Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

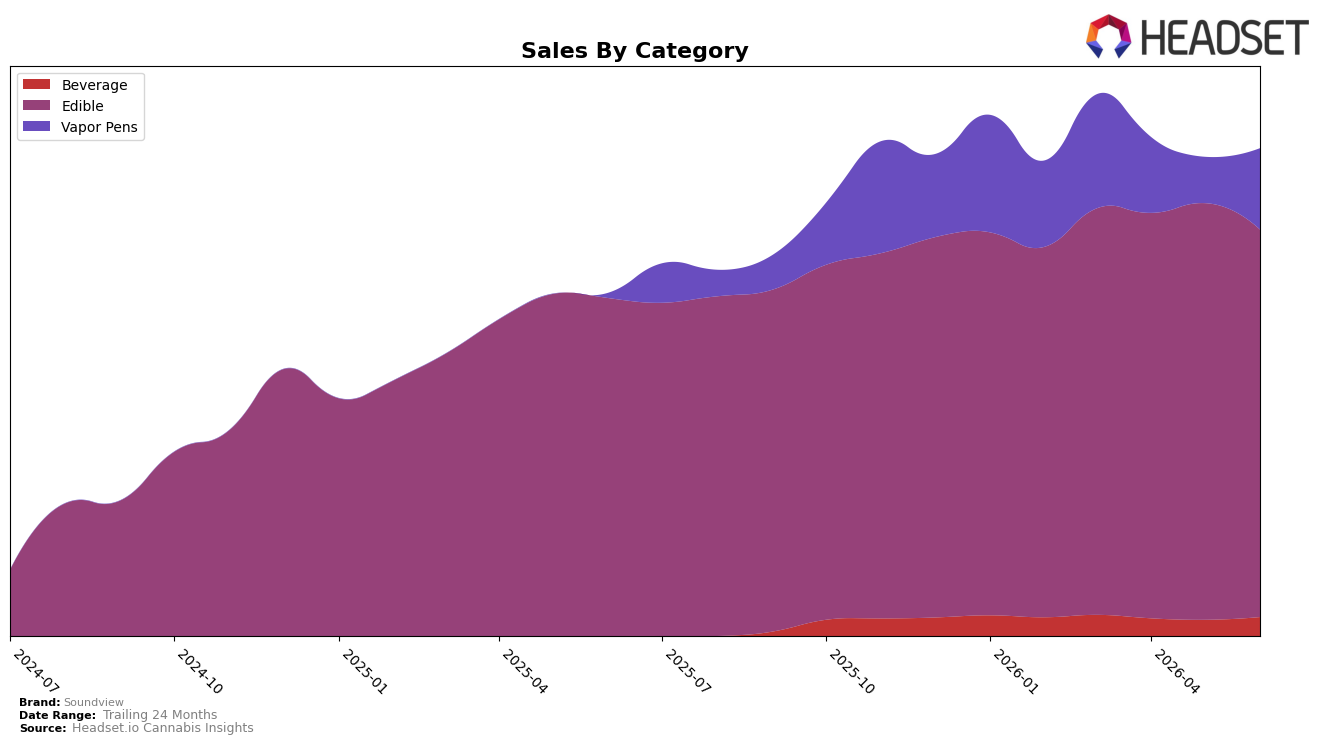

Edible remains the anchor at 79.49% share with 14.68% YoY growth but a -7.00% MoM pullback, while Vapor Pens scaled to 16.63% share on 1,558.60% YoY and 76.18% MoM growth; Beverage is still small at 3.89% share with 16.94% MoM momentum and no YoY comp. The average price fell -6.45% YoY to $25.64 even as brand sales rose 42.23% YoY, and in Connecticut Edible rank sits at 1, indicating volume expansion outpaced price compression. The pattern implies Soundview is using a lower effective price point in Edible to defend a rank-1 position while seeding a second growth pillar in Vapor Pens, with June’s -7.00% MoM in Edible offset by a 76.18% MoM surge in Vapor Pens.

The shift toward a two-pillar mix changes positioning from a single-category leader to a portfolio play: with Edible at 79.49% share and rank 1 in Connecticut, incremental gains now rely on Vapor Pens’ 16.63% share and 1,558.60% YoY expansion, plus Beverage’s 16.94% MoM lift. Price elasticity is at work: a -6.45% YoY average price decline alongside 42.23% YoY brand sales growth suggests demand capture via accessible pricing in Edible while premium-priced Vapor Pens at a $56.77 average support mix-driven revenue per buyer. The implication is to preserve Edible scale despite a -7.00% MoM dip by reallocating activation to Vapor Pens’ high-velocity cohorts, using Beverage as a low-risk test bed to diversify without diluting the rank-1 Edible position.

Competitive Landscape

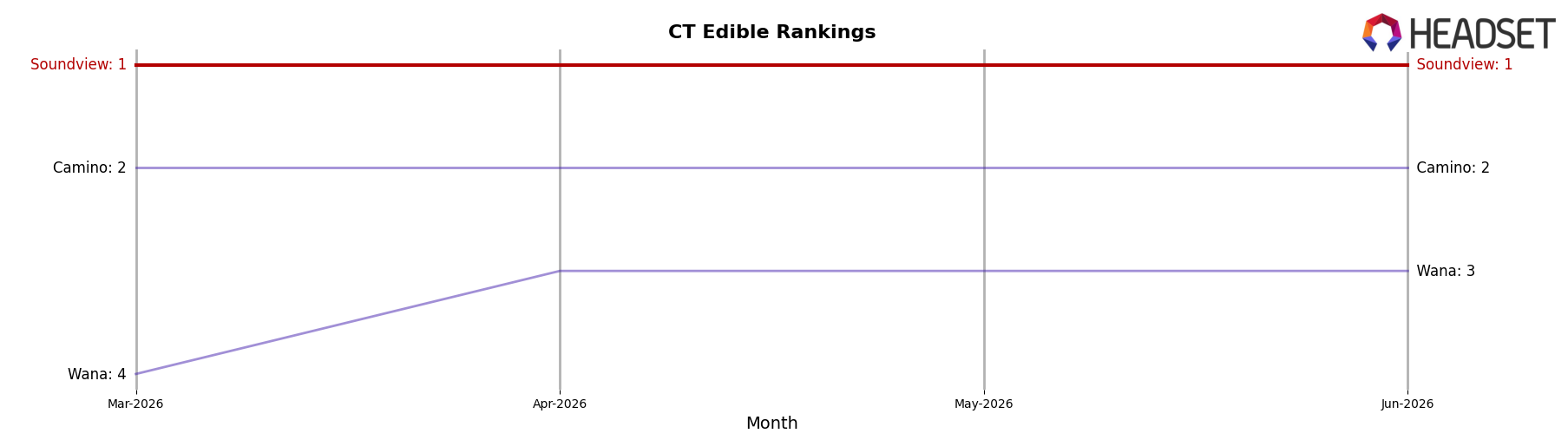

Soundview sits at rank #1 in CT Edible in June 2026, up 1 position year over year from #2, and holding #1 for the past three months, implying sustained share consolidation; meanwhile, Camino climbed from #6 to #2 with a 289.8% year-over-year sales increase, while Encore Edibles fell from #1 to #4 alongside a 53.1% sales decline, indicating that Soundview’s ascent has coincided with competitor churn rather than broad category expansion, so the trajectory implies Soundview’s lead is vulnerable to fast-rising challengers if their momentum persists.

Notable Products

Sativa Blood Orange Gummies 20-Pack (100mg) posted the steepest move in June 2026 with a -26.9% MoM slide to rank 3, while the leading CBN/THC 5:1 BlueZZZberry Gummies 20-Pack (500mg CBN, 100mg THC) dipped -7.9% at rank 1. Pink Lemonade Live Resin Gummies 20-Pack (100mg) surged +49.5% to rank 2, narrowing the gap with the leader on a single-month basis despite BlueZZZberry’s larger dollar base of $211,925. With eight of the top ten in Edibles, the concentration alongside a -20.8% drop for THC/CBN 2:1 G'Night Grape Gummies 20-Pack (100mg THC, 50mg CBN) and a -15.4% decline for Peach RSO Gummies 20-Pack (100mg) implies a maturing sleep/premium niche while fast-rising fruit SKUs pull share within the same category. The mix points to Soundview tilting toward flavor-led, daytime-friendly edibles as the growth engine, while legacy sleep formats stabilize at lower velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.