Where to Buy

The Green Lady Dispensary is stocked at 76 licensed dispensaries across New York and Massachusetts, 74 of them in New York, with the deepest coverage in New York, Queens, Rochester, Buffalo, and Concord. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

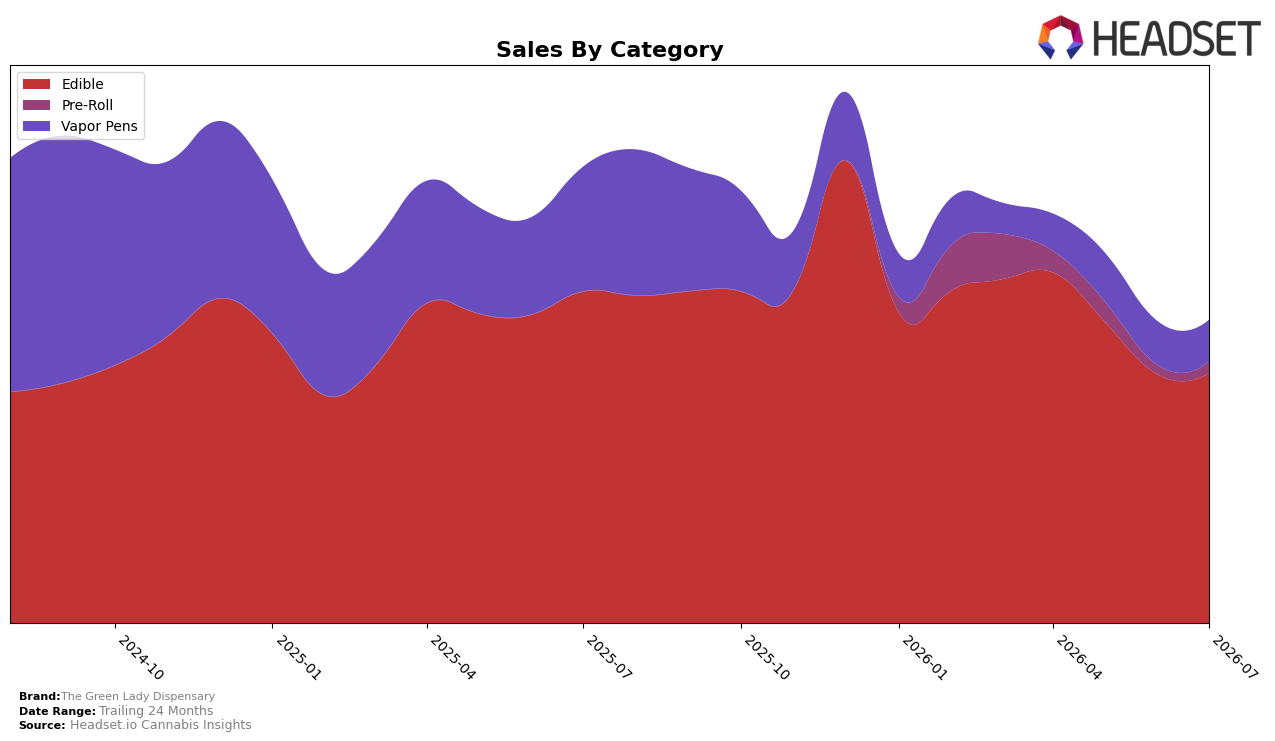

Market Insights Snapshot

In July 2026, The Green Lady Dispensary concentrated 82.59% of sales in Edible, where sales were down 24.60% year over year but up 0.54% month over month, while Vapor Pens held 13.71% share with a 66.63% year-over-year decline and a 4.77% month-over-month dip. Pre-Roll was 3.70% of sales with no year-over-year basis but a 24.07% month-over-month increase, and the average price fell 12.33% year over year to $28.30 as Edible’s average price sat at 26.93; together, these shifts point to Edible anchoring volume as Vapor Pens contract and Pre-Roll emerges as the incremental growth pocket.

The category mix implies a defensive tilt toward Edible scale in New York, where an Edible rank of 30 signals mid-tier presence, with the 0.54% month-over-month Edible uptick counterbalancing a 66.63% Vapor Pens slide and leveraging a 12.33% brand-wide price reduction. With Pre-Roll expanding 24.07% month over month off a 3.70% share base and Vapor Pens receding 4.77% month over month, the path to lift rank from 30 likely relies on deepening Edible assortment while seeding Pre-Roll to diversify away from the 33.61% year-over-year brand sales decline.

Competitive Landscape

The Green Lady Dispensary sits at rank #30 in July 2026, down 2 positions year over year from #28 and 4 positions worse than its three-month mark at #26, while also 6 positions off its peak at #24 in January 2025; in contrast, Off Hours slipped from #1 to #2 with a -10.4% year-over-year sales change and Wyld held #3 with a 7.4% year-over-year increase, implying that The Green Lady Dispensary’s downward rank drift amid mixed competitor momentum points to share being ceded to stable and rising incumbents rather than a category-wide contraction.

Notable Products

Mango Mojito Live Resin Gummies 10-Pack (100mg) posted the steepest decline in July 2026 at -17.2% and slid to rank 7, while Lemon Meringue Live Resin Disposable (1g) fell -13.2% at rank 8, implying mid-pack volatility concentrated in Live Resin formats. In contrast, Rainbow Z Live Resin Cartridge (1g) climbed +27.8% to rank 6 as Flirtatious - THC/THCV 2:1 Sex on the Beach Gummies 10-Pack (100mg THC, 50mg THCV) jumped +33.0% at rank 5, signaling a shift toward novelty actives and Live Resin devices over legacy 1:1 offerings. Four of the top ten are Edible SKUs anchored by ratioed cannabinoids, yet the category’s leaders—rank 1 at -1.9% and rank 2 at -1.6%—flattened while a THCV duo advanced into ranks 4–5, suggesting consumer rotation within Edibles from functional 1:1s to performance-tinged formulations. With Vapor Pens occupying ranks 6, 8, and 9 but splitting between +27.8% and -41.0%, the mix points to portfolio polarization where innovation spikes offset erosion in older Live Resin lines, guiding The Green Lady Dispensary toward faster product refresh cycles and targeted support for high-velocity novelty formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.