Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

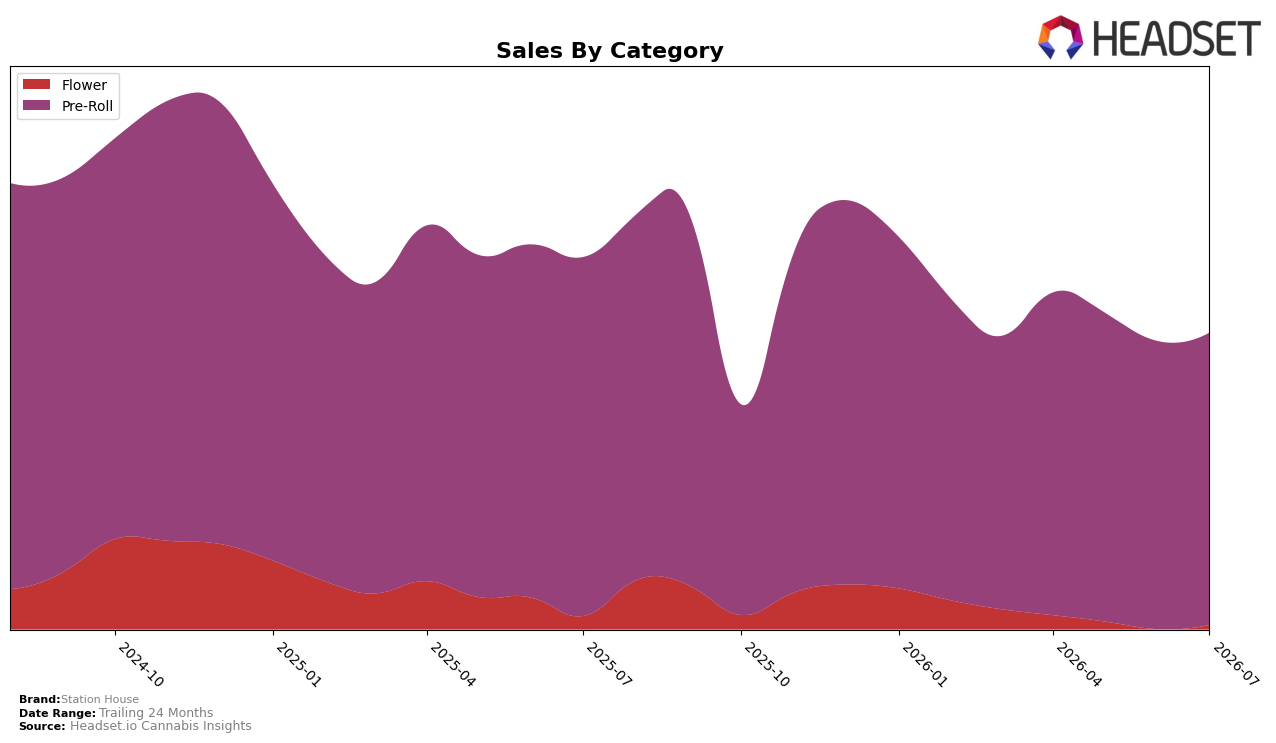

In July 2026, Pre-Roll held 87.09% share with year-over-year change of -16.47% and month-over-month movement of +1.28%, while Flower represented 12.91% share with year-over-year change of -15.27% and month-over-month gain of +9.13%. Despite a brand-level year-over-year sales change of -16.31% and an average price shift of -2.26%, the weight of Pre-Roll at 87.09% means small mix or velocity changes there disproportionately drive overall outcomes; meanwhile, Flower’s smaller base amplifies its +9.13% month-over-month growth without offsetting Pre-Roll’s -16.47% year-over-year drag. The pattern implies a reliance on a single category that limits recovery speed, with incremental Flower gains unable to materially counterbalance Pre-Roll’s year-over-year contraction.

With Pre-Roll ranked 13 in British Columbia and holding 87.09% of the brand’s mix, positioning is tied to mid-pack visibility where modest rank movement could hinge on sustaining the +1.28% month-over-month uptick while mitigating the -16.47% year-over-year decline. The -2.26% average price change alongside a 24-month sales change of -19.42% suggests pricing levers alone are unlikely to shift trajectory, so the +9.13% month-over-month Flower growth becomes a testing ground to diversify beyond Pre-Roll’s volatility and support incremental rank gains from the 13 position.

Competitive Landscape

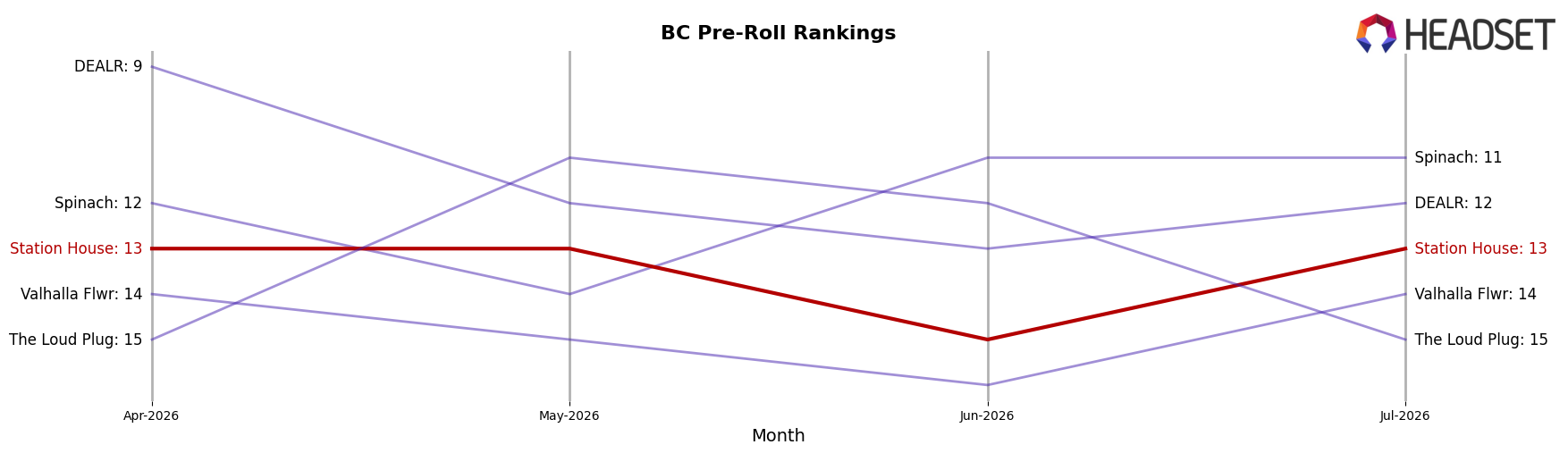

Station House ranks #13 in BC Pre-Roll in July 2026, down 4 places year over year from #9, and flat versus April 2026 at #13; the brand’s historical ceiling of #5 in January 2025 contrasts with today’s position, indicating a 8-rank slide from peak to current. Meanwhile, General Admission held #1 year over year at #1 despite a -22.3% YoY sales decline, and Back Forty / Back 40 Cannabis surged from #17 to #2 on +215.2% YoY sales, while Weed Me stayed in the top three despite a -6.8% YoY sales dip; against this backdrop, Station House’s -4 rank change YoY and 0 change over three months imply share is being redistributed upward to fast risers and incumbents, signaling that without a catalyst the brand’s trajectory points to mid-pack persistence rather than re-entry into the top 10.

Notable Products

White Widow Pre-Roll (0.5g) posted the steepest movement in July 2026 with a -24.1% month-over-month drop while sliding to rank 9, contrasting with Blue Dream Pre-Roll (0.5g) inching up +2.6% to hold rank 1. Northern Lights Pre-Roll (0.5g) declined -1.9% at rank 2 as Sour Diesel Pre-Roll (0.5g) climbed +13.2% within the top 10, indicating share is rotating from mid-pack staples to a smaller set of leaders. Eight of the top ten are Pre-Roll SKUs with mixed momentum ranging from -5.3% to +13.2%, and Trainwreck Pre-Roll (0.5g) advanced +11.2% at rank 8, implying the portfolio is concentrating velocity in a few high-frequency strains rather than broad-based gains. This pattern suggests Station House is leaning into a leader-led strategy in July 2026, prioritizing sustained rank defense on flagship Blue Dream while allowing underperformers like White Widow to cycle down.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.