May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

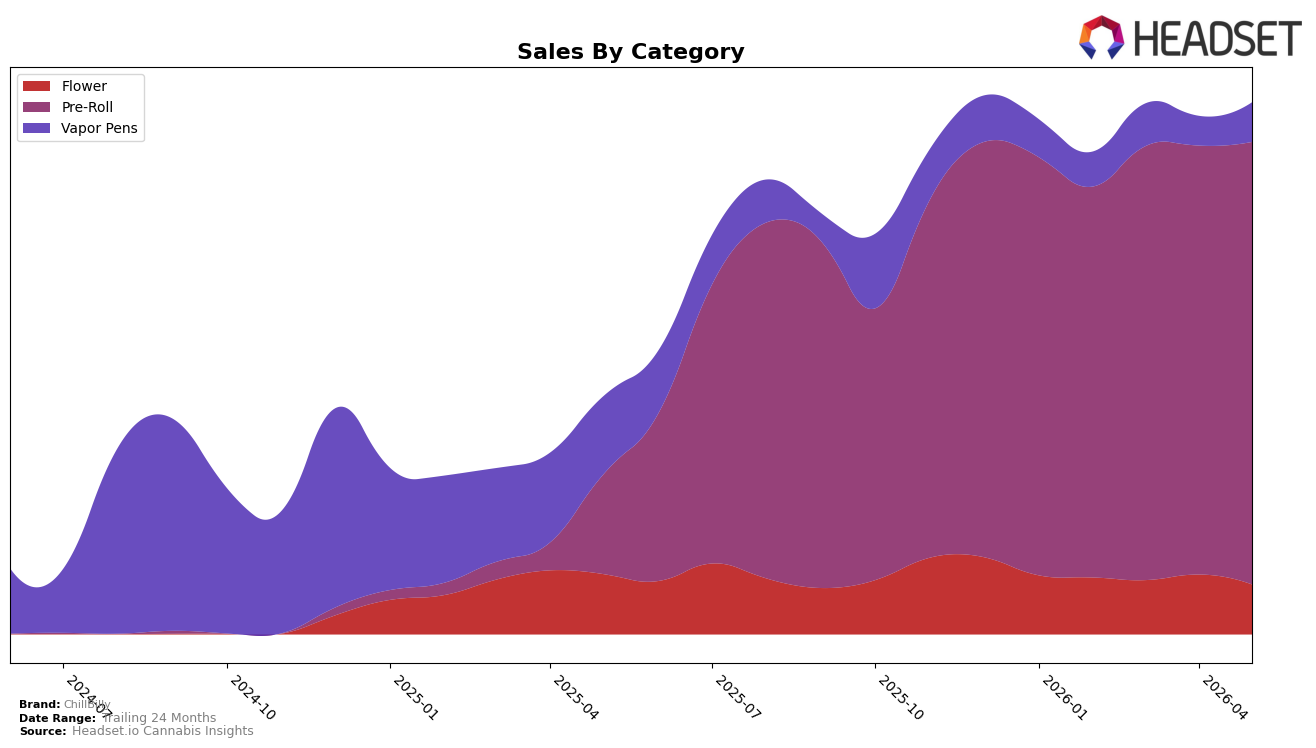

ChillBilly concentrated 83.26% of May 2026 sales in Pre-Roll, where category sales grew 344.92% year over year and 3.16% month over month, while Flower fell 17.24% YoY and 16.62% MoM to 9.35% share. Vapor Pens held 7.39% share with a 49.57% YoY decline but a 33.56% MoM rebound, indicating a tactical swing rather than sustained contraction; paired with a 16.20% YoY drop in average price to $27.07, the mix suggests price-based capture in Pre-Roll offsetting Flower attrition. The pattern implies ChillBilly is leaning into Pre-Roll scale at lower price points to drive volume while using a selective MoM push in Vapor Pens to stabilize overall mix despite ongoing Flower compression.

With Pre-Roll anchored at rank 25 in British Columbia, the 3.16% MoM Pre-Roll growth alongside a 33.56% MoM lift in Vapor Pens positions ChillBilly to trade shoppers within inhalables rather than reclaim Flower, which dropped 16.62% MoM. The combination of an 83.26% Pre-Roll share and a 49.57% YoY contraction in Vapor Pens signals portfolio polarization toward value-led Pre-Roll and opportunistic, promotion-responsive Vapor Pens; the implication is that maintaining or improving rank 25 will depend more on sustaining Pre-Roll price elasticity gains than reversing the 17.24% YoY Flower decline.

Competitive Landscape

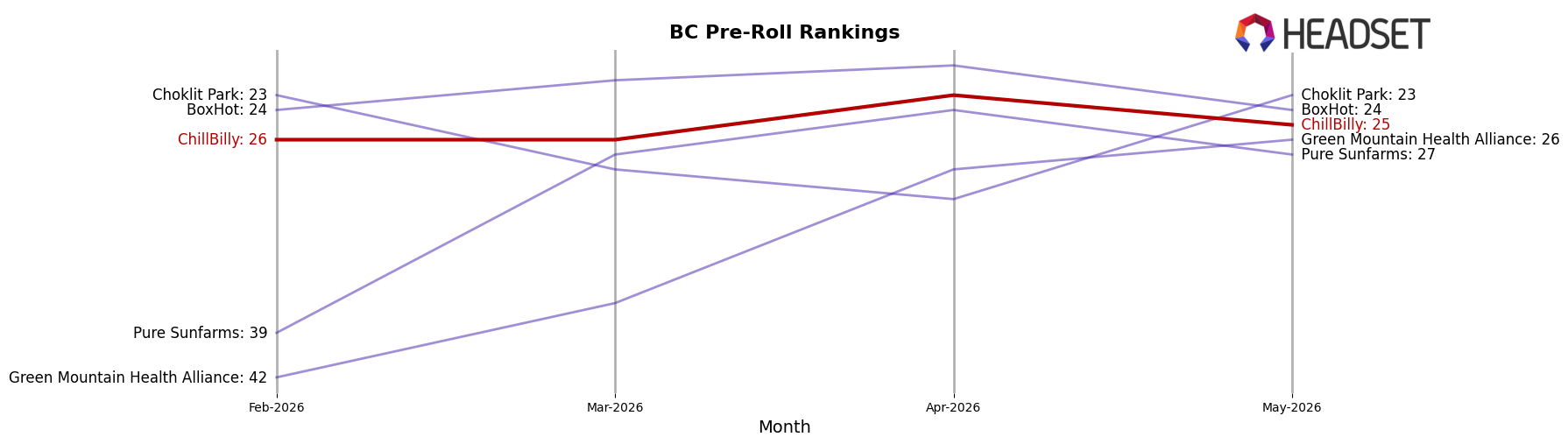

ChillBilly sits at rank 25 in BC Pre-Roll in May 2026, an improvement of 32 positions from rank 57 year over year, and a 1-spot lift from rank 26 three months ago; however, the brand’s peak rank of 23 in April 2026 indicates only a 2-position pullback month over month. Against leaders, General Admission held rank 1 year over year and remains rank 1 with 3.8% YoY sales growth, while BC Doobies climbed from rank 7 to rank 2 alongside 111.5% YoY sales growth, outpacing ChillBilly’s rank momentum; this mix of steady incremental gains (26 to 25) and a large YoY leap (57 to 25) implies ChillBilly is moving from fringe presence toward mid-tier relevance, but needs additional velocity to convert April 2026’s peak at rank 23 into a sustained top-20 foothold.

Notable Products

Max 60's- Rowdy Variety Pack Infused Pre-Roll 3-Pack (1.35g) delivered the standout movement in May 2026 with a 160% month-over-month surge, vaulting into rank 6 while 50 Cal- Gator Blood Double Infused Pre-Roll (2g) plunged 42% to rank 7; this bifurcation signals consumers trading toward variety-led value over single-stick novelty. At the top, Max 60's - Frosted Grape Triple Infused Pre-Roll 3-Pack (1.35g) held rank 1 with a 17% lift while Max 60's - Blood Orange Triple Infused Pre-Roll 3-Pack (1.35g) slid 9% yet stayed at rank 4, implying flavor rotation within the same format without eroding the flagship’s share. Six of the top ten are Pre-Roll SKUs and occupy ranks 1 through 8 except for two Vapor Pens at ranks 9 and 10 with roughly flat MoM near +1%, suggesting ChillBilly’s near-term volume and pricing leverage concentrate in infused Pre-Rolls over Vapor Pens, with one outsized gainer offsetting a steep decliner.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.