High Expectations: Navigating the Cannabis Culture Clash Between New York City and the Empire State

Introduction

There has always been a cultural, economic, and social rift between New York City and the rest of the "Empire State". As Headset tracks the development of New York's emerging cannabis market naturally we must ask how these differences are represented in cannabis. With NYC accounting for approximately 43% of the state's population, knowing how the two geographies differ in cannabis consumption patterns and preferences can provide valuable insights for businesses.

Methodology

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset's business intelligence software. Headset's data is very reliable, as it comes digitally directly from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. In this report, the analysis contains a sample of 10 New York City retailers and 26 retailers from around the state, capturing a large majority of the retail presence in the state at the time of publication. All sales figures are pre-tax and post-discount.

Sales

It's no secret that there is money to be made in NYC, but with such competition between legal and illicit cannabis options in the city, how might NYC cannabis retailers compare to those around the state? Since the start of 2024, the limited legal NYC retailers have attracted an average of nearly $35,000 in total sales per day. This is 54.7% higher than the roughly $22,500 that we have seen from retailers in the rest of the state.

Furthermore, there are some pronounced differences in category preference between consumers in these groups. In NYC it seems like shoppers tend to put their money towards a greater variety of products, most notably Edibles and Pre-Rolls. In NYC, Edibles' share of total sales is 44.8% higher than the rest of the state capturing over 20% of total sales. Additionally, Pre-Rolls in NYC make up 17% of total sales compared to only 14% in the rest of the state. This comes at the expense of Flower which is 38% of all sales in New York excluding NYC while in NYC that number is only 31%.

It looks like people in the city are enjoying the greater range of products that come with adult-use cannabis. However, it is the rest of the state that more closely resembles the US market. Will NYC converge on the national average over time or does NYC move to its own beat?

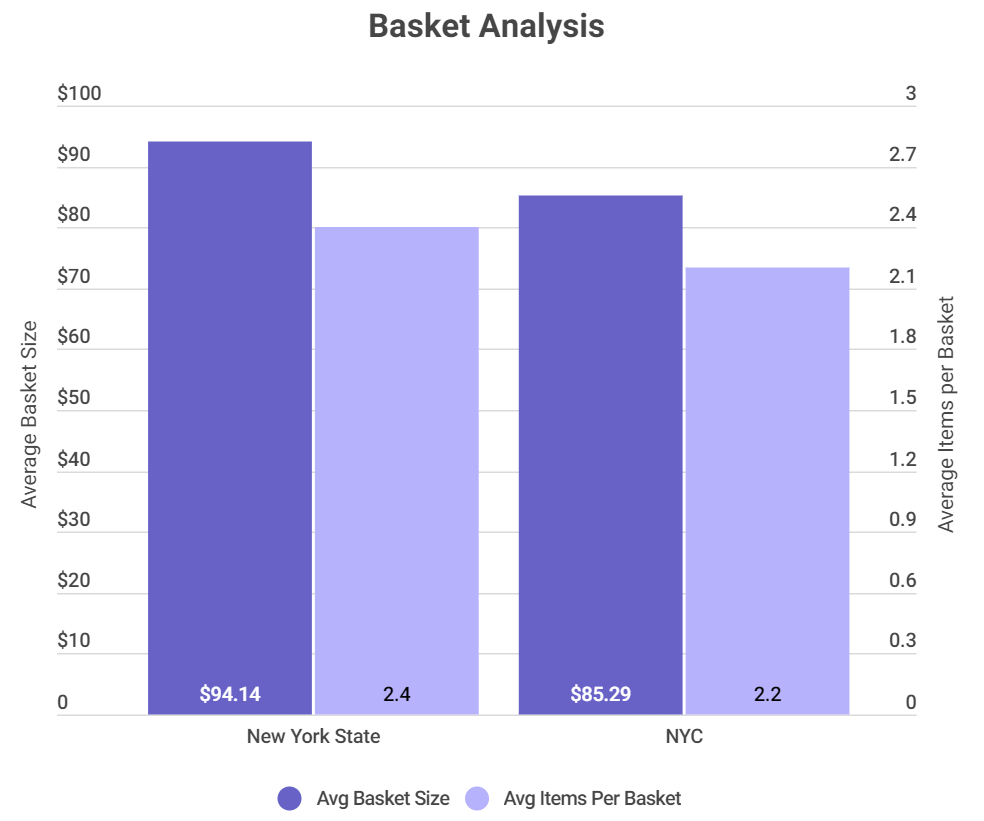

Cannabis Basket Size

The average basket in NYC is 9.4% lower than the rest of the state, $85.29 compared to $94.14 respectively. Contributing to the lower basket size is the slightly lower average item price in NYC ($38.02) likely a result of the category preferences mentioned above. The average number of items per basket is also a factor with NYC customers purchasing 2.2 items on an average trip compared to 2.4 items around the state. As NYC skews younger, it makes sense that they purchase fewer products, as older consumers generally spend more on cannabis.

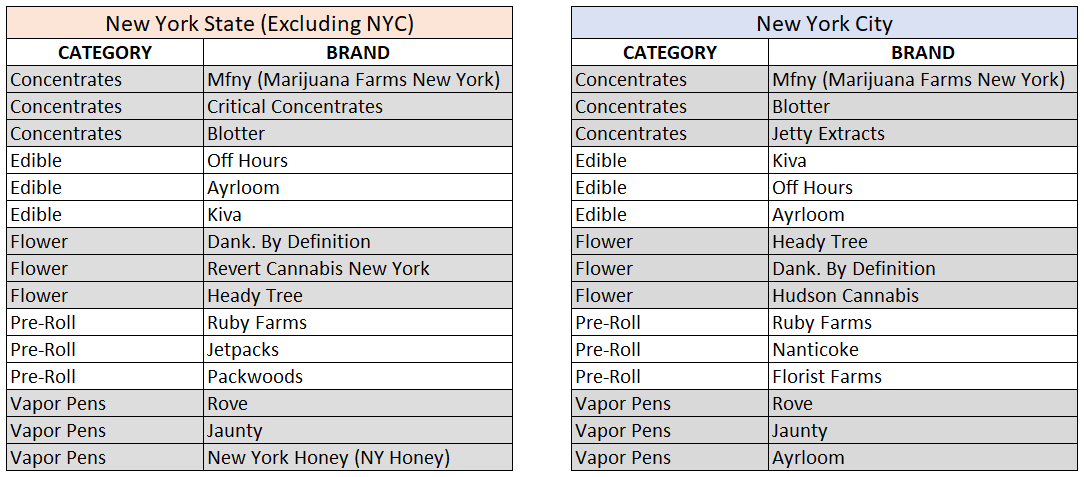

Top Cannabis Brands

Diversity in product offerings and brand specializations reflect the nuanced preferences of consumers across regions. A comparison between the statewide market and the bustling microcosm of New York City reveals fascinating trends in brand popularity and product choice. For instance, while Mfny and Blotter hold sway in both the state and city markets for concentrates, the presence of Jetty Extracts exclusively in NYC suggests a city-specific taste or perhaps a targeted distribution strategy. Similarly, the edibles category showcases a shared preference for Kiva and Off Hours, but the brand Ayrloom appears to cater specifically to the city's palate, pointing to potential regional variations in flavor profiles or branding that resonate more with urban consumers.

Moreover, the flower category, which is central to the cannabis experience, shows a mix of shared and unique preferences. Brands like Dank. By Definition and Heady Tree have managed to captivate users' preferences across the entire state as well as within the city, indicating a broad appeal that transcends regional differences. However, Hudson Cannabis seems to have found a niche or perhaps strategic exclusivity within New York City, hinting at the city's distinct consumer trends or urban-centric marketing efforts. The differentiation in the pre-roll and vapor pen categories further underscores the complex tapestry of the New York cannabis market. While Ruby Farms and Rove are popular choices for pre-rolls and vapor pens respectively across New York, brands like Nanticoke, Florist Farms, and Ayrloom for vapor pens are particularly notable within the New York City market, illustrating a more localized appeal or availability.

Headset customer Naturae, known for their Jaunty line, has been making significant strides in the New York market. Nicolas Guarino, CEO of Naturae, attributes their success to a couple of core principles.

Naturae is thriving in New York because we've doubled down on what matters: first a commitment to product quality and variety for our brand's consumers, and second a focus on fast and reliable service for our dispensary partners. That's what sets Jaunty and our other brands apart in this market right now, and what we will continue to anchor ourselves on as our brands evolve.

Demographics

With a median age of 37 in New York City, it's no surprise that millennials capture a larger portion of total sales than older urbanites. The scales balance in the rest of the state where Baby Boomers and Gen X see a larger representation than in the city. Additionally, women make up a larger demographic of total sales in NYC (32%) compared to the rest of the state (28%).

Conclusion

Limited retail options in NYC serve as a lightning rod to cannabis consumers in the city where retailers are seeing significantly higher average daily total sales than around the state. The younger millennial generation which drives nearly half of total sales nationwide is well represented in a youthful New York City while older patrons unsurprisingly are more represented around the state. This likely is a driving force in the category differences which shows a stronger preference for categories such as Edibles and Pre-Rolls in NYC, though the rest of the state more closely resembles the national category preferences.