Where to Buy

Vlasic Labs is stocked at 185 licensed dispensaries across Michigan, Missouri, and 8 other states, 59 of them in Michigan, with the deepest coverage in Detroit, Coldwater, Lansing, New Buffalo, and Grand Rapids. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

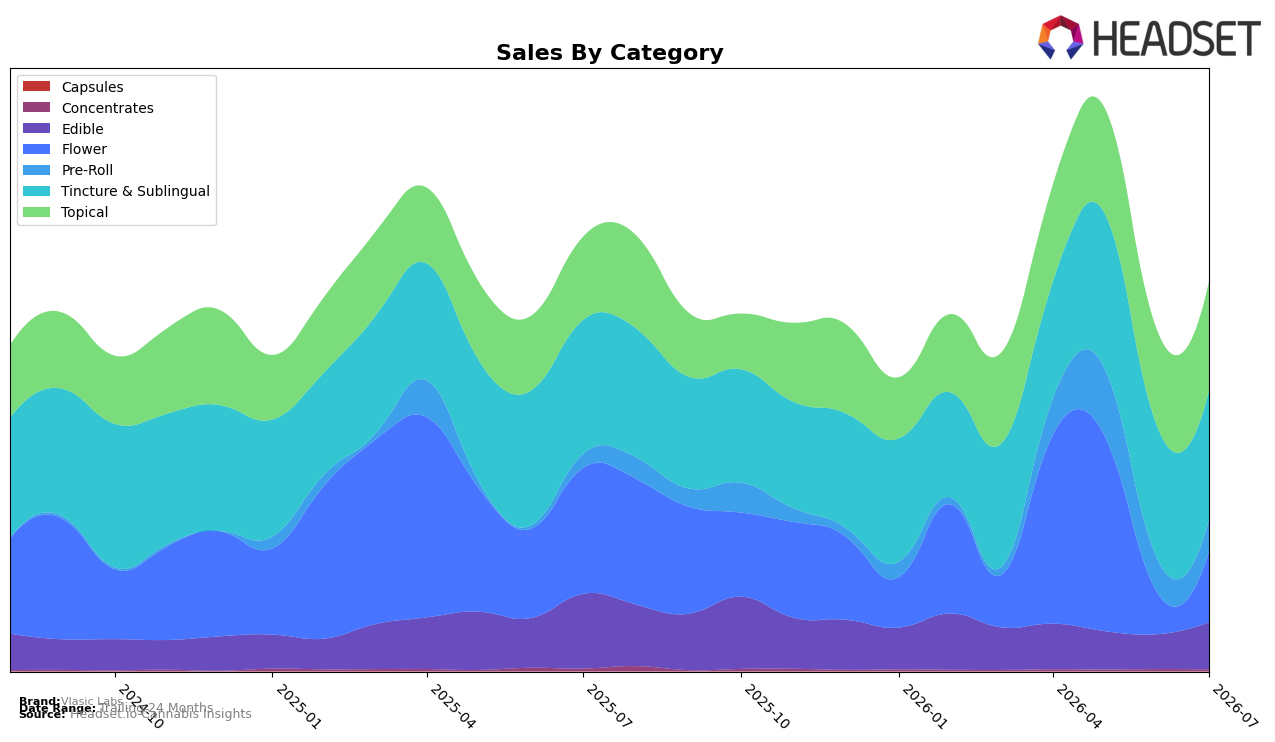

Vlasic Labs entered July 2026 with a category mix led by Tincture & Sublingual at 33.06% share, down 3.76% year over year and 2.28% month over month, while Topical rose to 28.09% share with a 31.54% YoY gain and 14.09% MoM lift. Flower held 18.20% share after a 72.90% MoM surge despite a 43.63% YoY decline, and Edible reached 12.05% share with 35.18% MoM growth against a 37.02% YoY drop. Pre-Roll captured 8.12% share with 129.52% YoY growth but slipped 5.26% MoM, and Concentrates remained marginal at 0.48% share with a 28.88% YoY and 13.29% MoM decline. The thesis is that July 2026 marks a pivot from historical reliance on Tincture & Sublingual toward faster-cycling form factors as Topical and Flower supply near-term volume momentum while legacy pillars contract.

The brand’s average price fell 23.08% YoY to $22.33, intersecting with a portfolio tilt where Topical’s 31.54% YoY growth and Flower’s 72.90% MoM spike can absorb price compression while maintaining mix breadth. With Vlasic Labs ranked 74 in Flower in Nevada, the 18.20% Flower share and 35.18% MoM Edible lift suggest a repositioning toward value-accessible inhalables and supportive wellness formats rather than premiumized concentrates, which contracted 13.29% MoM to 0.48% share. The implication is a two-track positioning: defend share via price-competitive inhalables where short-cycle demand is rebounding, and compound gains in Topical where repeat-driven growth (31.54% YoY) can offset erosion in Tincture & Sublingual (-3.76% YoY) and stabilize overall decline of 10.20% YoY in brand sales.

Competitive Landscape

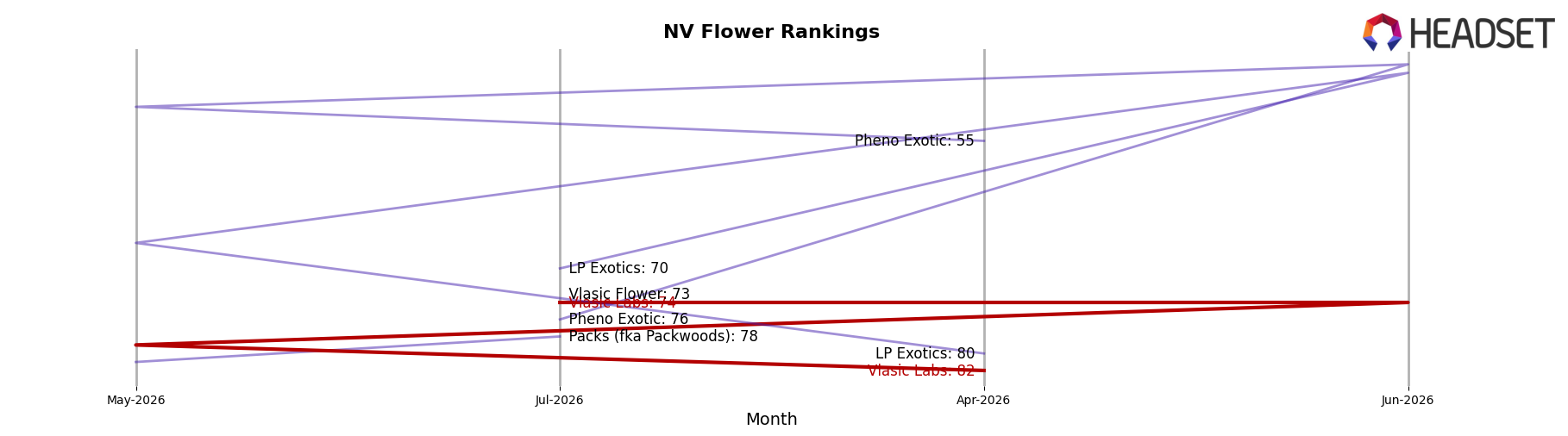

Vlasic Labs sits at rank #74 in NV Flower in July 2026, down 16 positions year over year from #58, while improving 8 ranks versus April 2026’s #82; that volatility contrasts with STIIIZY holding #1 after rising from #2 and RYTHM slipping from #1 to #2 alongside a −12.7% YoY sales change. Against rising challengers, Neon Moon advanced from #10 to #3 with +52.7% YoY sales and FloraVega / Welleaf surged from #24 to #5 with +299.7% YoY sales, while Vlasic Labs remains 36 spots below its April 2025 peak of #38. The pattern implies Vlasic Labs’ current #74 position and −16 YoY rank change signal share leakage to faster-climbing competitors despite a recent 8-rank quarter-over-quarter lift.

Notable Products

CBG Isolate Mood Tincture (1800mg CBG, 30ml, 1oz) posted the steepest decline at -9.5% MoM, slipping while holding rank 6, whereas CBD Full Spectrum Sports Roll On (3000mg CBD, 30ml, 1oz) climbed 39.4% MoM at rank 10 with $13,307 in July 2026 sales. CBD Full Spectrum Relief Cream (3000mg CBD, 3oz) in rank 4 rose 5.4% MoM, and Katsu Bubba Pre-Roll (1g) in rank 1 fell 5.6% MoM, indicating mix pressure at the very top even as selective recovery occurs lower in the top 10. With three Tincture & Sublingual SKUs and three Topical SKUs in the top ten, the concentration in wellness formats suggests Vlasic Labs is tilting demand toward higher-dosage relief products rather than inhalables.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.