Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

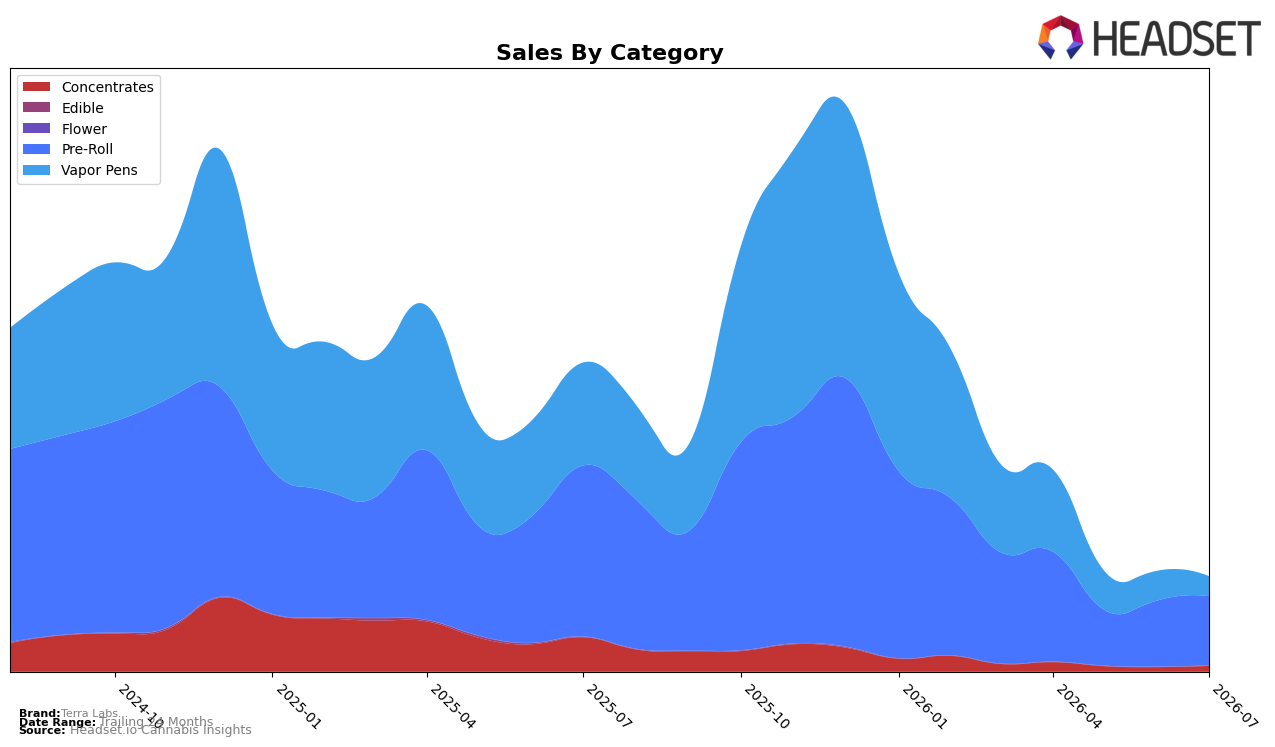

In July 2026, Terra Labs concentrated 73.07% of sales in Pre-Roll with a 4.52% month-over-month lift, while Vapor Pens fell to 20.93% share with a 33.03% MoM decline; Concentrates held 6.00% share with a 28.00% MoM increase. Year over year, Pre-Roll was down 59.65% versus Vapor Pens down 80.79% and Concentrates down 83.51%, and average price across the brand decreased 5.87% while Pre-Roll pricing sat at $25.45. The skew toward Pre-Roll alongside divergent MoM moves implies Terra Labs is consolidating volume in one anchor category while ceding breadth, with category volatility reshaping mix faster than overall brand sales, which fell 69.39% YoY.

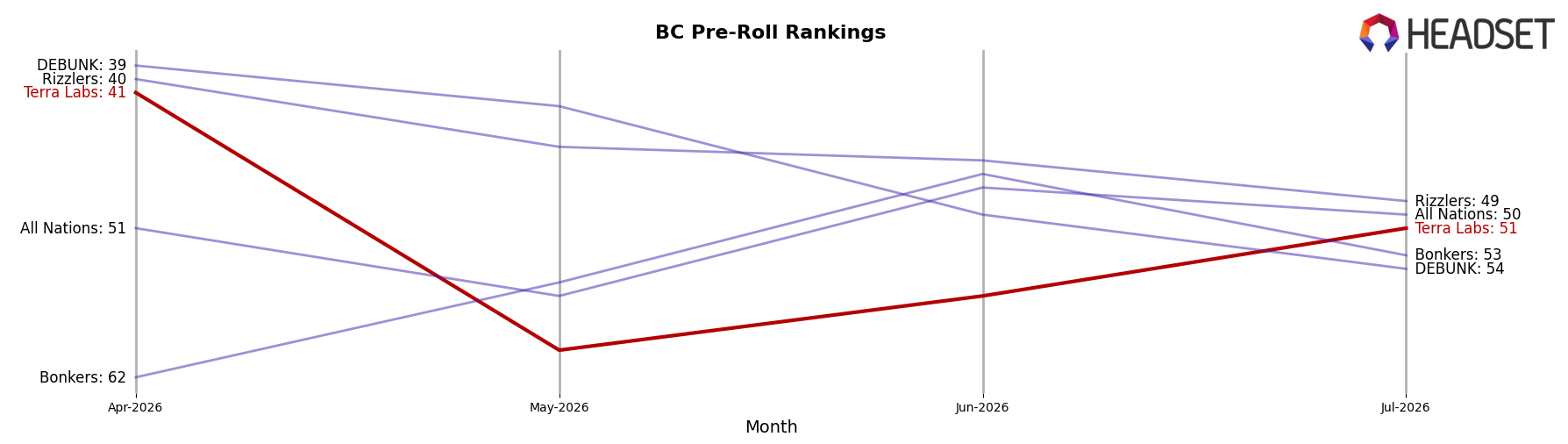

Positionally, the brand’s 51 rank in British Columbia Pre-Roll and a 73.07% mix weight indicate reliance on a mid-pack placement where small share gains matter more than portfolio expansion; a 4.52% MoM uptick in the largest category offsets a 33.03% MoM pullback in Vapor Pens. With Vapor Pens contracting 80.79% YoY versus Pre-Roll at 59.65% YoY and Concentrates rebounding 28.00% MoM from a low base, the pattern points to a price-sensitive, single-category posture where incremental Pre-Roll execution can stabilize rank while higher-priced formats face sustained demand elasticity.

Competitive Landscape

Terra Labs sits at rank #51 in July 2026, falling 18 positions year over year from #33, and sliding 10 spots versus April 2026’s #41; the contrast to its October 2025 peak at #6 adds a 45-place drop from peak to current. While General Admission holds #1 with a -22.3% year-over-year sales change and Back Forty / Back 40 Cannabis advanced to #2 with a 17-place YoY climb and 215.2% YoY sales growth, Terra Labs’ downward move from #41 to #51 over the past three months indicates lost share to faster-rising leaders; the trajectory implies Terra Labs must reverse multi-quarter rank erosion to avoid slipping further out of the top 50.

Notable Products

Frosted Oranges Infused Pre-Roll (0.5g) posted the steepest movement in July 2026 with a -51.5% month-over-month drop to rank 7, while Blueberry Avalanche Infused Pre-Roll 3-Pack (1.5g) surged +75.1% to rank 4. Sonic Boom Pre-Roll 2-Pack (2g) also climbed +60.7% to rank 2, whereas Strawberry Tsunami Diamond Infused Pre-Roll 5-Pack (2.5g) held rank 1 on +38.2% growth and roughly $46.3K in sales. Eight of the top ten are Pre-Roll multipacks, indicating consumer preference is concentrating around variety and value formats rather than single-stick options. This mix implies Terra Labs is consolidating share through higher-count, infused Pre-Roll formats that can swing quickly with promotions, signaling a strategy that trades depth in a few scalable SKUs for volatility in month-to-month performance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.