Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

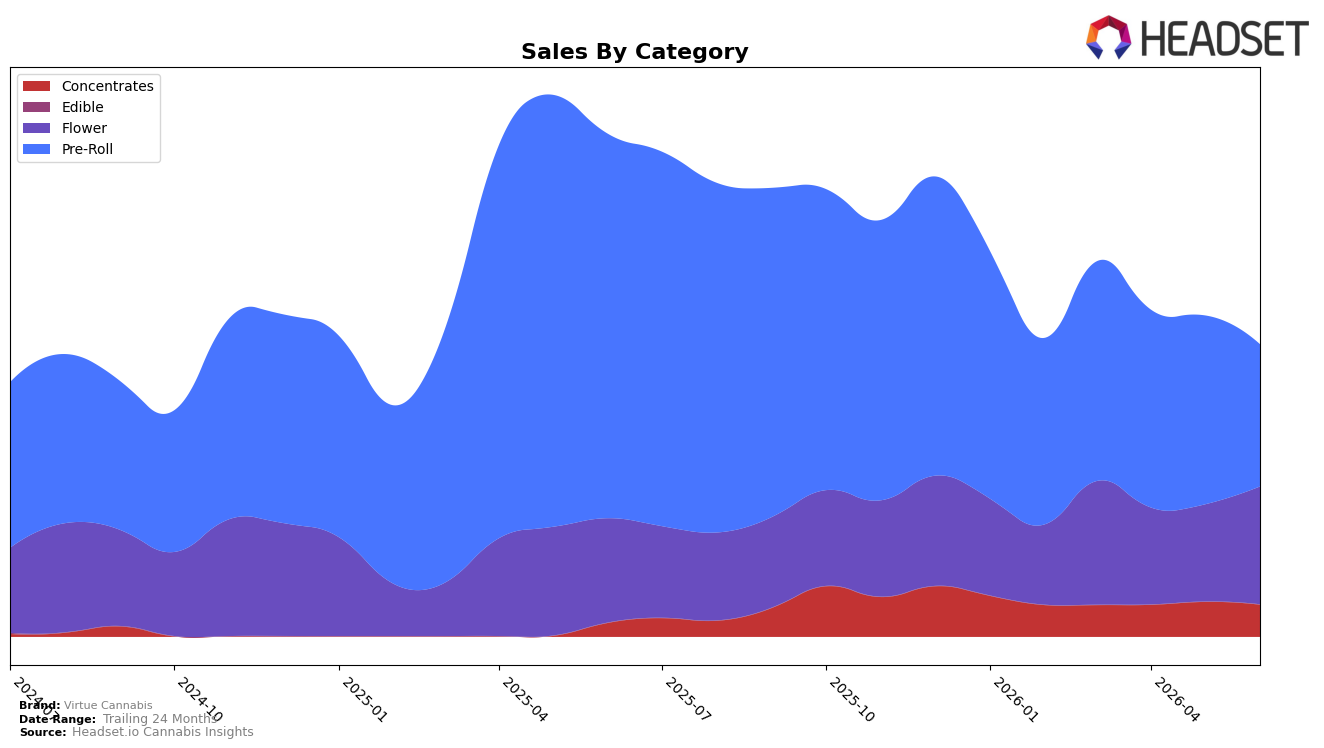

Virtue Cannabis concentrated 48.74% of June 2026 sales in Pre-Roll, where year-over-year sales fell 63.04% and month-over-month declined 24.80%, while Flower expanded to 40.33% share with sales up 13.08% YoY and 21.47% MoM. Concentrates held 10.92% share after a 133.37% YoY surge but slipped 8.05% MoM, and the brand’s average price rose 12.78% YoY to $38.16. With Pre-Roll ranked 34th in Alberta and shrinking on both YoY and MoM bases, the mix shift toward Flower’s double-digit MoM gain and Concentrates’ triple-digit YoY growth implies the portfolio is rebalancing away from a declining anchor toward categories with near-term velocity and margin potential.

The pivot suggests a positioning move from volume-led Pre-Roll toward higher-ticket Flower, where the 21.47% MoM growth alongside a 12.78% YoY average price increase points to trading up rather than discount-driven recovery, while the 8.05% MoM dip in Concentrates after 133.37% YoY growth indicates volatility that can be used as a tactical halo rather than a core driver. Given the 63.04% YoY contraction in Pre-Roll against a 13.08% YoY rise in Flower, maintaining relevance in Pre-Roll at a 34th-place rank in Alberta likely requires selective SKU pruning as the brand consolidates around formats where pricing power and sequential momentum are converging.

Competitive Landscape

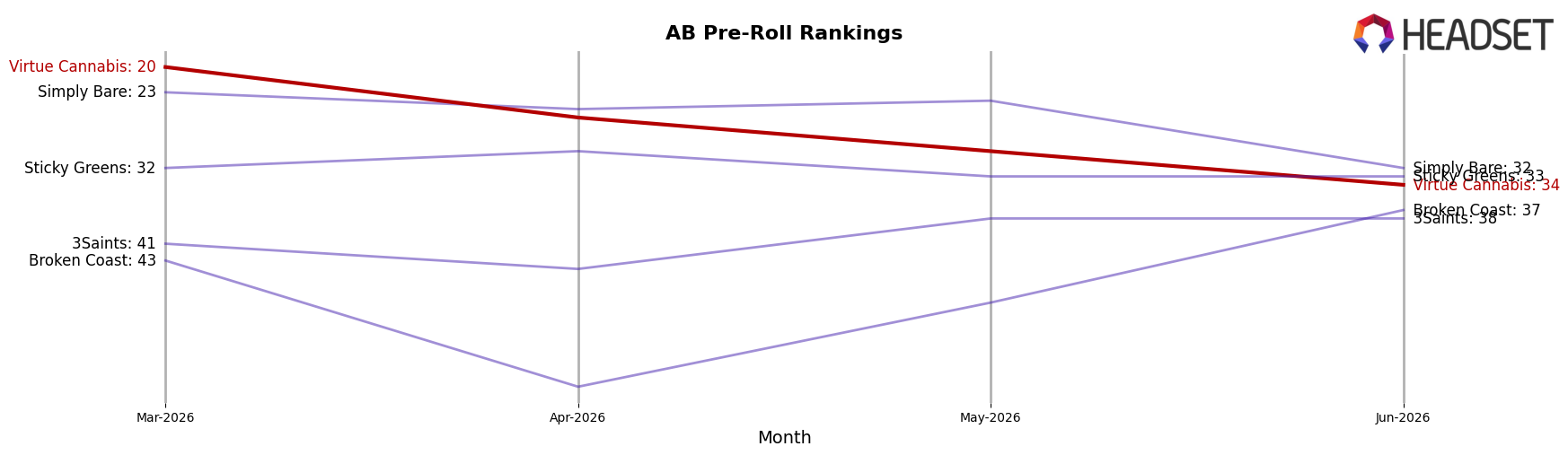

Virtue Cannabis sits at rank 34 in AB Pre-Roll for June 2026 after a year-over-year drop of 21 positions from rank 13, with a 14-rank slide since March 2026 when it was rank 20; this contrasts with Back Forty / Back 40 Cannabis rising 4 places from rank 6 to rank 2 alongside a 64.0% YoY sales increase, while General Admission holds rank 1 despite a 21.97% YoY sales decline. The peak at rank 13 in November 2025 followed by a 21-position fall implies Virtue Cannabis has shifted from mid-pack contender to lower-tier presence, signaling that regaining share will require reversing multi-month rank erosion rather than chasing short-term volatility.

Notable Products

Galactic Glue Blunt (1g) posted the steepest decline in June 2026 at -37% and slid to rank 4, while Fruitloops Diamond Infused Pre-Roll 5-Pack (2.5g) fell -21% yet held rank 1; this contrast signals reliance on multi-pack, value-leaning formats over single sticks. Orange Crush Pre-Roll 3-Pack (1.5g) climbed +31% to rank 5 as Galactic Glue Blunt (1g) contracted, and three of the top five SKUs are Pre-Roll formats, indicating pack-size concentration within the category. Flower entries Champagne Supernova (14g) and Galactic Glue (28g) placed at ranks 8 and 9 without month-over-month history, suggesting portfolio breadth but less current momentum than Pre-Rolls. The mix implies Virtue Cannabis is tilting toward bundled Pre-Roll offerings that sustain rank even amid price-sensitive pullbacks, with Flower positioned as secondary volume ballast around $57,772 in June 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.