Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

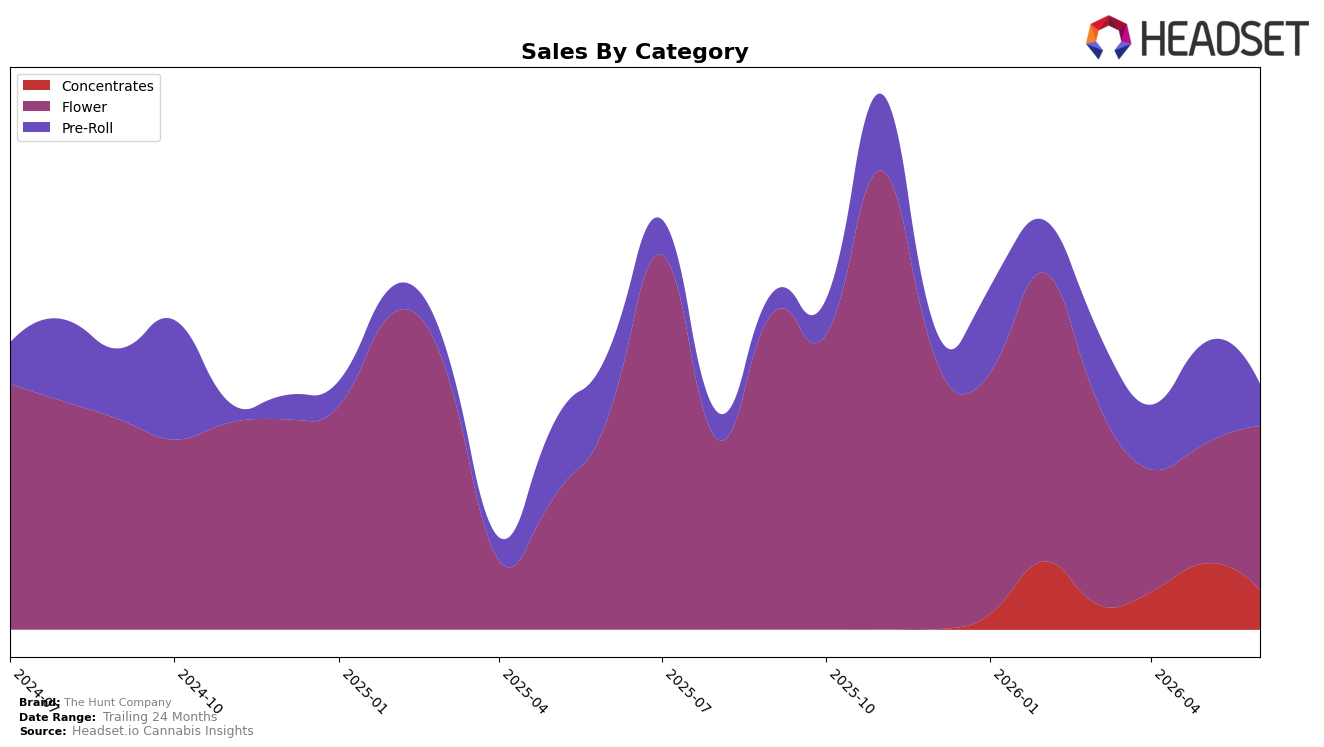

In June 2026, The Hunt Company’s mix concentrated in Flower at 66.86% share, with Flower down 22.92% year over year but up 37.52% month over month, while Pre-Roll held 17.13% share with a 35.02% YoY decline and a 58.48% MoM drop, and Concentrates at 16.01% share fell 40.52% MoM with no YoY comp available. Despite an average price decline of 17.49% YoY to $15.60 and total brand sales down 11.58% YoY, the Flower MoM rebound alongside sharp MoM pullbacks in Pre-Roll and Concentrates indicates a tactical pivot back toward the core Flower business, with rank at 57 in Flower in Illinois anchoring where momentum must convert to share.

The mix shift—Flower’s 37.52% MoM lift against Pre-Roll’s 58.48% MoM contraction and Concentrates’ 40.52% MoM decline—implies the brand is trading variety breadth for depth in its leading category, a positioning that favors price-sensitive customers after a 17.49% YoY price decrease. With total sales still 34.20% below the 24‑month level and Flower carrying 66.86% of revenue while sitting at rank 57 in Illinois Flower, the path to regain share likely depends on sustaining the Flower MoM recovery while stabilizing the secondary categories to prevent over-reliance on a single segment.

Competitive Landscape

The Hunt Company sits at rank #57 in Illinois Flower for June 2026, a 4-spot decline from #53 year over year, even as it climbed 17 positions from #74 in March 2026; against a category led by High Supply / Supply holding #1 with 32.1% YoY sales growth and &Shine rising from #10 to #5 with 28.5% YoY growth, the brand’s drop from its peak #42 in July 2025 and current placement outside the top 50 indicate share is consolidating among top players despite a recent quarter-on-quarter rank recovery, implying that sustained gains will require outpacing mid-tier climbers as well as the #1 incumbent.

Notable Products

Greasy Gusher Pre-Roll (1g) posted the steepest movement in June 2026 with a -55.5% month-over-month drop while holding rank 2, implying a sharp pullback in pre-roll velocity even as it stayed near the top. In contrast, Blue Power (3.5g) jumped +52.3% month-over-month to rank 1, creating a widening gap between Flower and Pre-Roll performance at the very top. Four of the top ten are Flower SKUs, including Big Detroit Energy (3.5g) at rank 3 and Weedies (3.5g) at rank 4, signaling category concentration toward Flower as pre-roll softness extends beyond Triangle Cake Pre-Roll (1g) at rank 5 with a -3.3% month-over-month dip. The pattern implies The Hunt Company is tilting toward higher-velocity Flower leadership while reevaluating pre-roll assortment and price architecture to stabilize share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.