Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

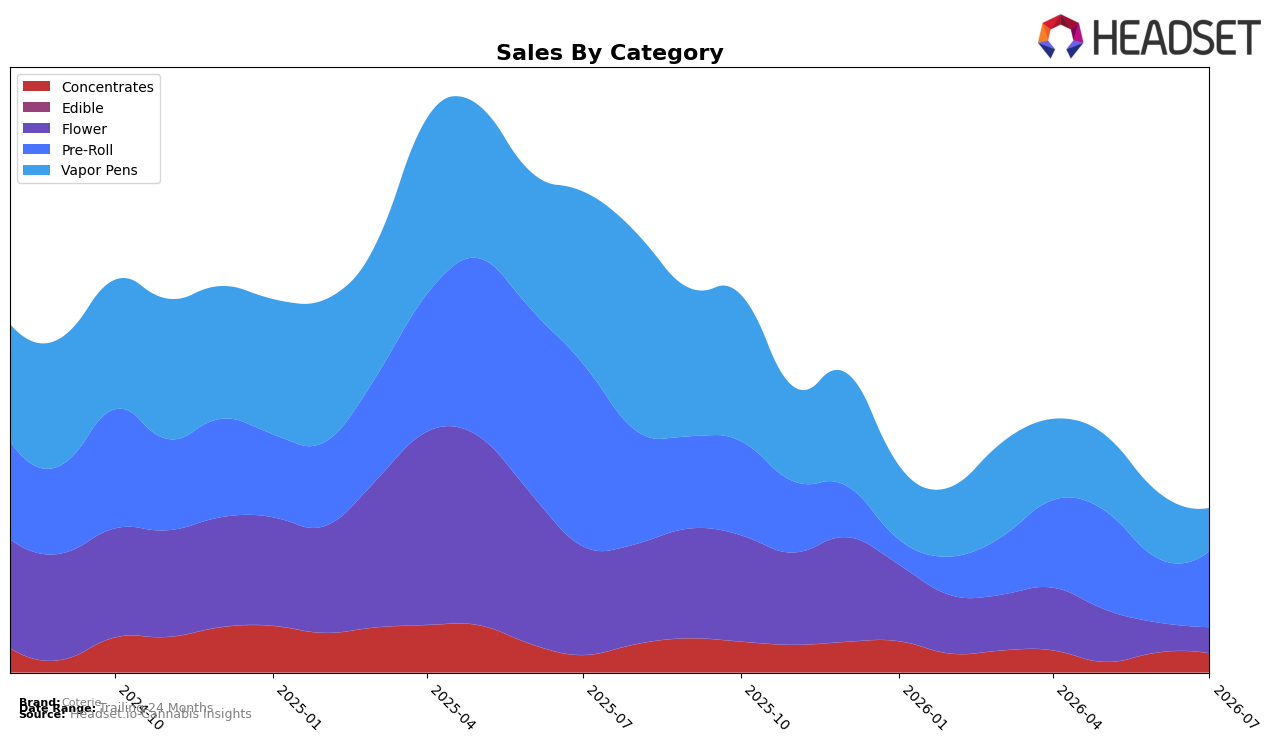

In July 2026, Coterie’s category mix concentrated in Pre-Roll at 46.26% share with month-over-month growth of 18.38% but year-over-year decline of 58.44%, while Vapor Pens fell to 26.38% share with a 34.62% MoM drop and a 74.90% YoY contraction. Flower held 15.75% share with a 13.09% MoM decline and a 76.18% YoY decline, contrasted by Concentrates at 11.61% share posting a 9.99% YoY gain but a 4.04% MoM dip. With overall average price down 10.21% YoY and Pre-Roll average price at 16.47 versus Vapor Pens at 36.21, the mix shift toward lower-priced Pre-Roll and away from higher-priced Vapor Pens implies margin pressure coinciding with a brand-level sales decline of 65.88% YoY.

The pivot toward Pre-Roll alongside a small but growing YoY pocket in Concentrates (9.99%) suggests a defensive reweighting toward accessible formats while deprioritizing premium-priced Vapor Pens, which contracted 34.62% MoM and 74.90% YoY; this pattern likely positions Coterie as value-leaning rather than premium within inhalables. Holding rank 62 in Pre-Roll in Alberta while Pre-Roll is up 18.38% MoM but down 58.44% YoY indicates tactical recovery potential within the largest category share, yet sustained share loss risk if Vapor Pens’ 26.38% share continues to erode; the net effect is a positioning that trades short-term volume stability for long-term pricing power.

Competitive Landscape

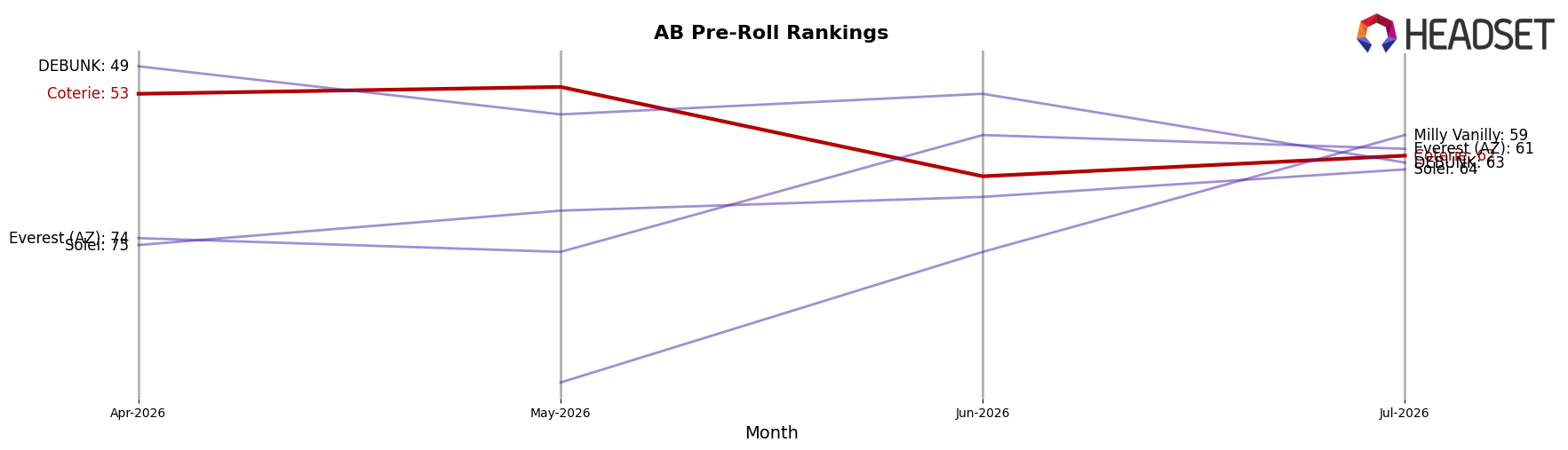

Coterie sits at rank #62 in AB Pre-Roll for July 2026, sliding 29 positions year over year from #33, and down 9 spots versus April 2026 when it was #53; this contrasts with General Admission holding at #1 year over year despite a -14.5% sales change, and Back Forty / Back 40 Cannabis moving up to #2 from #6 with +34.3% sales growth. The gap widened further as Space Race Cannabis improved to #3 from #2 while posting a -37.9% sales decline, and Thumbs Up Brand climbed to #5 from #19 on +138.3% sales, signaling that Coterie’s fall from its July 2025 peak of #33 to #62 is less about overall market contraction and more about losing share to faster risers, implying the current trajectory risks entrenching Coterie below the top 50 unless retention or assortment changes redirect momentum.

Notable Products

Strawberry Gary Liquid Diamond Infused Pre-Roll (1g) posted the largest move in July 2026 with +138.8% MoM to rank 2, while Double Mango Liquid Diamonds Disposable (1g) fell -38.5% to rank 4, a split that shifts share toward inhalables without cartridges. Two pre-rolls landed in the top five with +138.8% and +135.6% MoM for ranks 2 and 5 respectively, and three of the top ten are Pre-Roll SKUs overall, implying a pivot toward infused formats at the expense of Vapor Pens.

Within Pre-Rolls, Strawberry Gary Pre-Roll 3-Pack (1.5g) surged +135.6% MoM at rank 5 as Grape Gotti#12 Pre-Roll 3-Pack (1.5g) declined -25.5% at rank 6, a substitution pattern inside the format. Flower held mixed footing with Strawberry Gary (7g) up +7.7% at a shared rank 8 while Grape Gotti #12 (7g) dropped -35.2% at rank 9, and the category’s combined presence at ranks 8–9 with roughly $38,901 suggests mid-pack stability but not the month’s growth engine.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.