Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

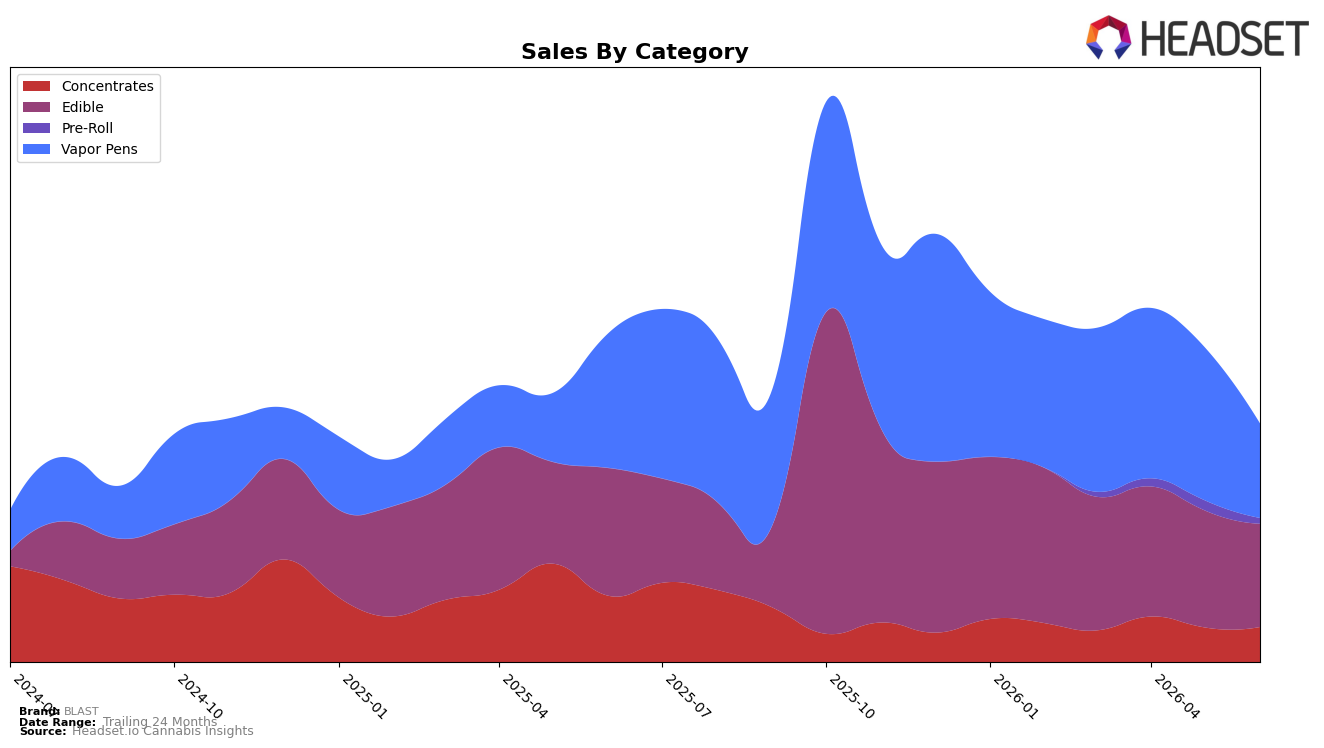

In June 2026, BLAST’s mix tilted toward Edible at 43.37% share (ranked 12 in Edible within British Columbia), while Vapor Pens contracted to 39.72% share; year over year Edible sales fell 19.14% and month over month declined 11.82%, whereas Vapor Pens dropped 29.74% YoY and 38.30% MoM. Concentrates held 14.60% share with a 47.45% YoY contraction but a 1.19% MoM uptick, and Pre-Roll sat at 2.32% share with a 43.98% MoM slide; at the brand level sales were down 27.51% YoY and average price dipped 0.83% YoY. The pattern implies BLAST is consolidating around lower-priced Edibles and retreating from higher-priced Vapor Pens in the short term, with a tentative floor forming in Concentrates as monthly declines stabilize.

The mix shift—Edible share up relative to Vapor Pens alongside a 0.83% YoY price decrease—suggests BLAST is leaning into value-led formats, which may defend volume but compress revenue if the 11.82% MoM Edible decline continues faster than the 38.30% MoM Vapor Pens pullback eases. With a 12th-place Edible rank in British Columbia and only 2.32% exposure to Pre-Roll after a 43.98% MoM drop, BLAST’s positioning hinges on stabilizing Edibles while nurturing the 1.19% MoM improvement in Concentrates to diversify risk. The implication is that near-term recovery depends on rebalancing toward categories with improving monthly momentum without over-indexing to segments showing accelerating monthly declines.

Competitive Landscape

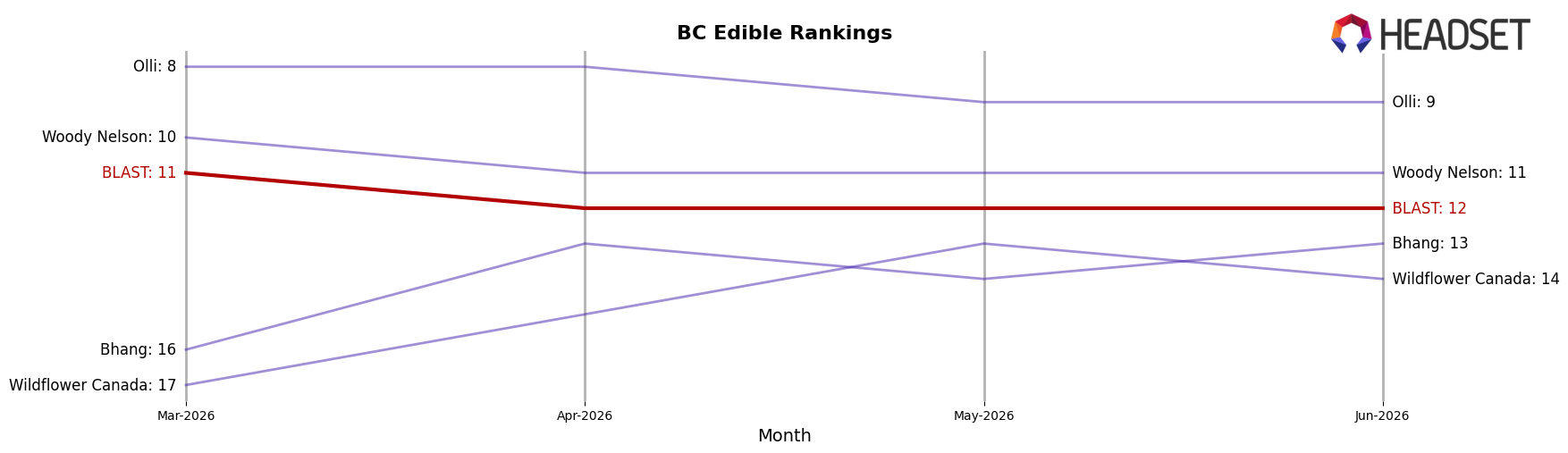

BLAST ranks #12 in BC Edible in June 2026, down 3 positions from #9 in June 2025, and 1 position from #11 in March 2026, while its prior peak was #3 in October 2025; meanwhile, Spinach holds #1 after rising from #2 year over year and Gron / Grön slipped from #1 to #3 as its sales fell 11.0%, indicating BLAST’s slide is occurring as leaders consolidate share at the top. Compared with No Future climbing from #3 to #2 on 94.0% sales growth and Wyld holding #4 with 118.2% growth, BLAST’s downward rank change of 3 places year over year alongside a 1-place quarter-over-quarter dip implies the brand is losing relative velocity to faster-growing competitors and needs a catalyst to reenter the top 10.

Notable Products

Death Bubba Distillate Cartridge (1g) posted the steepest decline at -65.92% month over month to rank 10, while Cosmic Cotton Candy Live Resin Cartridge (1g) fell -35.29% to rank 5, signaling a vapor-pen reset that shifts mix away from quick-turn SKUs and toward higher-margin edibles. At the top, Animal Style Sour Wild Raspberry Live Rosin Gummy (10mg) held rank 1 despite a -0.42% dip, whereas CBN/THC 1:1 Lunar Eclipse Lemon Chamomile Live Rosin Gummy (10mg CBN, 10mg THC) slid -16.09% at rank 3, and four of the top ten are Edible SKUs despite mixed MoM trajectories. The contrast between a +21.18% move for CBG/THC 1:1 Solar Eclipse Gummy (10mg CBG, 10mg THC) at rank 4 and a -48.14% drop for Sour Wild Raspberry Live Rosin Gummies 10-Pack (100mg) at rank 8 implies dosage format and functional positioning, rather than flavor alone, is determining share capture. Taken together, the concentration in Edibles alongside steep Vapor Pens pullbacks points to BLAST tilting assortment and demand toward functional gummies over inhalables for June 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.