Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

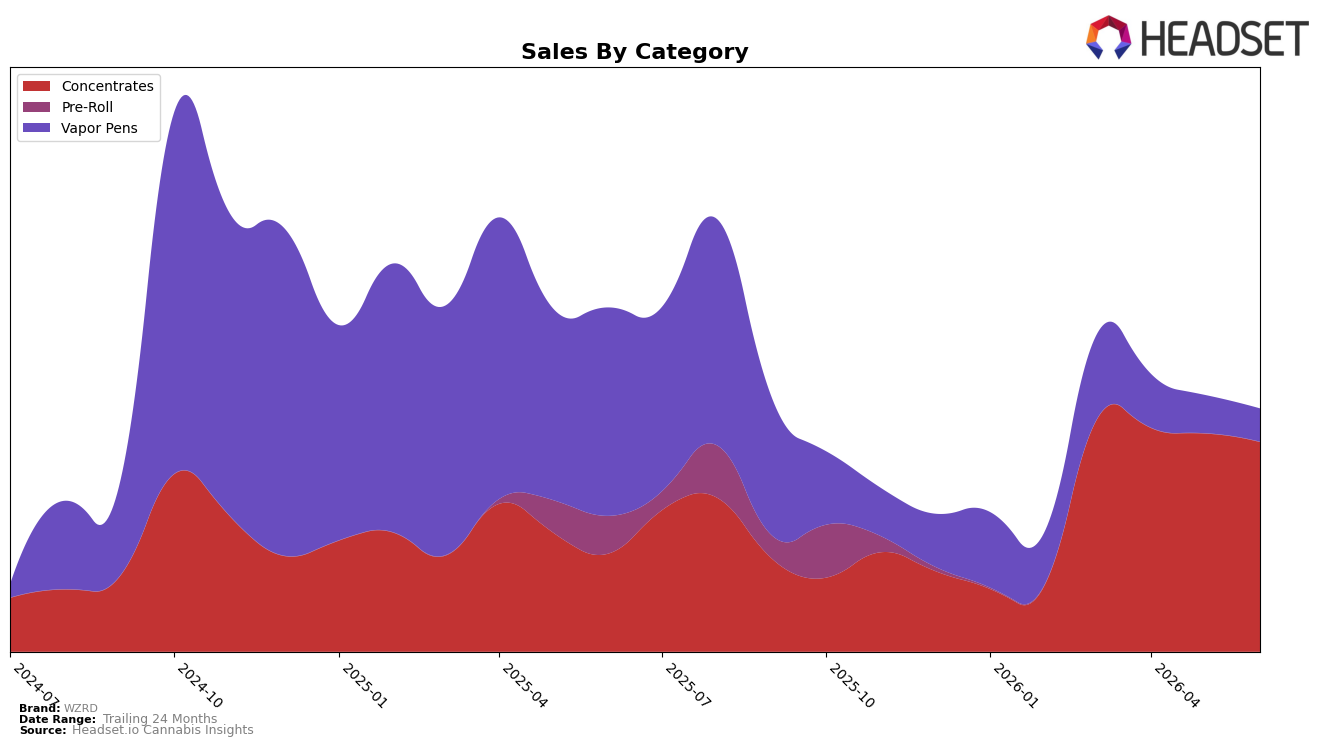

In June 2026, WZRD concentrated 86.38% of sales in Concentrates, up via a 114.07% year-over-year swing even as month-over-month volume in that category slipped 3.91%, while Vapor Pens fell to 13.62% share on an 84.14% year-over-year decline and a further 13.10% month-over-month drop. Against this mix shift, overall brand sales were down 29.40% year over year and average price contracted 35.18% to $11.38, implying a trade-down toward lower-priced Concentrates and away from higher-priced Vapor Pens despite Concentrates’ positive year-over-year growth.

The category tilt aligns with WZRD’s Concentrates standing at rank 12 in Arizona, suggesting mid-tier placement where a 114.07% year-over-year gain coupled with a 3.91% month-over-month dip points to momentum with short-term softness. With Vapor Pens shrinking 84.14% year over year and 13.10% month over month while Concentrates holds 86.38% share, the brand’s positioning is becoming more niche and price-led in Concentrates rather than balanced across formats, which implies future share stability will depend on defending rank 12 in Arizona Concentrates while de-emphasizing high-price pen exposure.

Competitive Landscape

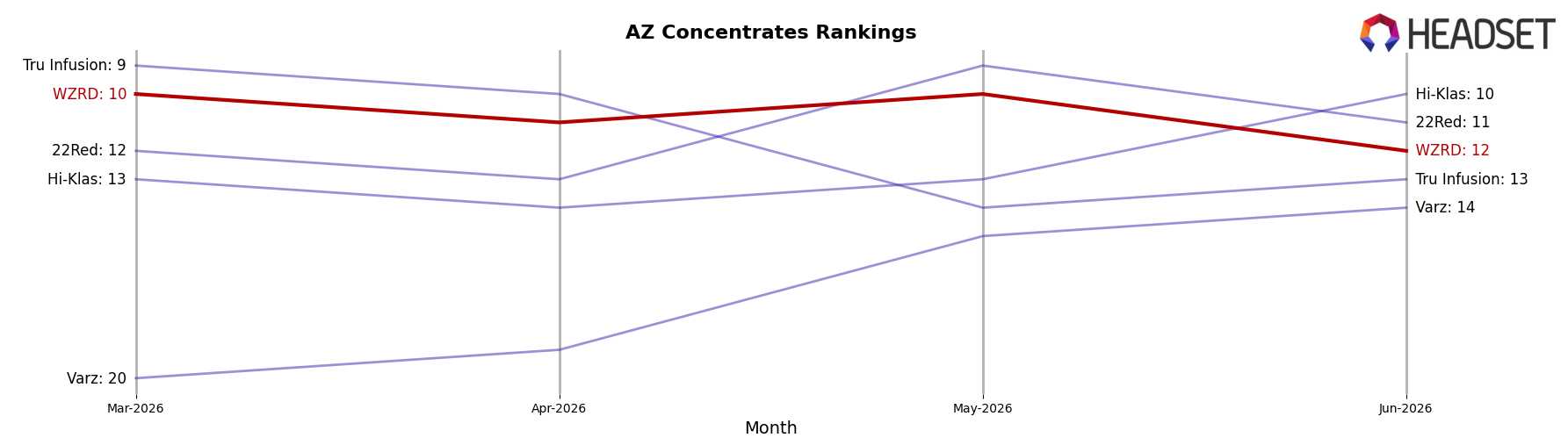

WZRD sits at rank #12 in Arizona Concentrates in June 2026, a 11-place improvement from #23 year over year, yet a 2-place slide from its peak at #10 in May 2026, implying momentum YoY but recent slippage within the quarter. Competitive movement is accelerating above WZRD: Grow Sciences advanced from #7 to #4 while expanding sales by 106.5%, and Drip Oils + Extracts rose from #5 to #3 with 32.5% YoY sales growth, whereas WTF Extracts fell from #3 to #5 alongside a 14.4% YoY sales decline; this mix indicates WZRD’s YoY rank climb coexists with faster ascents by select rivals, so holding share likely requires re-accelerating from the May 2026 peak rather than settling into a mid-pack position.

Notable Products

Pineapple Fruz Shatter (1g) posted the steepest setback in June 2026 with a -56.7% month-over-month drop and slid to rank 9, implying demand is consolidating away from lower-ranked shatter formats. Z Cubed Budder (1g) also retreated by -23.5% and held rank 4 while Puddles Cured Budder (1g) fell -14.7% at rank 7, indicating mid-pack concentrates are losing share to higher-velocity entries. At the top, Florida Jack Shatter (1g) grew 7.5% to sit at rank 2 while Tropical Cherry Shatter (1g) advanced 25.1% at a tied rank 2, and nine of the top ten are Concentrates SKUs, signaling category concentration despite mixed movements within subtypes. The mix implies WZRD is leaning into a concentrates-led lineup where a few shatter SKUs gain rank even as select legacy variants compress, pointing to a portfolio shift toward fewer, faster-moving leaders over broader depth, with Orange Zqueeze Badder (1g) anchoring the tier at rank 1 on $10,769 in sales.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.