Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

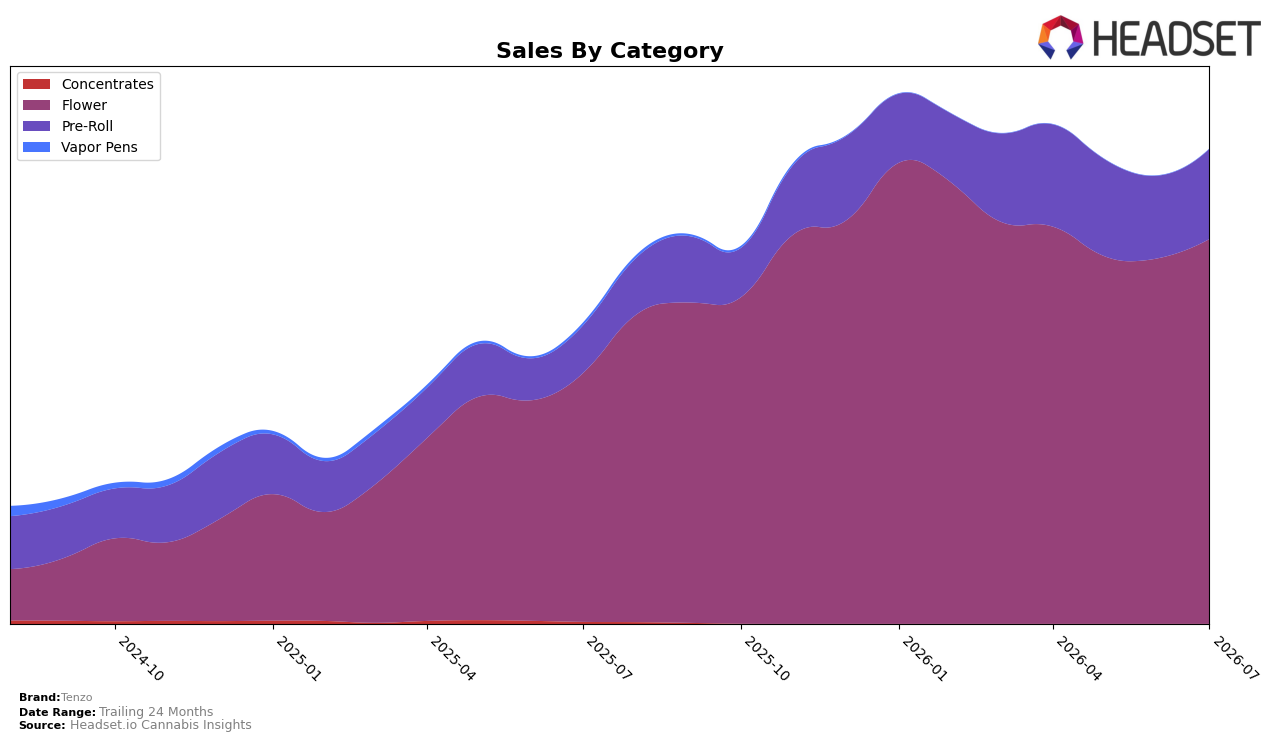

In July 2026, Tenzo’s mix is concentrated in Flower at 81.07% share with 54.72% year-over-year growth and 5.27% month-over-month expansion, while Pre-Roll holds 18.93% share with 89.96% year-over-year growth and 9.15% month-over-month momentum. The brand’s average price fell 17.76% year over year to $31.18 as Flower averaged 45.31 and Pre-Roll averaged 13.35, indicating mix and pricing are pulling in different directions. Tenzo’s Flower rank is 12 in Ontario, pairing an up-mix category with a double-digit rank position; the pattern implies volume-led gains are outpacing price compression, but the category split keeps scale tied to Flower cycles.

With Pre-Roll growing faster than Flower on both a year-over-year basis (89.96% vs. 54.72%) and month over month (9.15% vs. 5.27%), the mix is inching toward a two-pillar model despite Flower still carrying 81.07% of sales. The 17.76% decline in average price alongside a 57.94% brand sales lift signals elasticity and trade-down acceptance, while maintaining a 12 rank in Ontario Flower anchors visibility. The pattern implies Tenzo can lean into Pre-Roll to diversify growth without sacrificing Flower scale, using lower-price pack architecture to protect share if Flower pricing tightens further.

Competitive Landscape

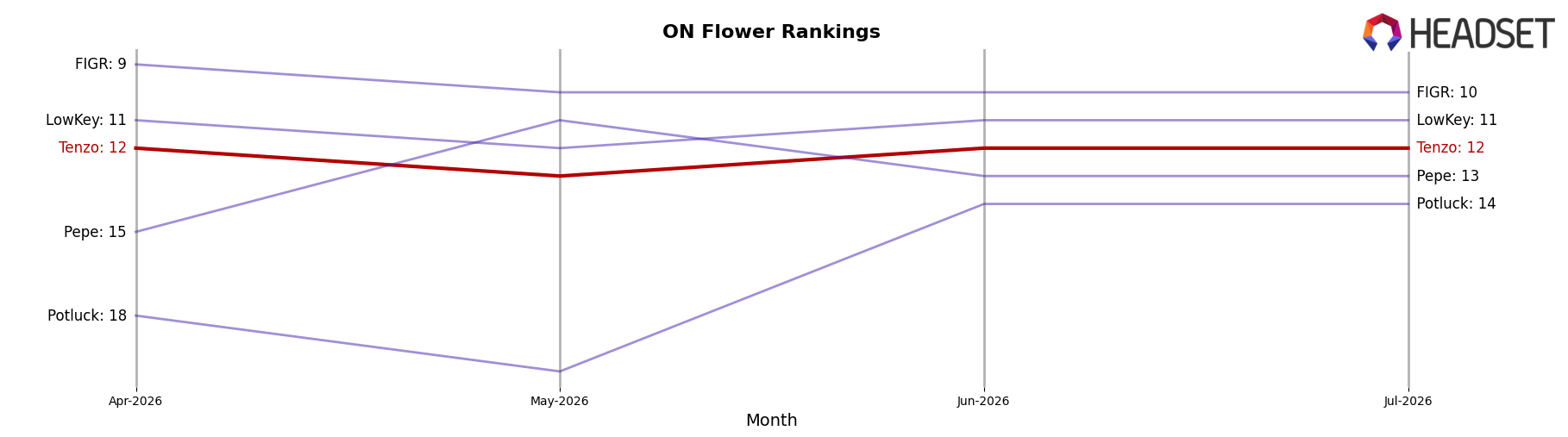

Tenzo sits at rank #12 in ON Flower in July 2026, improving 13 positions from #25 year over year, while holding flat versus three months ago at #12; the brand’s peak of #10 in February 2026 indicates a 2-rank slide from that high. In the same period, Shred moved from #2 to #1 with a 17.23% YoY sales increase, and Spinach climbed from #4 to #2 with 31.07% YoY growth, whereas Back Forty / Back 40 Cannabis fell from #1 to #4 as sales declined 5.44%. The mix of Tenzo’s 13-rank YoY advance alongside a 2-rank retreat from its February 2026 peak implies momentum has cooled recently, suggesting the next phase hinges on reclaiming share from top-three incumbents that are still ascending.

Notable Products

Midnight Maraschino Infused Pre-Roll (1g) posted the steepest move in July 2026 with a -23.98% month-over-month decline at rank 9, while Pop Drop & Roll Milled (3.5g) slid -15.72% at rank 6, indicating weakness in value-oriented or novelty segments despite top-tier placement. In contrast, Fun Trip Milled (7g) grew 8.70% to hold rank 1 and Big Smallz (14g) jumped 33.20% at rank 3, and with six of the top ten being Flower SKUs this concentration points to a category tilt that is widening the gap over softer Pre-Roll trends. Pink Passionfruit & Peach Infused Pre-Roll (0.5g) was flat at +0.37% while Red Bottoms Distillate Infused Pre-Roll (0.5g) gained 15.50% at rank 7, suggesting mixed Pre-Roll momentum against steadily rising flagship Flower where Biggie Smalls (14g) stayed in the top ten at rank 10 despite a -3.39% dip. Taken together, the mix implies Tenzo is consolidating around larger-pack Flower value and milled formats, directing assortment and pricing toward high-velocity Flower while letting selective Pre-Rolls play a supporting role.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.