Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

FloraCal Farms is stocked at 306 licensed dispensaries across Illinois, Massachusetts, and 5 other states, 149 of them in Illinois, with the deepest coverage in Chicago, East Peoria, Normal, Addison, and Arlington Heights. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

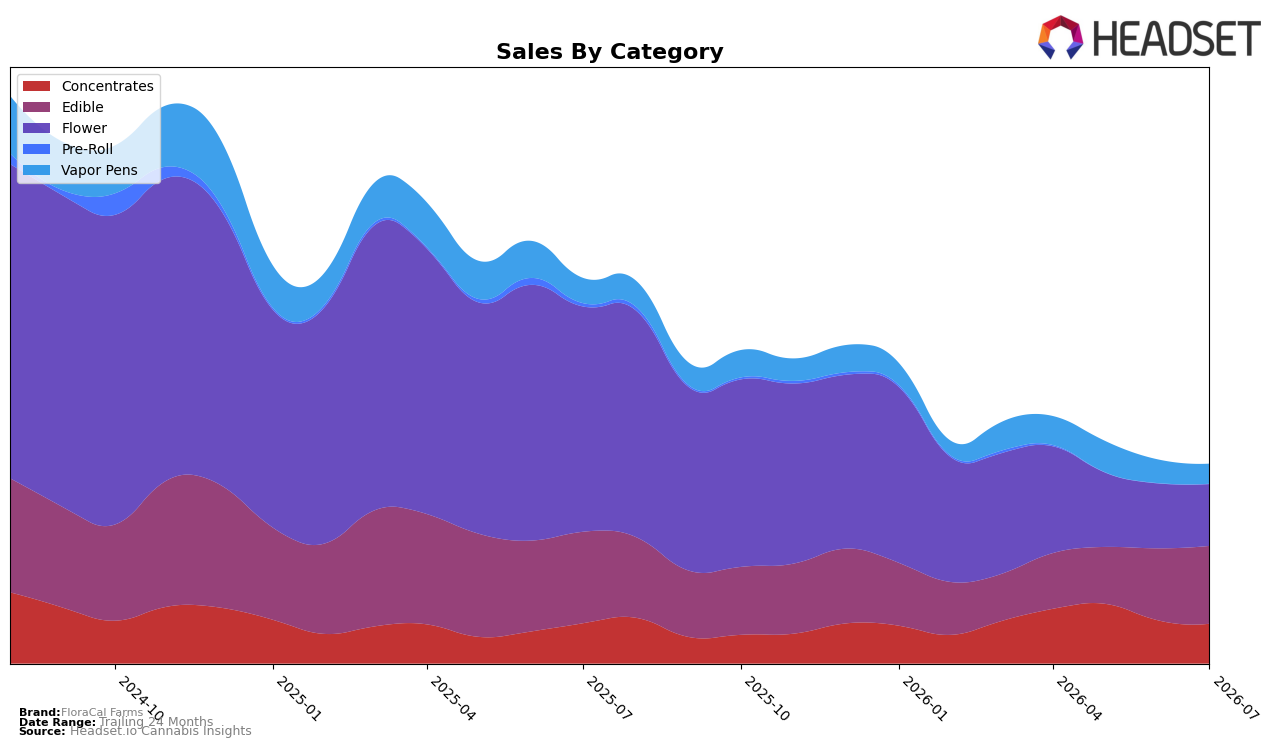

In July 2026, FloraCal Farms’ mix tilted toward Edible at 39.06% share with month-over-month growth of 8.11% despite a year-over-year decline of 14.95%, while Flower fell to 31.00% share with a 4.73% MoM drop and a 72.65% YoY contraction. Concentrates held 19.96% share with a modest 1.35% YoY decline but a 7.95% MoM dip, and Vapor Pens represented 9.98% share with a 15.30% MoM pullback and a 20.65% YoY decrease. With brand sales down 48.34% YoY and average price down 13.89%, the shift toward lower-priced Edible ($18.27) and away from Flower ($31.09) implies a defensive pivot toward value-led formats that can stabilize volume but compress premium positioning.

Given a Flower category rank of 53 in Illinois and a 72.65% YoY decline in Flower alongside an 8.11% MoM rise in Edible, July 2026 signals FloraCal Farms leaning into categories with steadier or recovering velocity to offset Flower exposure. The relatively shallow 1.35% YoY decline in Concentrates versus a 20.65% YoY decline in Vapor Pens indicates a narrower focus on higher-ticket, niche formats over broadly discounted inhalables, which, coupled with a 13.89% brand-wide price reduction, suggests repositioning from premium Flower leadership toward a portfolio anchored by Edible resilience and Concentrates margin balance.

Competitive Landscape

FloraCal Farms is ranked #53 in Illinois Flower in July 2026, down 22 positions year over year from #31, and 12 spots lower than April 2026’s #41, while still far from its peak of #21 set in July 2024; in contrast, High Supply / Supply held #1 with a -3.0% YoY sales change and RYTHM stayed at #2 with +20.8% YoY growth, indicating share is consolidating at the top as FloraCal Farms drifts downward. The brand’s two-step slide from April 2026 to July 2026 and the 22-rank YoY drop, alongside competitors like &Shine rising from #8 to #4 with +87.4% YoY sales, implies that without a turnaround in velocity or assortment, FloraCal Farms’ trajectory points toward further mid-pack erosion rather than a near-term re-entry into the top 30.

Notable Products

Morning Dew (3.5g) posted the steepest movement in July 2026 with a -43.1% month-over-month drop and sat at rank 7, while Blue Sapphire (3.5g) also contracted by -30.9% at rank 8. In contrast, Tropical Punch Live Rosin Gummies 10-Pack (100mg) grew 10.8% to rank 3 and Wild Berry Live Rosin Gummies 10-Pack (100mg) rose 7.9% at rank 2, creating a split where edibles advanced as multiple flower SKUs retreated. Four of the top ten are Edible SKUs led by Pink Lemonade Live Rosin Gummies 10-Pack (100mg) at rank 1 with a -2.7% dip and Strawberry Jam Live Rosin Gummies 10-Pack (100mg) up 9.1% at rank 5, concentrating share in Live Rosin gummies even as Purple Plague (3.5g) climbed 35.8% to rank 4. This pattern implies FloraCal Farms is tilting toward a gummies-led mix for volume while flower becomes more selective by strain performance, with dollar leadership still diversified across categories at $70,222 for Purple Plague (3.5g).

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.