Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sinse Cannabis is stocked at 179 licensed dispensaries across Missouri, with the deepest coverage in St. Louis, KCMO, Springfield, Columbia, and Independence. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

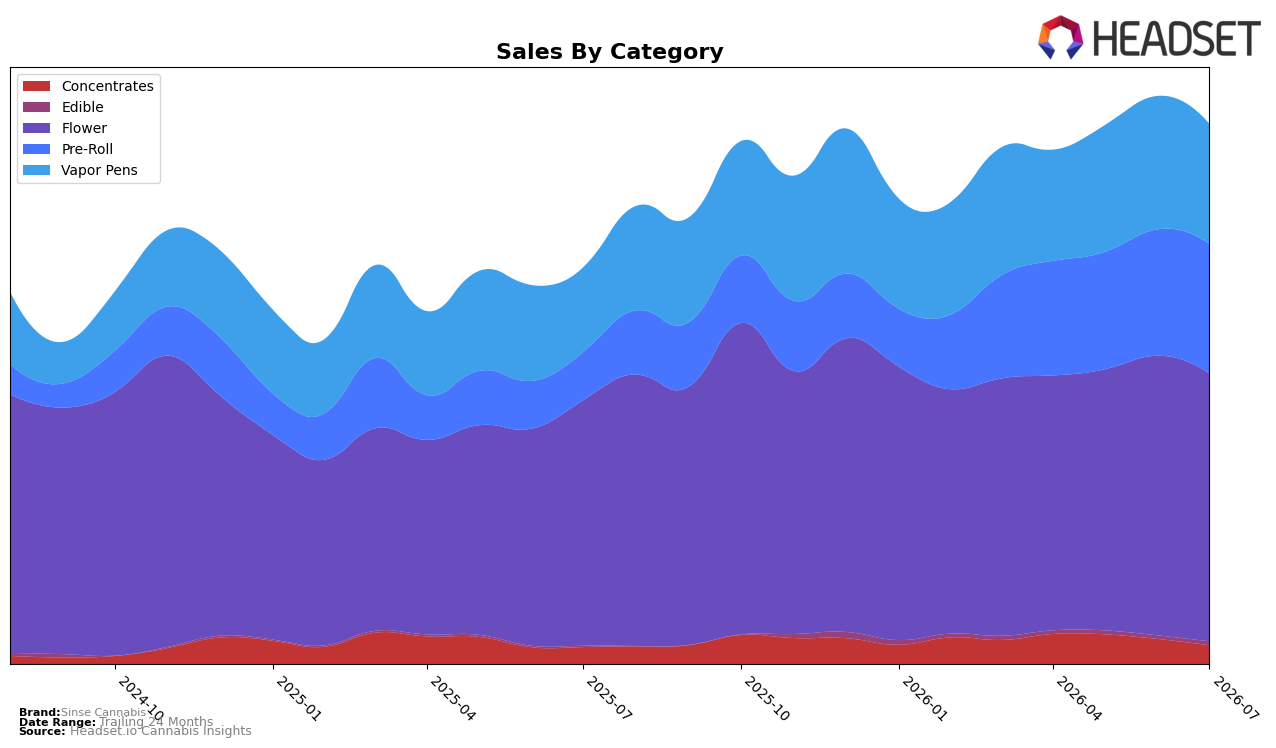

Sinse Cannabis concentrated nearly half of July 2026 sales in Flower at 49.53% share, with Flower up 8.99% year over year but down 4.29% month over month, while Vapor Pens held 22.25% share with 41.86% YoY growth and a 9.89% MoM decline. Pre-Roll expanded to 23.98% share on 169.28% YoY growth and a 2.46% MoM increase, and Edible, though just 0.72% share, posted 196.30% YoY and 10.22% MoM gains; meanwhile Concentrates slipped 24.94% MoM despite 10.54% YoY growth. With the brand ranked 2 in Flower in Missouri and an average price down 17.96% YoY to $15.44, the pattern implies deliberate mix broadening beyond Flower and price recalibration to defend volume while nurturing faster-growing Pre-Roll and Edible lines.

The tilt toward Pre-Roll and Edible—together adding 170–196% YoY growth while Vapor Pens contracted 9.89% MoM—suggests a pivot to formats with quicker trial and replenishment, while buffering Flower’s 4.29% MoM pullback. Holding the number 2 Flower rank in Missouri alongside Pre-Roll’s 2.46% MoM rise indicates the brand is using Flower scale to seed adjacent categories, implying a positioning shift from a Flower-led specialist to a multi-format portfolio where Pre-Roll becomes the growth engine and Vapor Pens serve as a margin counterweight despite near-term MoM softness.

Competitive Landscape

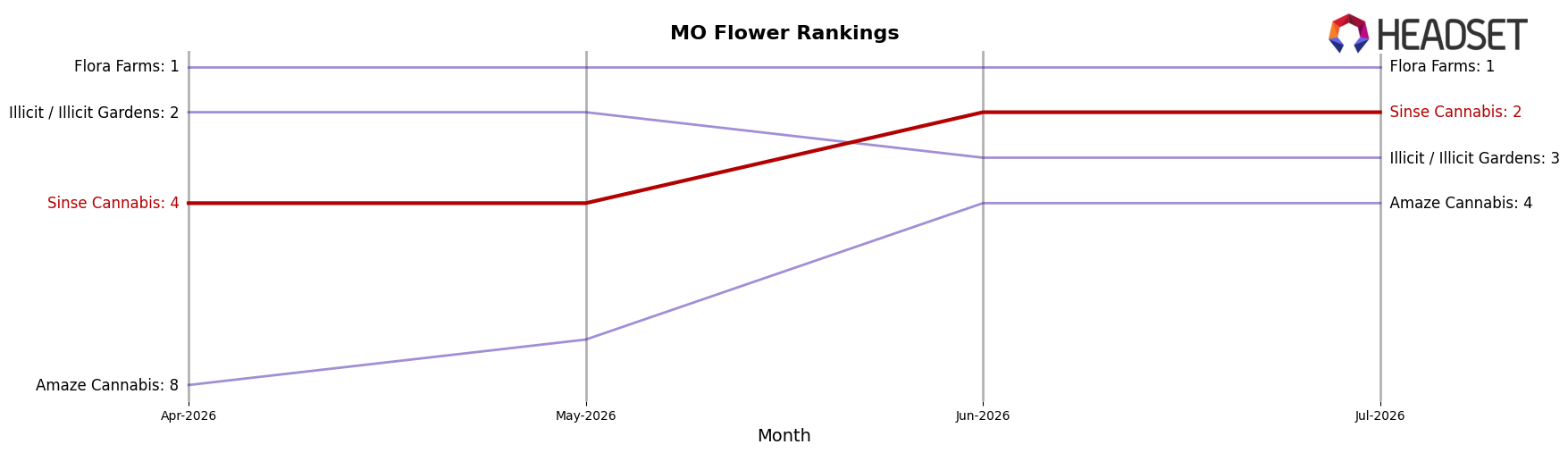

Sinse Cannabis sits at rank #2 in Missouri Flower in July 2026, up two positions from #4 year over year, and two spots higher than its April 2026-like three-month reference at #4; by contrast, Flora Farms held #1 both this month and a year ago while its sales fell 1.3% YoY, and Amaze Cannabis improved its rank from #6 to #4 on 20.6% YoY sales growth. With Illicit / Illicit Gardens stationary at #3 alongside a 12.8% YoY sales decline and Local Cannabis Co. rising from #10 to #5 on 41.8% YoY growth, Sinse Cannabis’s move from #4 to a peak of #2 in July 2026 implies it has closed distance on the category lead while also facing faster-rising challengers immediately below.

Notable Products

Cherry Pie (Bulk) posted the standout movement in July 2026 with a month-over-month gain of 74.5% while Blueberry Muffin (Bulk) slid 11.5% to hold rank 1. Jungle Cookie (Bulk) rose 34.7% at rank 2 as Lemon Royale (Bulk) dipped 5.6% at rank 3, and Flower SKUs occupied six of the top ten positions. The pattern implies a pivot within Flower toward momentum SKUs rather than the long-running leader, signaling assortment recalibration inside the same category.

Across formats, Cherry Pie Pre-Roll 3-Pack (1.5g) advanced 26.4% at rank 5 even as Blueberry Muffin (Bulk) contracted 11.5%, with Pre-Rolls accounting for four of the top ten slots and one SKU generating $225,793. The split between accelerating Cherry Pie across both Flower and Pre-Roll and moderating Blueberry Muffin suggests Sinse Cannabis is steering share toward scalable strains that can travel across formats for July 2026 and beyond.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.