Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Kushberry Farms is stocked at 25 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Reno, Carson City, Henderson, and North Las Vegas. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

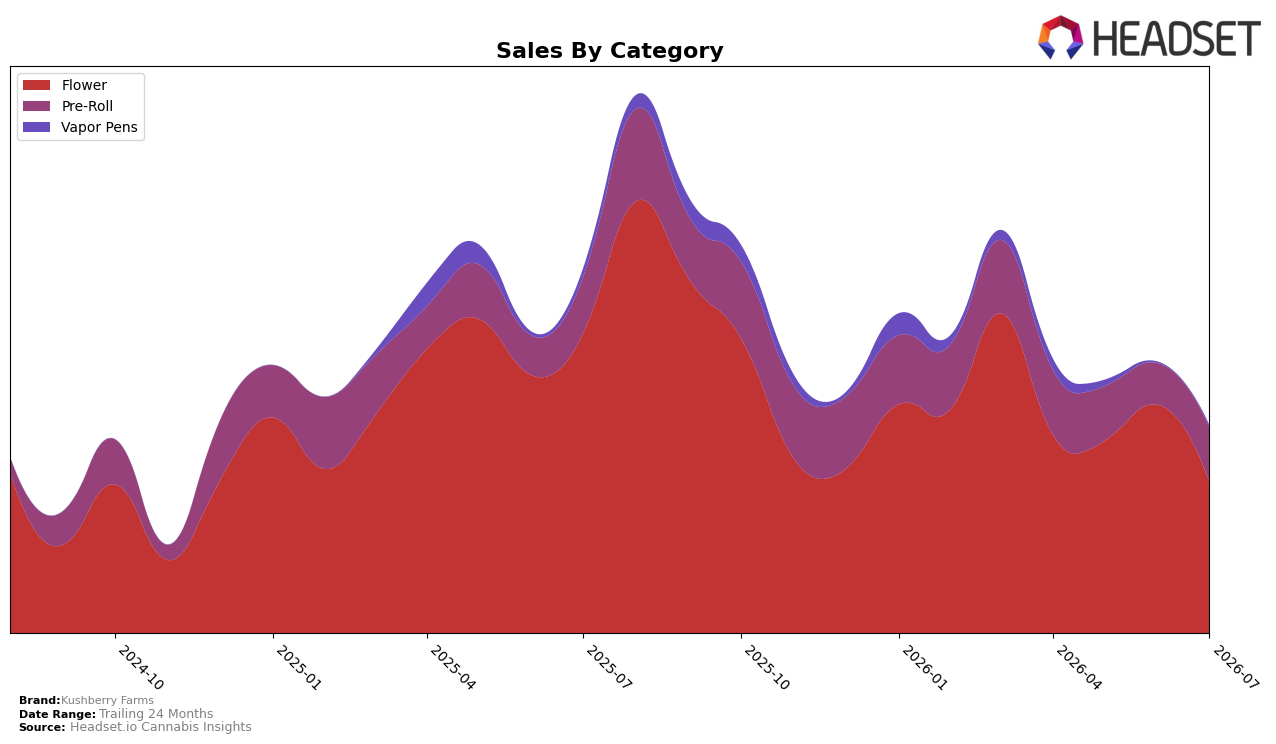

In July 2026, Kushberry Farms’ mix concentrated 72.70% in Flower with a year-over-year decline of 49.79% and a month-over-month drop of 34.00%, while Pre-Roll expanded to 26.39% share with a modest 2.49% YoY decline and a 32.19% MoM increase; Vapor Pens remained marginal at 0.91% share despite a 77.60% YoY decline and a 63.40% MoM rise. Average price fell 18.27% YoY to $13.83 as Flower’s higher ticket averaged $24.78 versus Pre-Roll at $6.20, indicating mix shift toward lower-priced units alongside a sharp pullback in the largest category. The pattern implies a pivot from Flower volume toward Pre-Roll to stabilize unit throughput, with shorter-cycle recovery in Pre-Roll offsetting Flower contraction.

With Flower still the top category yet down 49.79% YoY and 34.00% MoM, and Pre-Roll rising 32.19% MoM to 26.39% share, the brand is tilting toward value-accessible formats that compress price while improving basket frequency. The 63.40% MoM lift in Vapor Pens off a small 0.91% base suggests testing rather than scale, while the overall 43.15% YoY sales decline and 18.27% YoY price reduction point to a repositioning that trades average revenue per unit for share defense in Pre-Roll. The implication is a near-term strategy anchored in Pre-Roll to mitigate Flower volatility, using pricing and pack architecture to regain rank in Nevada while maintaining Flower as the flagship.

Competitive Landscape

Kushberry Farms sits at rank #18 in July 2026 in NV Flower, down 7 positions year over year from #11 and 5 positions versus April 2026’s #13, after previously peaking at #6 in September 2025; in contrast, STIIIZY moved up from #2 to #1 with 31.5% YoY sales growth while RYTHM slipped from #1 to #2 with a 12.7% YoY decline, indicating leadership fluidity at the top that Kushberry Farms has not capitalized on, and FloraVega / Welleaf surged from #24 to #5 alongside a 299.7% YoY sales increase, underscoring that substantial upward mobility is occurring even as Kushberry Farms trends the opposite direction; the rank trajectory implies market share is consolidating around faster-advancing rivals, and without a reversal in momentum Kushberry Farms risks sliding from mid-tier presence toward lower-visibility status.

Notable Products

Dutch Hawaiian (3.5g) posted the steepest decline at -25.3% while holding rank 4, contrasting with Dutch Hawaiian Pre-Roll (1g) up 45.0% at rank 1, which signals substitution within the same strain across formats rather than category-wide weakness. Kush Mints Pre-Roll (1g) rose 11.5% at rank 2 while MAC 1 (3.5g) in Flower edged up 5.2% at rank 7, and six of the top ten are Pre-Roll SKUs, indicating consumer momentum tilting toward ready-to-smoke options over packaged Flower. With MAC 1 Pre-Roll (1g) only down 3.3% at rank 10 against these shifts, the mix points to Kushberry Farms leaning into Pre-Rolls to stabilize ranks and recapture dollars migrating from Flower to smaller-ticket formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.