Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

(the) Essence is stocked at 725 licensed dispensaries across Illinois, New Jersey, and 10 other states, 158 of them in Illinois, with the deepest coverage in Chicago, Normal, Peoria, Addison, and Arlington Heights. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

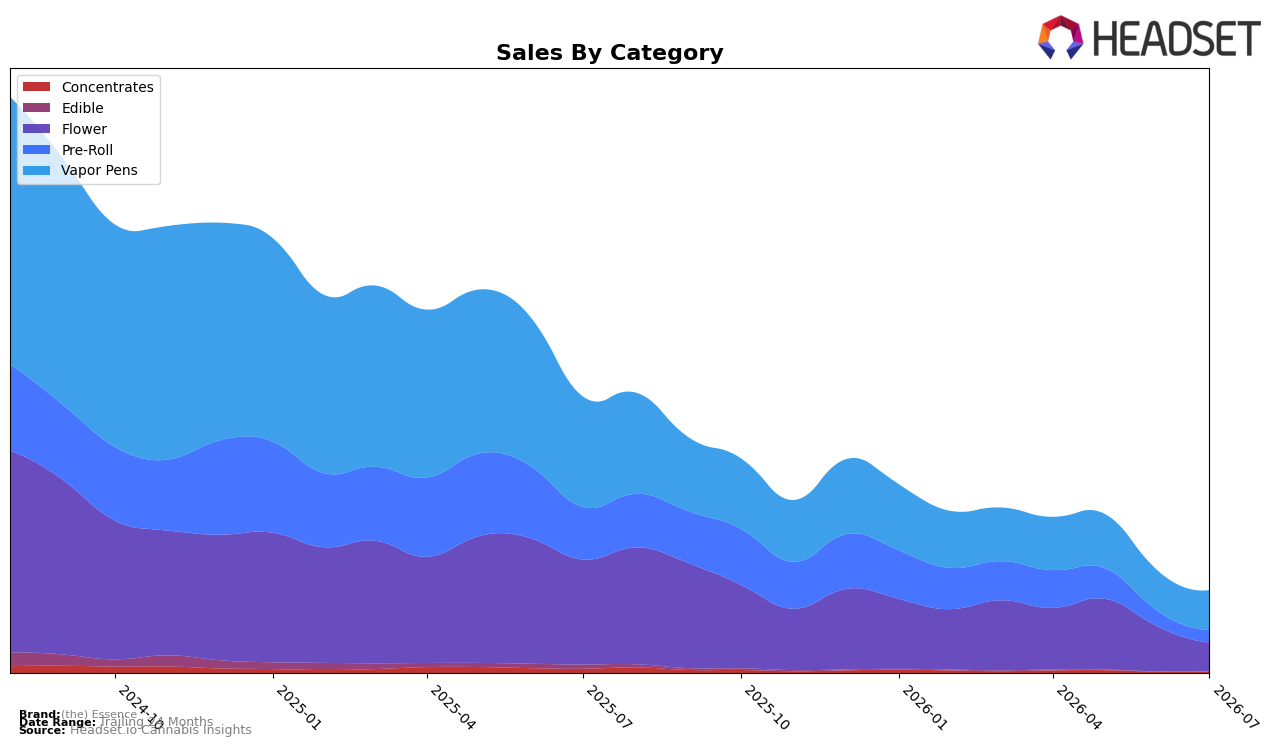

Vapor Pens held 48.24% share in July 2026 with a year-over-year decline of 63.86% and a month-over-month dip of 0.80%, while Flower at 34.60% share fell 72.74% YoY and 35.99% MoM; Pre-Roll at 15.13% share dropped 76.14% YoY and 18.78% MoM. Concentrates were the only MoM gainer at 8.51% despite a 64.82% YoY drop, whereas Edible, now just 0.17% share, contracted 96.63% YoY and 36.94% MoM. With brand-wide sales down 70.07% YoY and the average price down 2.54% YoY to $27.96, the category mix has consolidated toward Vapor Pens and away from Flower and Pre-Roll, implying a defensive pivot to fewer, larger-volume formats even as Illinois Vapor Pens rank sits at 14.

Rank 14 in Vapor Pens in Illinois alongside a 0.80% MoM slide and a 63.86% YoY drop indicates that (the) Essence is maintaining presence but yielding velocity to the middle tier, while the 35.99% MoM contraction in Flower signals active deprioritization or shelf loss where price at $40.44 suggests limited promotional push. The 8.51% MoM lift in Concentrates, despite just 1.86% share, points to a testable niche that can buffer volatility as Pre-Roll’s 18.78% MoM decline and Edible’s 36.94% MoM fall compress breadth; the implication is a need to anchor positioning around a single lead format (Vapor Pens) while selectively scaling Concentrates to diversify without diluting focus.

Competitive Landscape

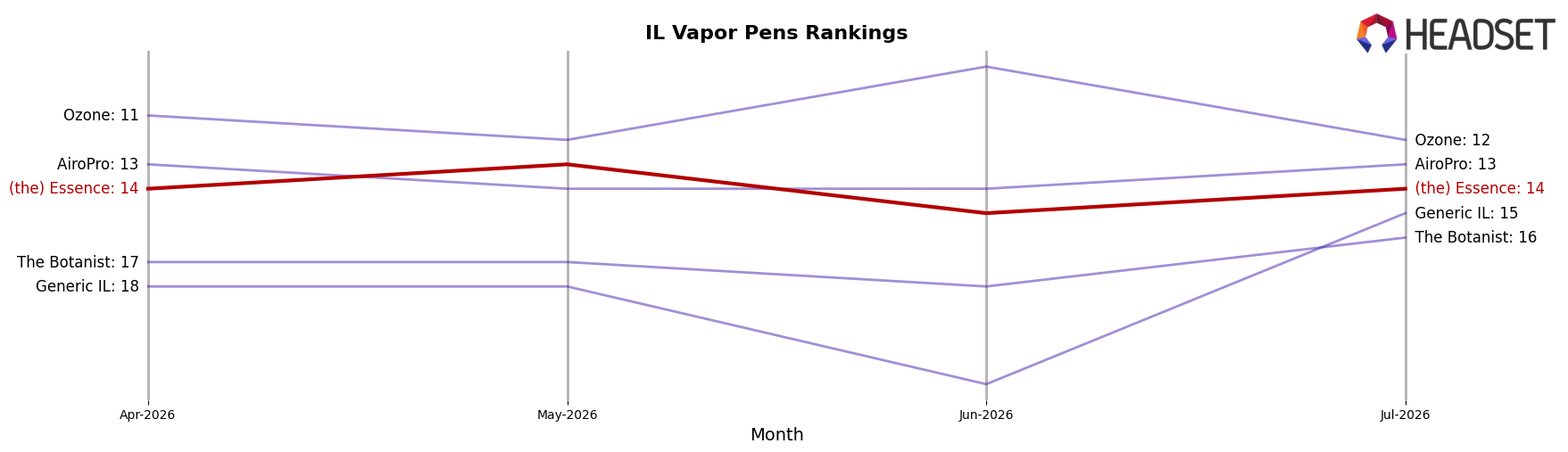

(the) Essence sits at rank #14 in Illinois Vapor Pens in July 2026, down 9 positions year over year from #5, and unchanged versus April 2026 at #14; meanwhile, &Shine holds #1 with an 11.09% YoY sales increase and Select is #2 with 15.30% YoY growth, while Joos advanced to #4 from #6 as RYTHM moved to #5 from #4. Given the prior peak at #4 in February 2025 and the flat three-month rank at #14, the pattern implies (the) Essence has shifted from a contender near the top tier to a mid-pack position that will require share capture against upward-moving rivals to regain earlier rank territory.

Notable Products

Hyphen - Strawberry Cough Distillate Cartridge (1g) posted the most notable movement in July 2026 with +185.7% MoM, vaulting to rank 2 while Hyphen - Bombsicle Distillate Cartridge (1g) slid 7.6% MoM to rank 3. Three of the top four are Vapor Pens, indicating category concentration, while Pre-Rolls span ranks 1, 5, 6, and 8 with steep declines of -25.2% and -20.2% on J's - Dead Headz Pre-Roll (1g) and J's - Biscotti Pre-Roll (1g). Cantaloupe Haze Distillate Cartridge (1g) advanced 35.0% MoM at rank 4 as Casey Jones (3.5g) held rank 10, with only one Flower SKU in the top ten and a single Vapor Pen surpassing $80,000. The mix implies a strategic skew toward Vapor Pens, with momentum consolidating in a few fast-rising SKUs while legacy Pre-Rolls require repositioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.