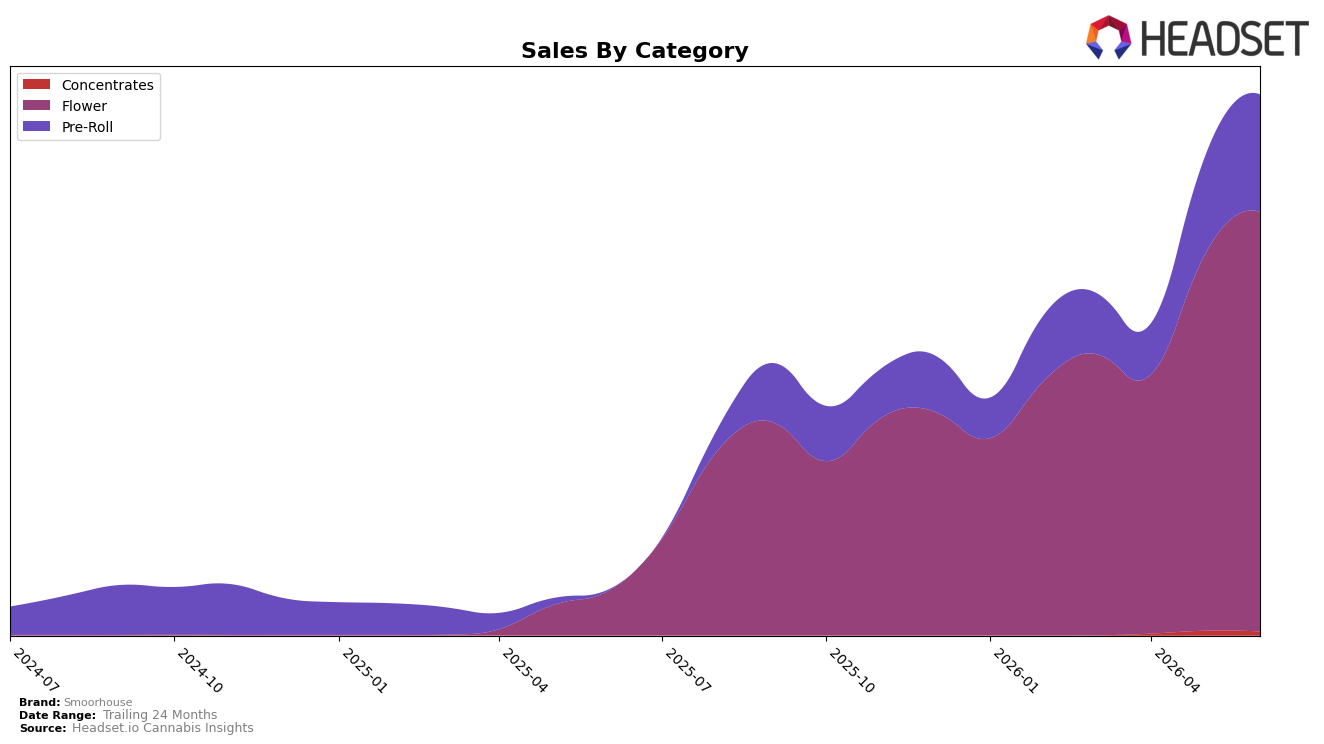

Market Insights Snapshot

In June 2026, Smoorhouse’s mix concentrated 77.59% of sales in Flower with 11.76% MoM growth and 852.90% YoY, while Pre-Roll expanded to 21.71% share with 20.18% MoM and 11,347.87% YoY; Concentrates was 0.71% share with a -18.09% MoM decline and no YoY baseline. Despite an average price down 26.01% YoY to $28.15, unit velocity likely expanded as total brand sales rose 1,100.20% YoY and 1,603.41% over 24 months; this pricing-plus-mix pattern implies Smoorhouse is trading volume for reach, anchored in Flower and accelerating in Pre-Roll.

With Flower at rank 25 in Michigan and an 11.76% MoM uptick alongside a 20.18% MoM lift in Pre-Roll, Smoorhouse is positioned to move from a Flower-led footprint toward a two-pillar portfolio where Pre-Roll serves as the acquisition engine. The 852.90% YoY surge in Flower paired with an 11,347.87% YoY in Pre-Roll indicates penetration gains are outpacing premiumization, and the -18.09% MoM in Concentrates suggests deliberate focus rather than broad category sprawl; net effect, the brand’s share growth is most defensible where rank headroom exists in Flower while Pre-Roll provides faster share pickup potential at lower price points.

Competitive Landscape

Smoorhouse is ranked #25 in MI Flower in June 2026, a climb of 161 positions from #186 in June 2025, and up 14 spots from #39 in March 2026; this is also its peak rank (#25) to date in June 2026. In contrast, High Minded held at #1 year over year but posted a -13.7% sales change, while Goodlyfe Farms moved from #5 to #2 with a 44.1% sales increase, indicating Smoorhouse’s rank surge is occurring alongside leadership stability at the very top and aggressive advancement among mid-top peers. The pattern implies Smoorhouse’s rapid rank compression into the top 25 is more about momentum gain versus entrenched incumbents than share capture from the #1 position, suggesting its near-term trajectory depends on sustaining multi-month rank improvements against faster-rising competitors like Goodlyfe Farms rather than displacing High Minded.

Notable Products

Blueberry Zkittlez Infused Pre-Roll 7-Pack (3.5g) posted the largest move in June 2026 with a +76.5% month-over-month increase while holding rank 4, as Magic Sherblato Infused Pre-Roll 7-Pack (3.5g) slipped -2.1% at rank 1. Magic Sherblato Infused Buds (Bulk) advanced +49.0% to rank 3, and Lemon Cream Cake Infused (3.5g) rose +22.6% at rank 10, while no SKU in the top ten declined more than -2.1%. With four of the top ten coming from Flower and three from Pre-Roll, the mix tilts toward infused formats that are gaining velocity at middle ranks, implying Smoorhouse is shifting traction from a single flagship into a broader infused portfolio that can trade shoppers up the ladder.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.