Jan-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

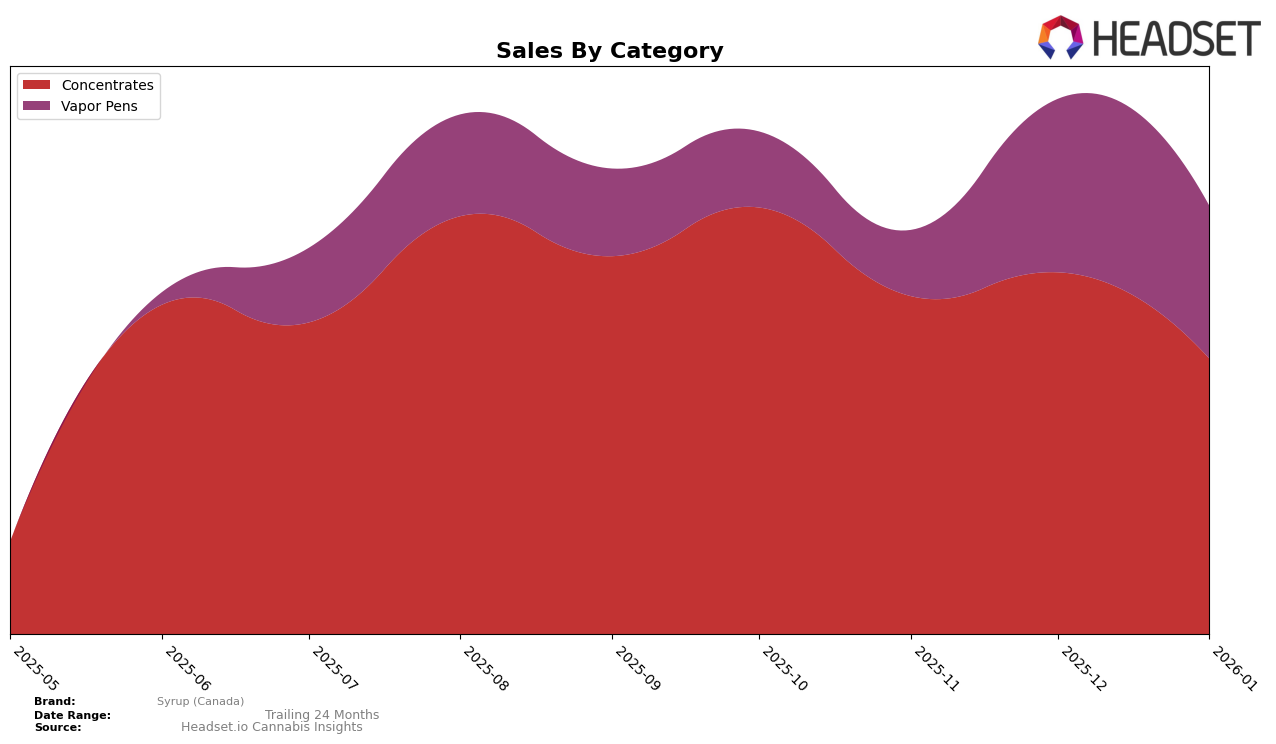

Syrup (Canada) has shown varied performance across different categories and regions. In the Concentrates category within Alberta, Syrup has experienced a decline in rankings from 18th in October 2025 to 30th by January 2026. This downward trend is mirrored by a significant decrease in sales over the same period, suggesting potential challenges in maintaining market share or customer interest. Notably, Syrup was not ranked in the top 30 for Vapor Pens in Alberta until January 2026, when it entered at 70th, indicating an area of potential growth or a new market entry strategy.

In Ontario, Syrup (Canada) has maintained a more stable presence in the Concentrates category, with rankings fluctuating between 40th and 45th from October 2025 to January 2026. This suggests a relatively steady performance, although there is room for improvement to break into higher ranks. Despite these modest rankings, sales figures in Ontario show a positive trend, with a noticeable increase from November to December 2025, hinting at growing consumer interest or effective promotional efforts during that period. The consistent presence in Ontario contrasts with the challenges faced in Alberta, highlighting the importance of regional strategies in the cannabis market.

Competitive Landscape

In the Ontario concentrates market, Syrup (Canada) has shown a fluctuating performance in the rankings from October 2025 to January 2026. Despite a drop from 42nd to 45th in November, Syrup (Canada) managed to recover slightly to 40th in December and maintained a close position at 41st in January. This indicates a resilience in maintaining its market presence amidst competitive pressures. Notably, Lord Jones consistently ranked higher than Syrup (Canada), although it experienced a slight decline from 35th to 38th over the same period. Meanwhile, Jublee showed a strong upward trend, improving its rank from 43rd to 39th, potentially posing a threat to Syrup (Canada)'s market share. Tuck Shop and Dom Jackson also represent significant competition, with Tuck Shop experiencing a downward trend, while Dom Jackson entered the top 50 in December and improved further in January. These dynamics suggest that while Syrup (Canada) is holding its ground, it faces increasing competition from both established and emerging brands, necessitating strategic adjustments to enhance its competitive edge.

Notable Products

In January 2026, Syrup (Canada) maintained Chem Bomb Live Terp (1g) as the top-performing product in the Concentrates category, holding the number one rank consistently from previous months, despite a sales decline to 1810 units. Velvet Lightning Live Resin Terp Cartridge (0.95g) showed a significant improvement, climbing to the second position from fourth in December 2025, with sales increasing to 442 units. Little Tokyo Live Terp Dab (1g) remained stable in the third position, while Zuper Kush Live Terp Dispenser (1g) dropped to fourth place from its consistent second rank in prior months. Little Tokyo Live Resin Terp Cartridge (2g) entered the ranks in December 2025 and secured the fifth position in January 2026. These shifts indicate dynamic changes in consumer preferences within the Vapor Pens and Concentrates categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.