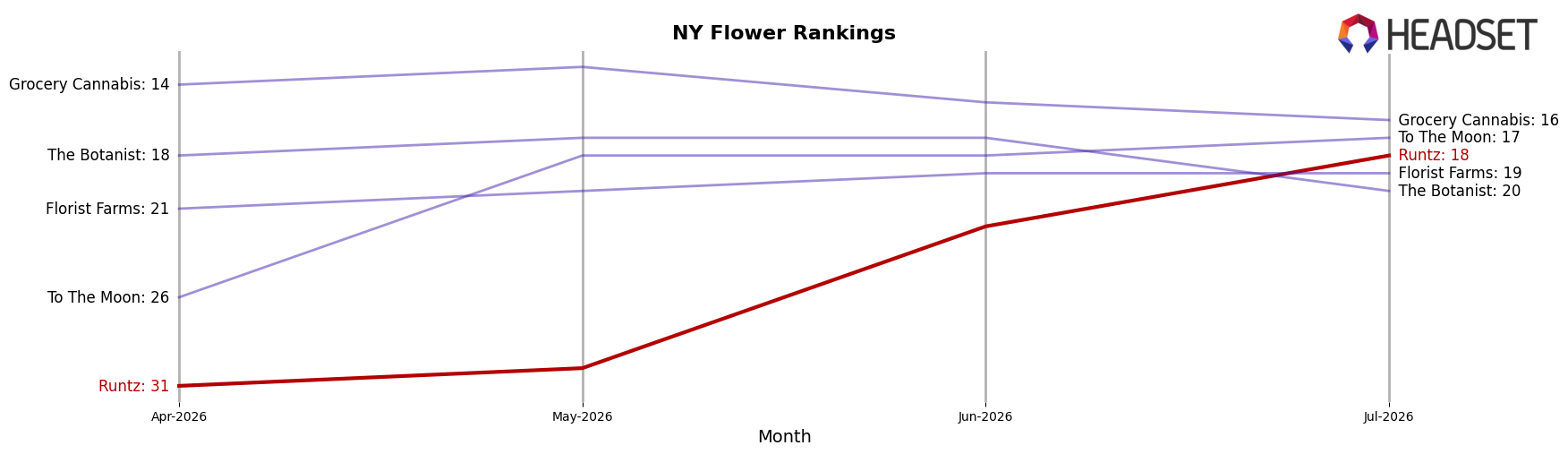

Runtz sits at rank #18 in New York Flower in July 2026, a 4-place improvement from #22 year over year, and a 13-place climb from #31 three months ago; however, it remains just below its historical peak of #17 from January 2025, indicating progress but not a new high. In contrast, Find. moved from #8 to #1 year over year while growing sales by 46.7%, and Grassroots advanced from #15 to #5 alongside a 79.8% sales increase, suggesting Runtz’s rank gains are slower than leaders that combined upward mobility with sharper growth. With peers like Leal rising from #7 to #2 and Untitled moving from #4 to #4 year over year while adding 15.7% in sales, Runtz’s 4-rank YoY improvement and 13-rank quarter-on-quarter lift point to recovery momentum that could sustain mid-pack positioning unless translated into larger share shifts.

Notable Products

Amaretto Di Lemon Pre-Roll 2-Pack (1.5g) posted the standout move in July 2026 with a +152% month-over-month surge, vaulting into rank 4, while Pluto Pre-Roll 2-Pack (1.5g) followed with a +150% jump to rank 6. In contrast, Lemon Candy Runtz Pre-Roll 2-Pack (1.5g) fell -40% yet still held rank 5, and White Cherry Runtz Pre-Roll 2-Pack (1.5g) dropped -64% to rank 9, marking a sharp bifurcation between winners and laggards inside the lineup. Eight of the top ten are Pre-Roll SKUs, concentrated across ranks 1 through 6 and 8 through 9, with Pink Runtz Pre-Roll 2-Pack (1.5g) up +16% at rank 1 and Obama Runtz Pre-Roll 2-Pack (1.5g) up +71% at rank 2 anchoring momentum, while Flower entries like Frog Poison (3.5g) at rank 7 and L'Orange (3.5g) at rank 10 carry only part of the volume at $229,544 combined. The pattern implies Runtz is consolidating around Pre-Rolls as the commercial engine, using a few breakout SKUs to offset volatility in slower variants and leaving Flower as a complementary, not lead, contributor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.