Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Soulshine Cannabis is stocked at 89 licensed dispensaries across Washington, with the deepest coverage in Tacoma, Seattle, Everett, Olympia, and Spokane. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

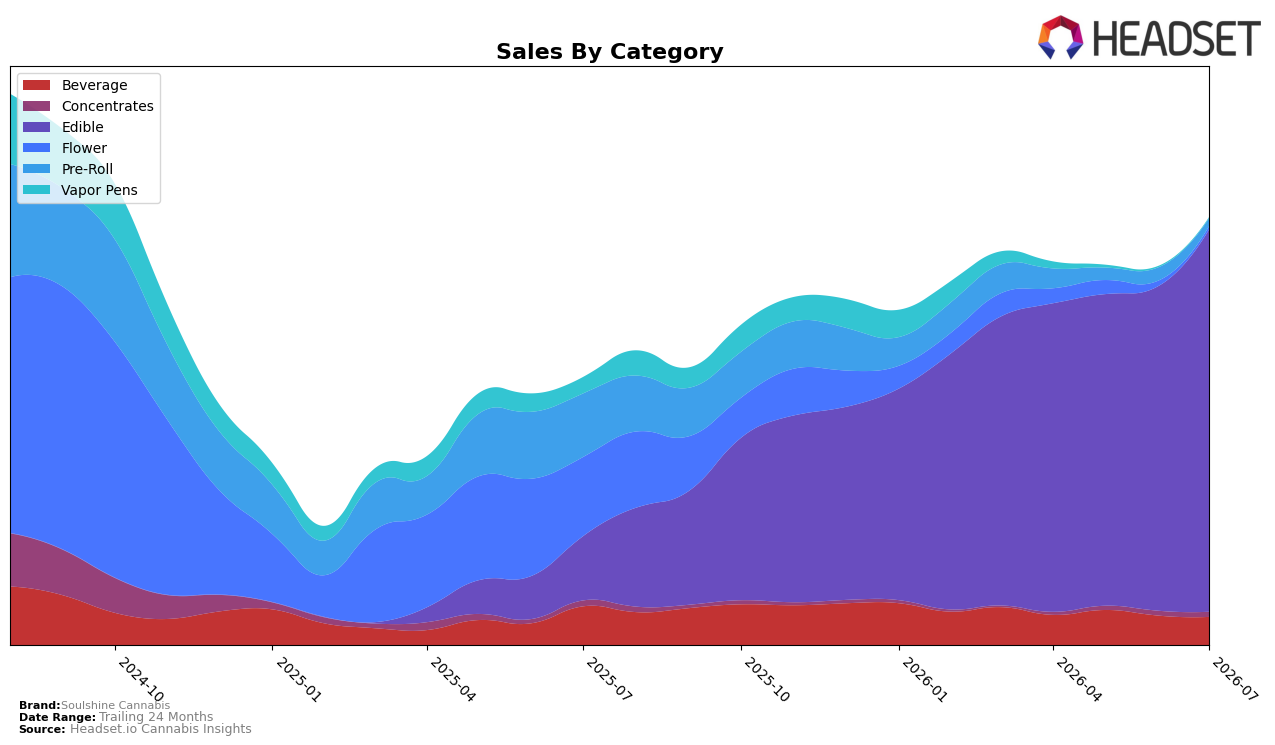

In July 2026, Soulshine Cannabis concentrated 89.65% of sales in Edible, up 17.93% month over month and 498.43% year over year, while Beverage held 6.56% share with a -4.69% MoM decline and -27.40% YoY contraction. Legacy inhalables receded: Pre-Roll fell -40.77% MoM and -87.87% YoY to 1.80% share, and Flower dropped -41.82% MoM and -96.17% YoY to 0.71% share; Vapor Pens also slid -36.51% MoM and -95.75% YoY to 0.16% share. Concentrates was a small counterpoint at 1.12% share with +6.20% MoM despite a -13.86% YoY dip, and the brand’s average price rose 9.15% YoY to $11.66. The mix shift implies Soulshine Cannabis has pivoted decisively into Edible as the primary growth engine, using price and assortment to expand within a single category while de-emphasizing inhalables.

The Edible-heavy profile aligns with a July 2026 rank of 15 in Edible within Washington, suggesting a middle-of-pack footprint where +17.93% MoM category growth can translate to further share capture if sustained, but where -27.40% YoY in Beverage limits cross-category reinforcement. With brand sales up 60.16% YoY against a -35.24% 24‑month trend, the rapid Edible surge must offset deep declines in Flower (-96.17% YoY) and Vapor Pens (-95.75% YoY), and the +6.20% MoM in Concentrates offers a narrow hedge. The pattern implies Soulshine Cannabis is trading breadth for depth: concentrating resources on Edible to gain rank and pricing power while accepting lower presence in underperforming inhalable segments.

Competitive Landscape

Soulshine Cannabis ranks #15 in Washington Edible in July 2026, improving 14 positions from #29 year over year and edging up 2 spots from #17 in April 2026, while also marking a peak rank of #15 in July 2026; by contrast, Wyld held #1 both year over year and in July 2026 with +7.99% sales YoY, and Craft Elixirs slipped from #4 to #5 with -8.01% sales YoY, indicating Soulshine Cannabis is closing distance on mid-tier rivals despite a stable top tier.

Notable Products

Sun - CBD/CBG/THC 3:2:1 Watermelon Hash Rosin Gummies 10-Pack (300mg CBD, 200mg CBG, 100mg THC) posted the steepest movement in July 2026 with a -6.27% month-over-month decline while holding rank 7, contrasting with Moon - CBD/CBN/THC 3:2:1 Mango Solventless Gummies 10-Pack (300mg CBD, 200mg CBN, 100mg THC) up 44.55% at rank 2 and Moon - CBD/CBN/THC 3:2:1 Blueberry Gummies 10-Pack (300mg CBD, 200mg CBN, 100mg THC) up 18.83% at rank 1. Seven of the top ten are Moon or Sun 3:2:1 gummies variants, with Moon units concentrated in CBN-led formulations and Sun units in CBG-led formulations, as ranks 1–6 are all Edibles and include gains of 30.75% at rank 5 and 25.38% at rank 4. The mix shows CBD/CBN-weighted Moon SKUs outpacing CBD/CBG-weighted Sun SKUs, implying Soulshine Cannabis is being pulled toward sleep and unwind use cases over daytime formulations.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.