Market Insights Snapshot

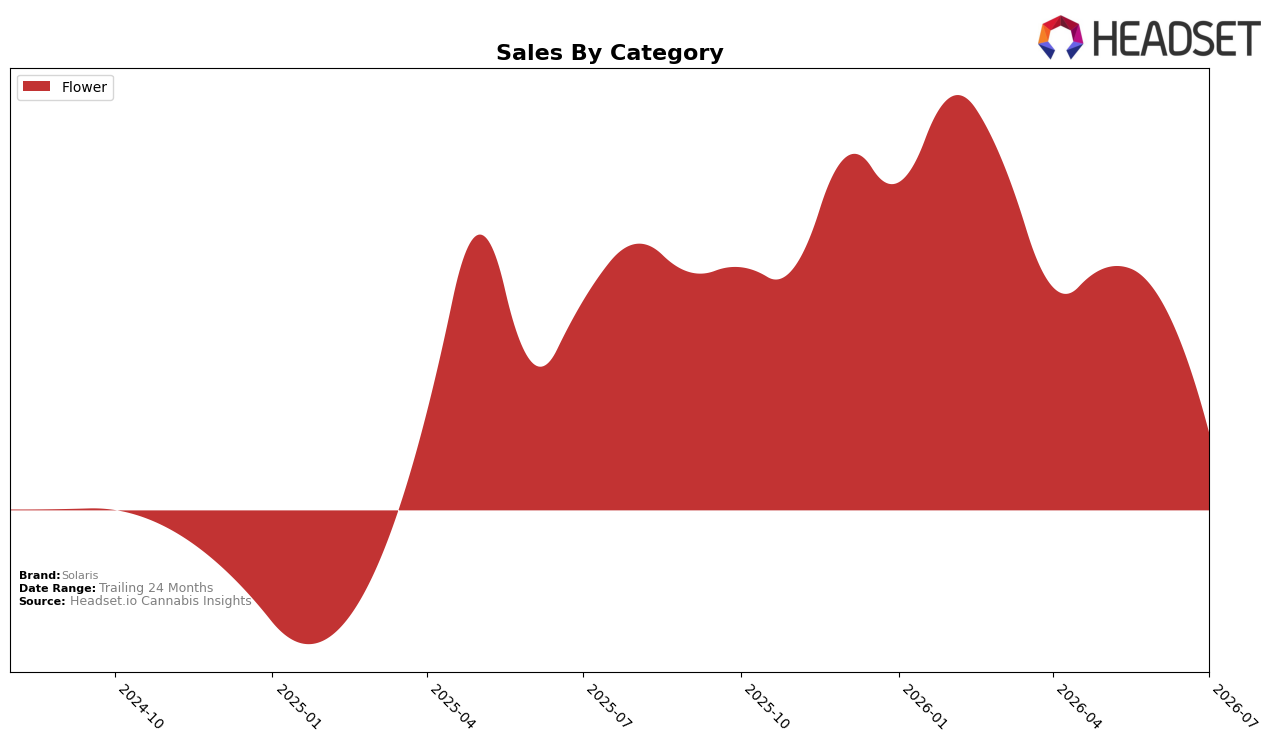

In July 2026, Solaris concentrated 100.0% of sales in Flower, while year-over-year sales fell 62.3% and month-over-month sales declined 63.4%. Average price contracted 39.1% YoY to $14.93, yet rank in Nevada Flower held at position 45, indicating volume erosion outpaced pricing cuts. The pattern implies a single-category dependency that magnifies volatility: with no offset from other categories and a 100.0% mix in Flower, the -62.3% YoY and -63.4% MoM drops indicate demand compression not sufficiently mitigated by the 39.1% price reduction.

The shift toward an all-Flower mix and a 45 rank in Nevada suggests Solaris is competing primarily on price within lower tiers rather than on assortment breadth, given a 39.1% YoY price decline alongside a 62.3% YoY sales contraction. The 63.4% MoM fall paired with a 100.0% category share implies sensitivity to weekly shelf dynamics and promotional cycles; maintaining rank 45 despite steep declines points to stable but thin distribution where volume elasticity is weak at the current $14.93 price point. This configuration implies repositioning is needed toward differentiated SKUs or selective premiumization to reduce exposure to Flower-only volatility and to convert price cuts into measurable share rather than accelerated volume loss.

Competitive Landscape

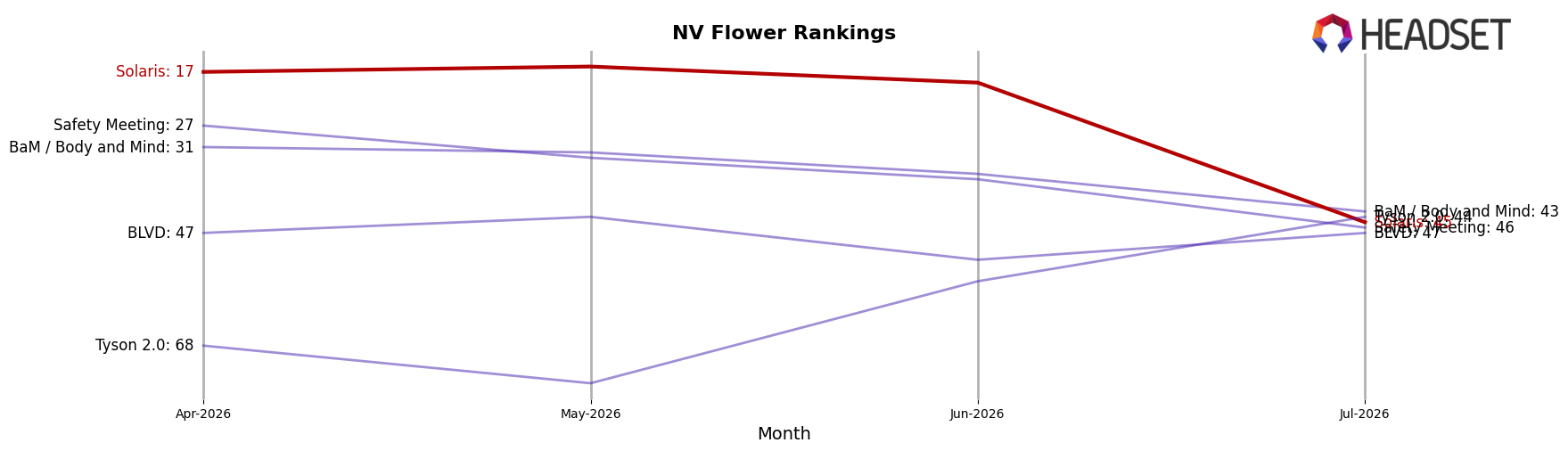

Solaris is currently ranked #45 in NV Flower, down 23 spots year over year from #22, and sliding 28 places since April 2026’s #17 after peaking at #12 in February 2026; meanwhile, STIIIZY climbed from #2 to #1 with 31.5% year-over-year sales growth and RYTHM slipped from #1 to #2 with a 12.7% year-over-year decline, indicating Solaris’s descent is driven more by share consolidation at the top than a broad market lift, and the trajectory implies re-entry into the top 20 will require reversing multi-month rank erosion rather than waiting for competitor retrenchment.

Notable Products

Chemical Cookies (3.5g) plunged 71.7% month over month and slid to rank 6, while Mousse Cake (7g) fell 57.4% to rank 7, signaling a sharp pullback in mid-pack Flower formats even as Jealousy (3.5g) surged 52.2% to claim rank 1. With four of the top ten as Jealousy family SKUs across 1g, 3.5g, and 7g, the category mix is consolidating toward a single strain line as secondary strains contract, and the $30,789 in July 2026 sales for Jealousy (3.5g) concentrates spend at the top of the chart. The pattern implies Solaris is tilting assortment and demand toward a hero strain strategy where Jealousy anchors volume while breadth in other Flower SKUs narrows.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.