Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

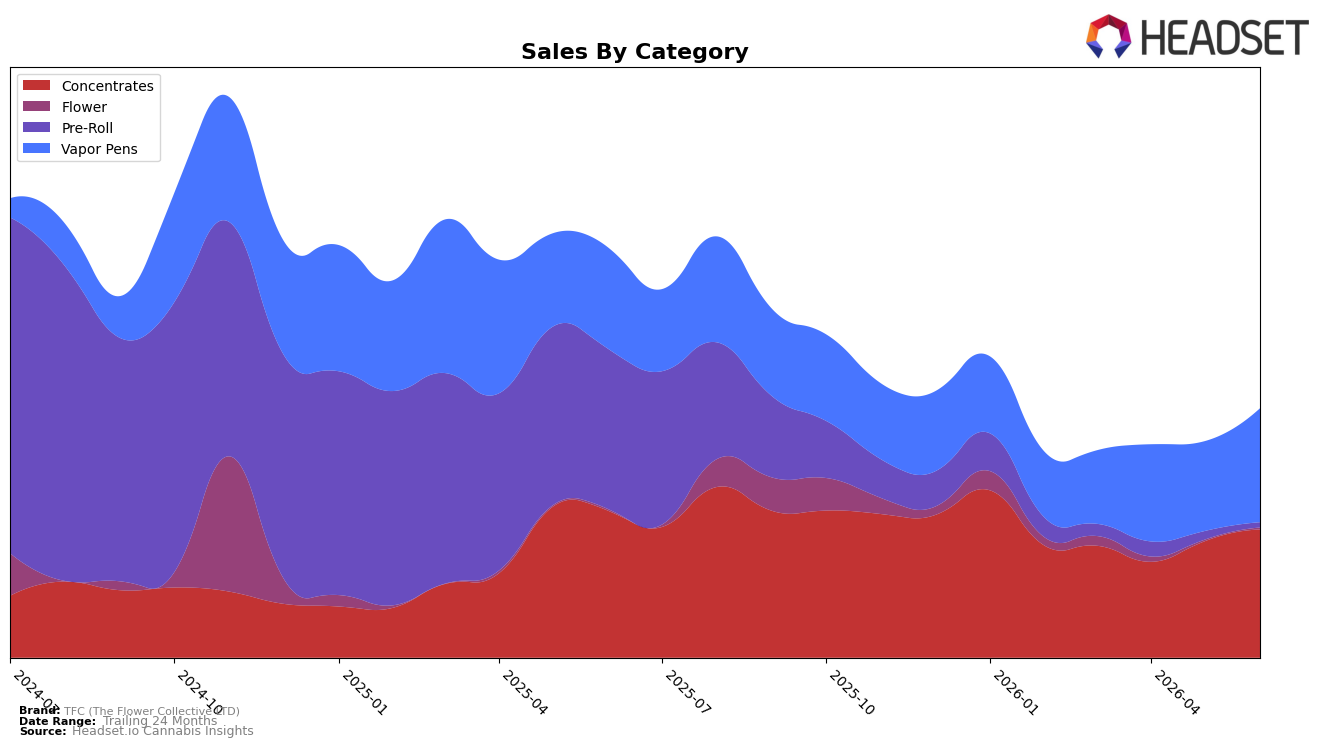

TFC (The Flower Collective LTD) concentrated nearly half of June 2026 sales in Concentrates at 49.64% share, while Vapor Pens carried 44.27%, indicating a two-pillar mix that displaced Pre-Roll to a marginal 3.67% share. Month over month, Vapor Pens expanded 25.53% versus 9.75% for Concentrates, while Pre-Roll contracted 25.52%; year over year, Concentrates declined 12.32% as Vapor Pens grew 11.93%. With Pre-Roll down 94.04% year over year and Flower up 5.41% year over year but still just 2.42% share, the mix is coalescing around higher-ticket inhalables, implying a strategic tilt toward categories where price can carry volume despite brand-level sales down 37.51% year over year.

The average price rose 30.66% year over year to $35.53, alongside a Vapor Pens average of $50.53 and Concentrates at $29.58, while the brand held rank 18 in Concentrates in Colorado. Month-over-month growth concentrated in Vapor Pens at 25.53% versus 6.18% in Flower, suggesting price-led, premium-leaning demand is offsetting softness in value-driven Pre-Roll; the pattern implies TFC (The Flower Collective LTD) is positioning for depth in Concentrates and margin capture in Vapor Pens, using category mix to stabilize against a 43.33% two-year sales decline while defending a mid-pack Concentrates placement at rank 18.

Competitive Landscape

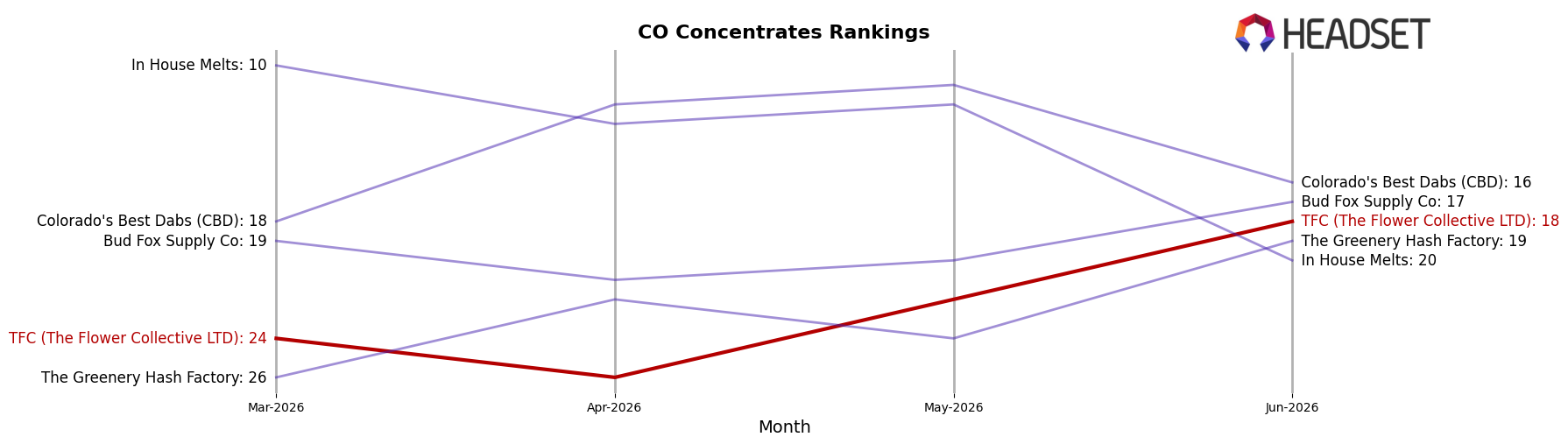

TFC (The Flower Collective LTD) ranks #18 in CO Concentrates in June 2026, improving 4 positions year over year from #22 while edging up 6 spots versus March 2026’s #24; this sits just one step below its peak of #17 reached in August 2025 and indicates incremental share recovery rather than a breakout. Competitive pressure is concentrated at the top: Amber held #1 year over year with a 39.0% sales lift, while 710 Labs stayed at #2 despite a -9.9% sales decline, a dynamic that suggests stable podium positions even as growth patterns diverge; against that backdrop, TFC’s +4 rank gain year over year and +6 since March 2026 point to a gradual climb driven more by consistent execution than category churn.

Notable Products

Pie Dance Bubble Hash (1g) set the tone in June 2026 with a 202.9% month-over-month surge and a move to rank 1, indicating demand is coalescing around solventless concentrates rather than spreading across form factors. Indica Bubble Infused Blunt (1g) climbed 56.1% MoM to rank 6 while Hitchcock's Cut Bubble Hash (1g) rose 21.1% MoM to rank 4, and together these gains point to a skew toward value-forward inhalables that convert momentum without discounting beyond a single mid-tier $10k-plus item. With seven of the top ten SKUs in Concentrates and only two Vapor Pens in ranks 5 and 8, the assortment concentration suggests TFC (The Flower Collective LTD) is leaning into bubble hash-led share capture rather than balancing into cartridges. The pattern implies a near-term commercial direction focused on solventless depth and pre-roll adjacency to lock in repeat buyers while deprioritizing broader vapor expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.