Market Insights Snapshot

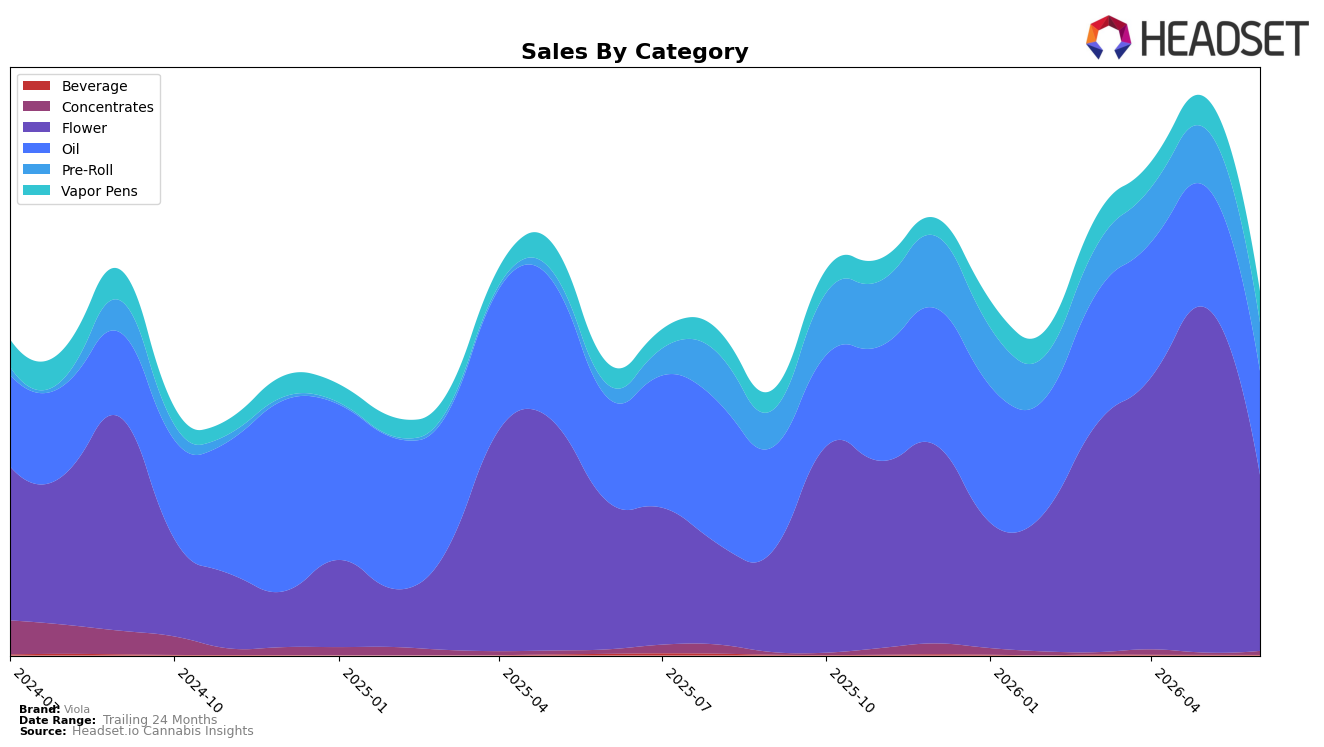

In June 2026, Viola’s mix tilted toward Flower at 48.52% share, yet the category dropped 49.06% month over month even as it grew 19.64% year over year, indicating a swing from a high April–May base into a leaner June; Oil held 28.60% share with a 14.56% MoM decline and a flat 0.09% YoY change. Pre-Roll expanded to 13.25% share on a 270.68% YoY surge while contracting 16.37% MoM, and Vapor Pens reached 8.51% share with a 0.61% MoM uptick and 47.05% YoY growth. Concentrates remained just 1.03% share but spiked 90.49% MoM against a 10.96% YoY decline, while Beverage slid to 0.08% share with a 27.06% MoM and 79.07% YoY drop. The pattern implies Viola is leaning on year-over-year gains in core inhalables while navigating sharp intra-quarter volatility, with category concentration in Flower amplifying month-to-month swings.

The shift suggests a positioning anchored in value-led inhalables: average price fell 1.00% YoY to one price point across the portfolio while Flower’s average ticket held near the low end, and Pre-Roll’s triple-digit YoY growth alongside Vapor Pens’ 47.05% YoY lift points to traction in accessible formats even as MoM pullbacks hit three of the top four categories. With rank 42 in Flower in Colorado and Flower still near half of mix, the 49.06% MoM decline concentrates rank risk, whereas the 0.61% MoM increase in Vapor Pens and the 90.49% MoM rebound in Concentrates indicate adjacent inhalable lanes that can buffer volatility; the implication is a need to rebalance share from a 48.52% Flower dependency toward categories showing steadier month progression to stabilize June-season rank and sustain the 24.92% brand-level YoY growth.

Competitive Landscape

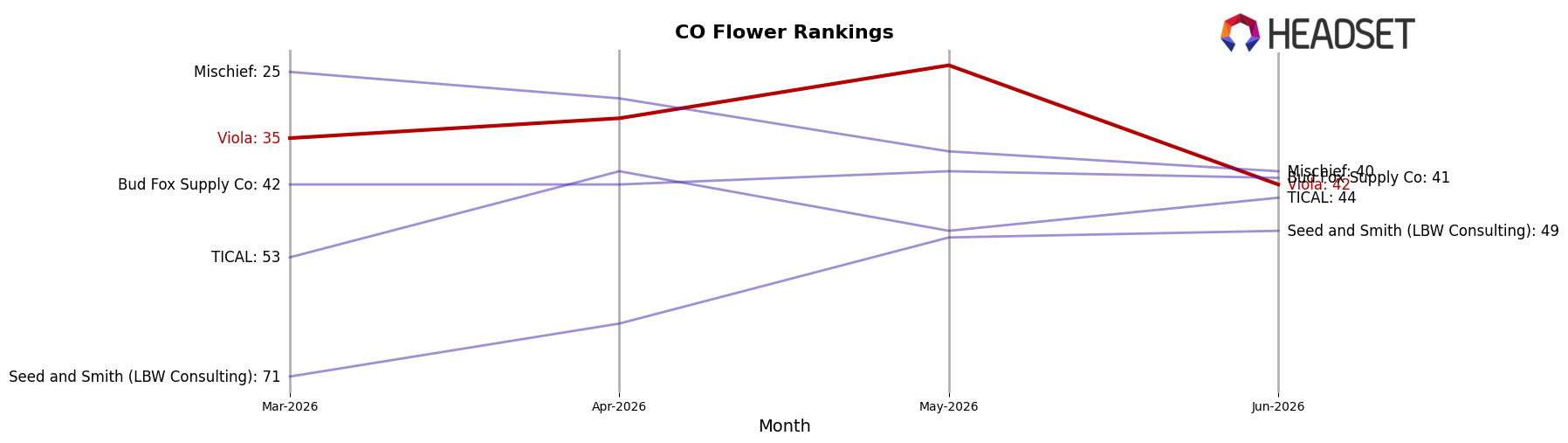

Viola sits at rank #42 in Colorado Flower in June 2026, improving 5 positions from #47 year over year, but sliding 7 spots from #35 in March 2026 after peaking at #24 in May 2026; meanwhile, Seed & Strain Cannabis Co. edged up from #2 to #1 while posting a 62.8% YoY sales increase, and Good Chemistry Nurseries moved down from #1 to #3 with a -2.8% YoY change, indicating Viola’s mid-year pullback is driven more by intensified top-tier churn than broad market contraction and implies the rank trajectory depends on converting its May 2026 peak into sustained share rather than episodic spikes.

Notable Products

Junior Mintz Smalls (Bulk) posted the steepest move in June 2026, dropping 73.5% MoM and sliding to rank 10, while The Drop THC Extract Oil (20ml) fell 14.6% MoM at rank 3. Durban Gruntz Smalls (Bulk) also contracted 8.6% MoM yet held rank 1, and Skywalker OG Live Resin Cartridge (1g) in Vapor Pens inched up 2.3% MoM to rank 6. With seven of the top ten positioned in Flower and four of those as Smalls variants concentrated in bulk formats, the mix signals reliance on value Flower while volatility at the low end and declines in Oil imply a pivot is needed toward steadier, higher-retention formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.