Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

UB GOOD is stocked at 143 licensed dispensaries across Ohio, Maryland, and Nevada, 130 of them in Ohio, with the deepest coverage in Columbus, Cincinnati, Akron, Cleveland, and Dayton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

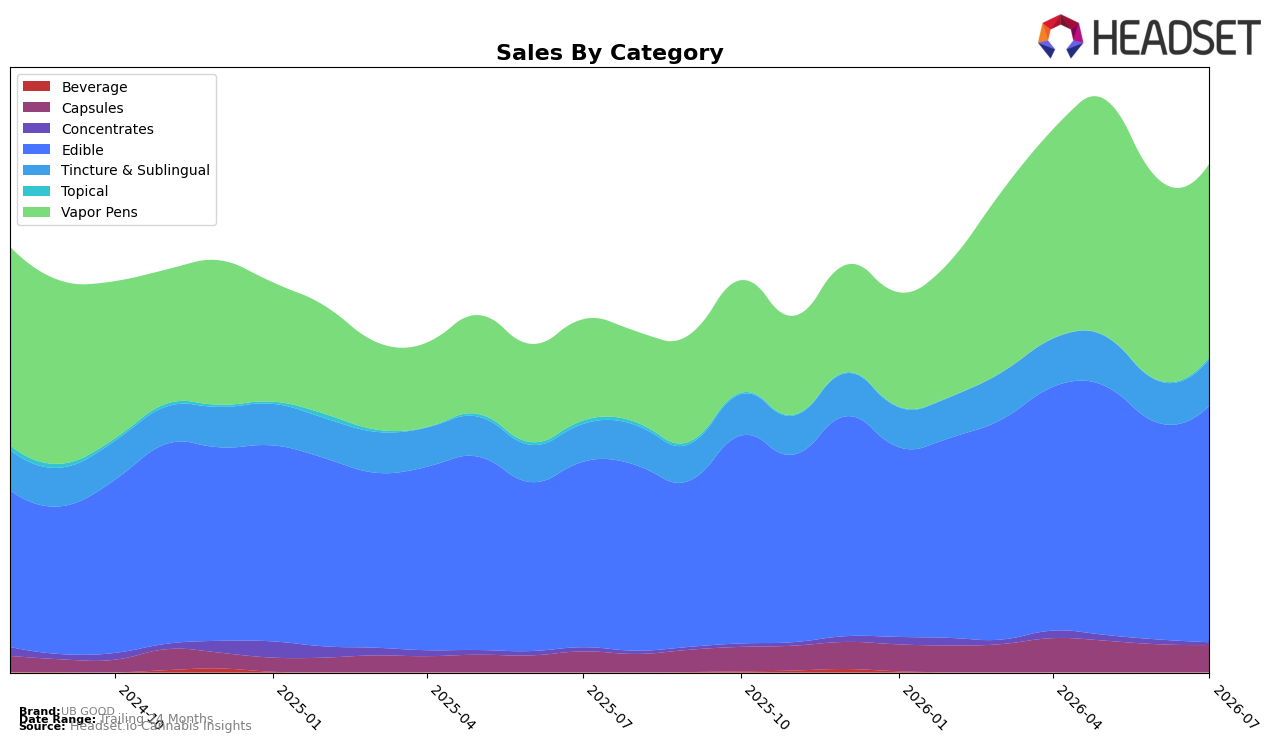

UB GOOD’s mix in July 2026 is anchored by Edible at 46.56% share with 27.54% year-over-year growth and 9.18% month-over-month lift, while Vapor Pens hold 38.06% share with 91.10% year-over-year growth but a 3.88% month-over-month decline. Tincture & Sublingual contributes 9.18% share with 24.00% year-over-year and 11.49% month-over-month increases, as Capsules at 5.35% share rose 31.44% year-over-year despite a 2.63% month-over-month dip. At the fringe, Topical is 0.36% share with a 233.98% month-over-month spike against a 42.49% year-over-year drop, and Concentrates fell 36.40% year-over-year and 44.99% month-over-month to 0.49% share. The pattern points to a portfolio consolidating around Edible and Vapor Pens for volume while selective momentum in Tincture & Sublingual offsets volatility in small niches, enabling total brand sales to scale 44.29% year over year with a 5.05% average price decrease to $26.31.

UB GOOD’s rank of 2 in Edible in Ohio combined with a 9.18% month-over-month gain in Edible and a 3.88% month-over-month decline in Vapor Pens suggests prioritizing Edible-led visibility while containing Vapor Pens’ pullback to protect the 38.06% mix. The 11.49% month-over-month rise in Tincture & Sublingual alongside a 31.44% year-over-year lift in Capsules indicates wellness-adjacent formats can absorb demand shifts if pricing stays disciplined after a 5.05% brand-wide price reduction, while the 233.98% month-over-month rebound in Topical and the 44.99% month-over-month drop in Concentrates argue for test-and-learn allocation rather than broad expansion. The implication is a two-engine posture where Edible growth and Vapor Pens scale are balanced by targeted bets in Tincture & Sublingual and Capsules to stabilize mix when pen momentum moderates and niche formats remain volatile.

Competitive Landscape

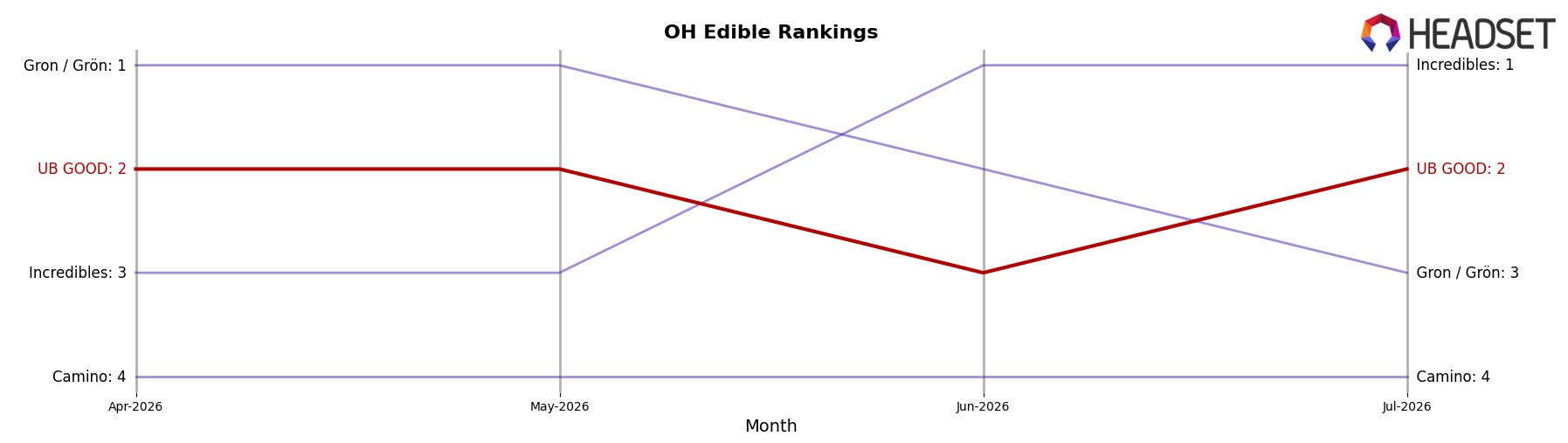

UB GOOD is currently ranked #2 in OH Edible in July 2026, matching its #2 position from July 2025, and holding steady from April 2026 at #2 while remaining below its peak at #1 in May 2025; meanwhile, Incredibles holds #1 now and was also #1 a year ago, and Gron / Grön sits at #3 after rising from #5 year over year, indicating upward pressure just behind UB GOOD. With Camino sliding from #3 to #4 and Smokiez Edibles improving from #6 to #5, the mid-pack is in flux while UB GOOD’s unchanged #2 position for both year over year and the last three months signals durable placement but limited momentum to reclaim #1 without a share-accretive shift.

Notable Products

Blue Rush BDT Distillate Cartridge (1g) posted the steepest decline in July 2026 at -0.17% MoM while slipping to rank 5, whereas Red Splash Distillate Cartridge (1g) climbed 23.85% MoM to rank 7; this inverse movement suggests UB GOOD’s Vapor Pens lineup is fragmenting around price-point or flavor preferences. Cherry Pomegranate Extra Strength Releaf Gummies 10-Pack (500mg) rose 22.16% MoM to hold rank 1 and Pineapple Punch Extra Strength Gummies 10-Pack (500mg) gained 13.08% MoM at rank 2, and four of the top ten are Edible SKUs, pointing to sustained dominance of the gummy format over hardware-attached categories. Spark - Green Punch Distillate Cartridge (1g) added 12.21% MoM at rank 8 while Sativa Kiwi Dragonfruit Boost Gummies 10-Pack (100mg) advanced 10.51% MoM at rank 6, and the CBD/THC 10:1 Juicy Pear Gummies 20-Pack (1100mg CBD, 110mg THC) dipped -3.45% at rank 9, implying balanced trade-up into higher-potency edibles rather than broader category attrition. Taken together, the concentration of ranks 1–3 in gummies and mixed momentum in Vapor Pens indicate UB GOOD’s commercial direction is tilting toward potency-led edible leadership with selective pen SKU pruning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.