Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Hudson Cannabis is stocked at 214 licensed dispensaries across New York, with the deepest coverage in New York, Syracuse, Albany, Buffalo, and Rochester. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

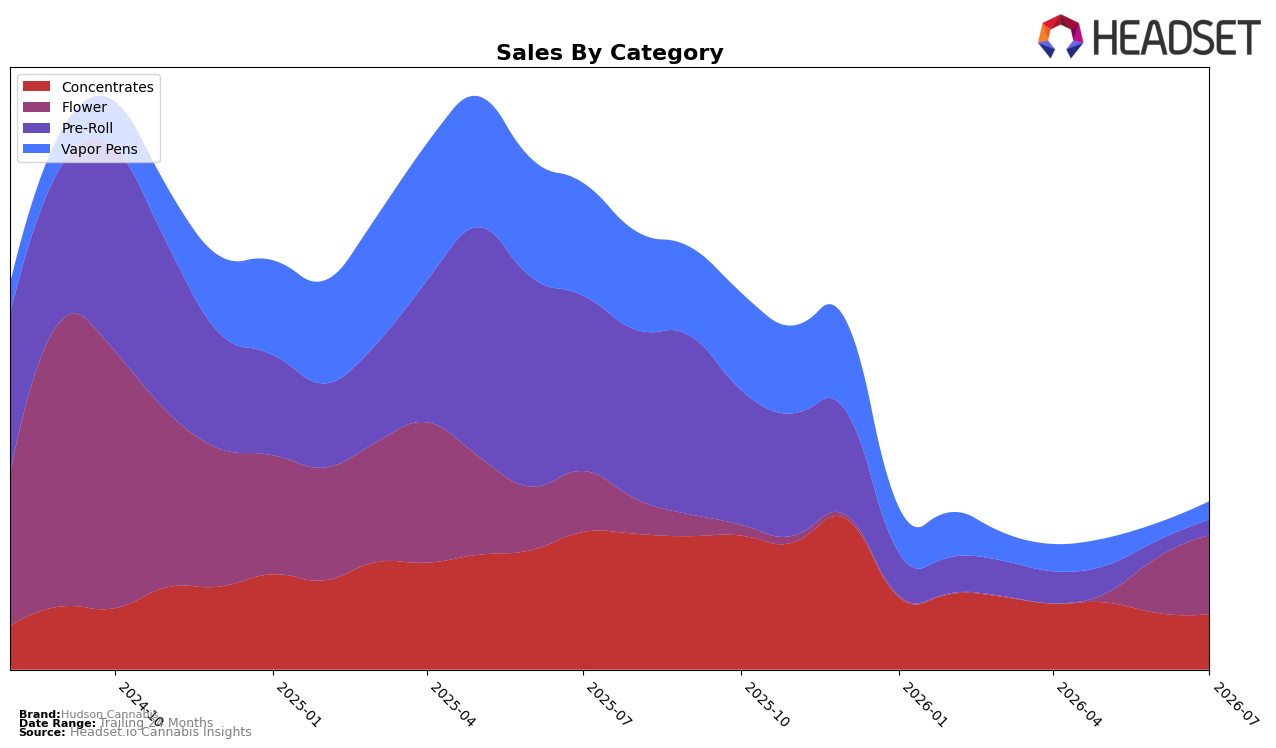

In July 2026, Hudson Cannabis shifted toward Flower, which rose to 46.78% share with 29.27% year-over-year growth and 40.83% month-over-month, while Concentrates contracted to 33.04% share with a -59.64% YoY and -1.60% MoM decline. Vapor Pens held 10.80% share with -83.90% YoY and a modest 3.20% MoM uptick, and Pre-Roll slipped to 9.38% share with -91.01% YoY and -6.06% MoM. Despite total brand sales down -65.45% YoY, the mix tilts toward higher-priced Flower at an average price of $133.10 and coincides with a 127.37% YoY jump in overall average price, implying a deliberate pivot to premiumized formats and away from lower-priced volume drivers.

This mix change positions Hudson Cannabis to compete on higher ticket baskets in New York Flower, where the brand ranks 56, but it raises exposure to demand elasticity as Concentrates and Pre-Roll volumes erode by -59.64% and -91.01% YoY while Flower grows 29.27%. With Vapor Pens down -83.90% YoY yet slightly up 3.20% MoM, and Concentrates nearly flat MoM at -1.60%, the near-term lift hinges on sustaining Flower’s 40.83% MoM surge without further cannibalizing the 43.22% combined share in Vapor Pens and Pre-Roll; the pattern implies a repositioning toward fewer, higher-priced units that can support margin but risks ongoing share loss in value-oriented segments.

Competitive Landscape

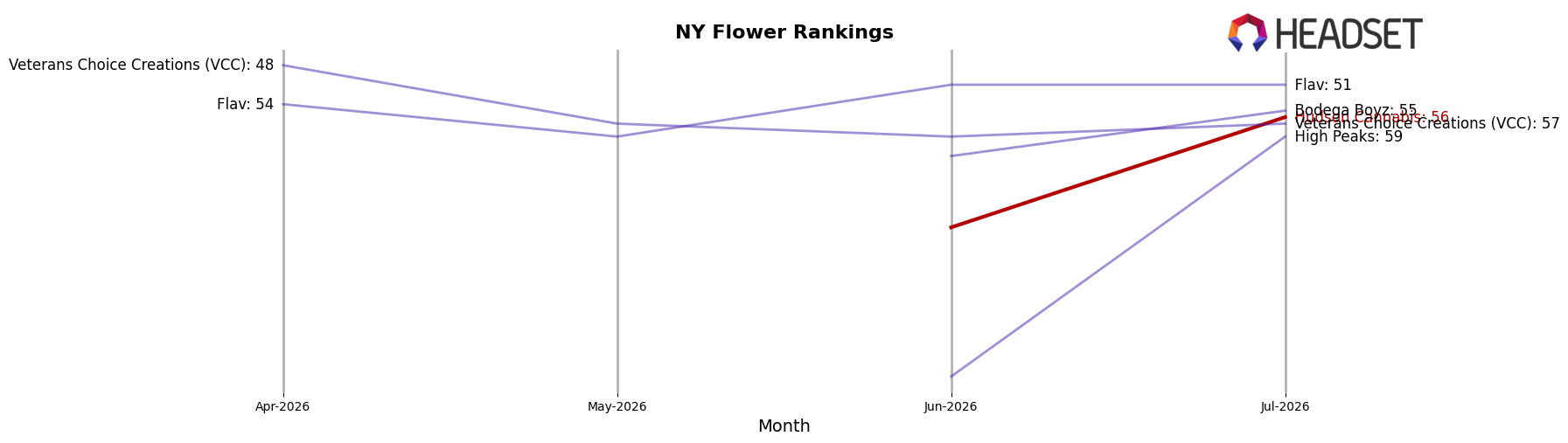

Hudson Cannabis sits at rank #56 in July 2026 in NY Flower, improving 6 positions from #62 year over year and rebounding 258 spots from #314 in April 2026, while still well below its peak at #11 in September 2024 and trailing the top tier where Find. moved up from #8 to #1 and Leal climbed from #7 to #2; the contrast with Dank. By Definition, which slid from #1 to #3 alongside a 51.55% sales decline, underscores that Hudson Cannabis’s upward rank change (+6 YoY) amid volatile leaders signals a stabilization phase rather than a return to its September 2024 peak trajectory.

Notable Products

Full Moon Hash (1g) posted the steepest decline in July 2026 at -62.3%, sliding to rank 6 while Sour Unicorn Infused Pre-Roll 7-Pack (3.5g) fell -23.7% at rank 5; this simultaneous drop alongside Lemon OG Haze (28g) rising 44.3% to rank 2 signals demand consolidating into large-format Flower at the expense of Concentrates and Infused Pre-Rolls. Sour Glue (28g) still held rank 1 despite an -11.1% MoM dip, and Garlic Bud (28g) climbed 38.2% into rank 10, meaning four of the top ten are Flower SKUs with mixed momentum but stronger rank security than other categories. With Concentrates occupying ranks 3, 4, 6, and 8 yet split between single-digit growth and double-digit declines, the category mix points to volatility around smaller-pack formats while 28g Flower absorbs share; the implication is a product strategy tilt toward high-volume Flower even if price-per-ounce pressure tempers dollar growth, as seen with one leader still over $67,000.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.