Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

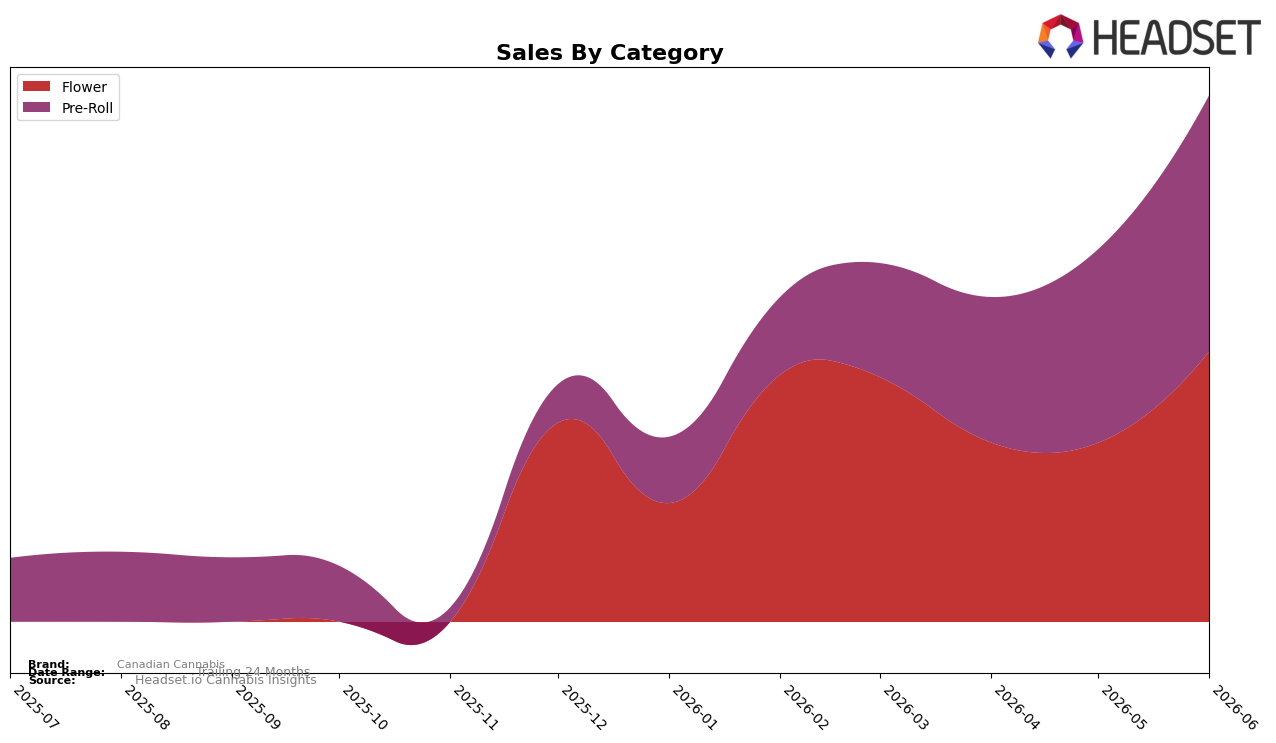

Canadian Cannabis concentrated in two categories in June 2026, with Flower at 51.35% share and Pre-Roll at 48.65%, and month-over-month growth diverging as Flower rose 50.98% while Pre-Roll increased 32.46%. The brand’s category footprint is effectively a split portfolio, yet the faster 18.52 percentage-point gap in MoM growth favors Flower while keeping total mix balanced within 2.70 percentage points, implying the brand leaned into higher-velocity Flower without abandoning Pre-Roll. With a Flower rank of 12 in Alberta and an average Flower price of $53.81 against a portfolio average price of $21.07, the combination of a double-digit rank position and a wider price ladder implies headroom to trade customers between value and premium tiers.

The acceleration skew toward Flower (+50.98% MoM) versus Pre-Roll (+32.46% MoM), while maintaining a near-even mix (51.35% vs. 48.65%), implies a positioning that can pivot toward Flower-led acquisition while using Pre-Roll to sustain breadth without diluting focus. Holding a 12th-place Flower rank in Alberta alongside a 2.70 percentage-point spread in category share suggests the brand can climb the Flower ladder by converting marginal Pre-Roll buyers, while the $53.81 average in Flower relative to the $21.07 overall average indicates room to upweight higher-price Flower without overexposing the mix to price sensitivity.

Competitive Landscape

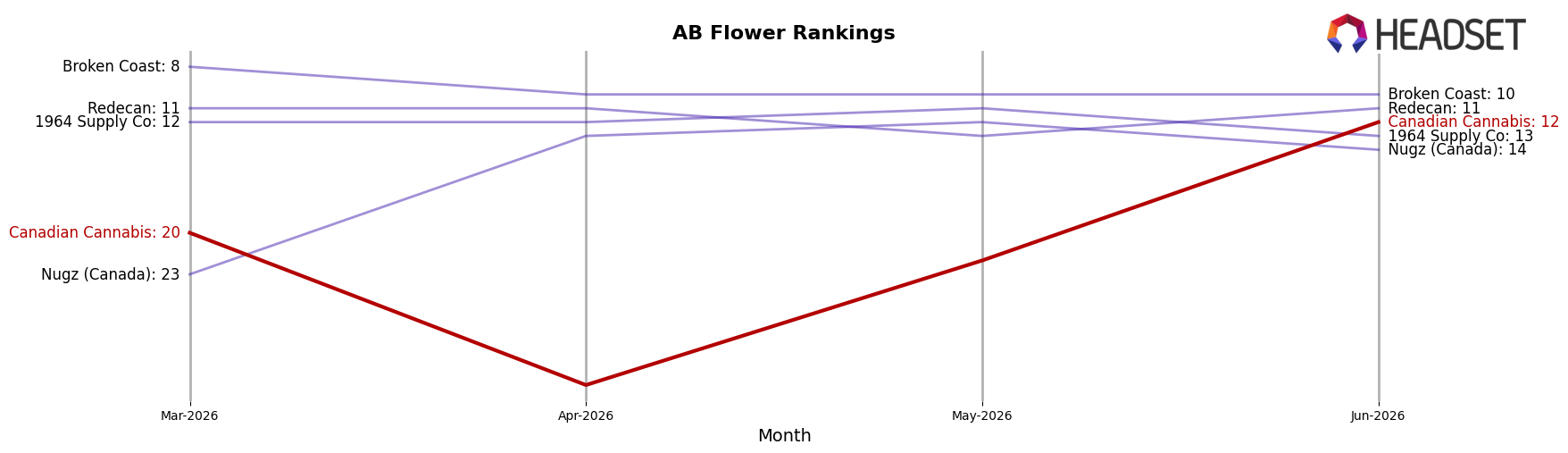

Canadian Cannabis sits at rank #12 in AB Flower in June 2026, a climb of 8 positions from #20 in March 2026, marking its peak rank to date at #12 while the year-over-year rank change is unavailable. Against market leaders, Pure Sunfarms moved up to #1 with a +4 YoY rank shift and +20.1% sales growth, whereas Good Supply slipped to #5 with a -1 YoY rank move and -41.0% sales change; in contrast, Big Bag O' Buds advanced to #3 with a +7 YoY rank shift and +35.0% sales growth. The combination of an 8-place rise over three months and a first-time peak at #12 implies Canadian Cannabis is gaining placement momentum but must convert that momentum into share against leaders improving rank and growth simultaneously.

Notable Products

Organic Thunder Zkittlez Pre-Roll 10-Pack (5g) posted the standout move in June 2026 with a +148.6% month-over-month surge to rank 2, while Mango Hashplant Pre-Roll (0.5g) slid -15.3% to rank 8. Apex Kush Pre-Roll (0.5g) inched up +2.0% at rank 1, and Indica Eh! Pre-Roll 2-Pack (2g) advanced +61.8% at rank 6, indicating momentum concentrated in value or multipack pre-rolls versus single sticks. Seven of the top ten are Pre-Roll SKUs, and two Organic Thunder Zkittlez variants sit inside the top five, signaling a family-led halo effect across pack sizes. This mix implies Canadian Cannabis is tilting commercial focus toward multi-pack pre-roll depth while maintaining a flagship single Pre-Roll at the top to capture both basket-building and trial-oriented shoppers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.