May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

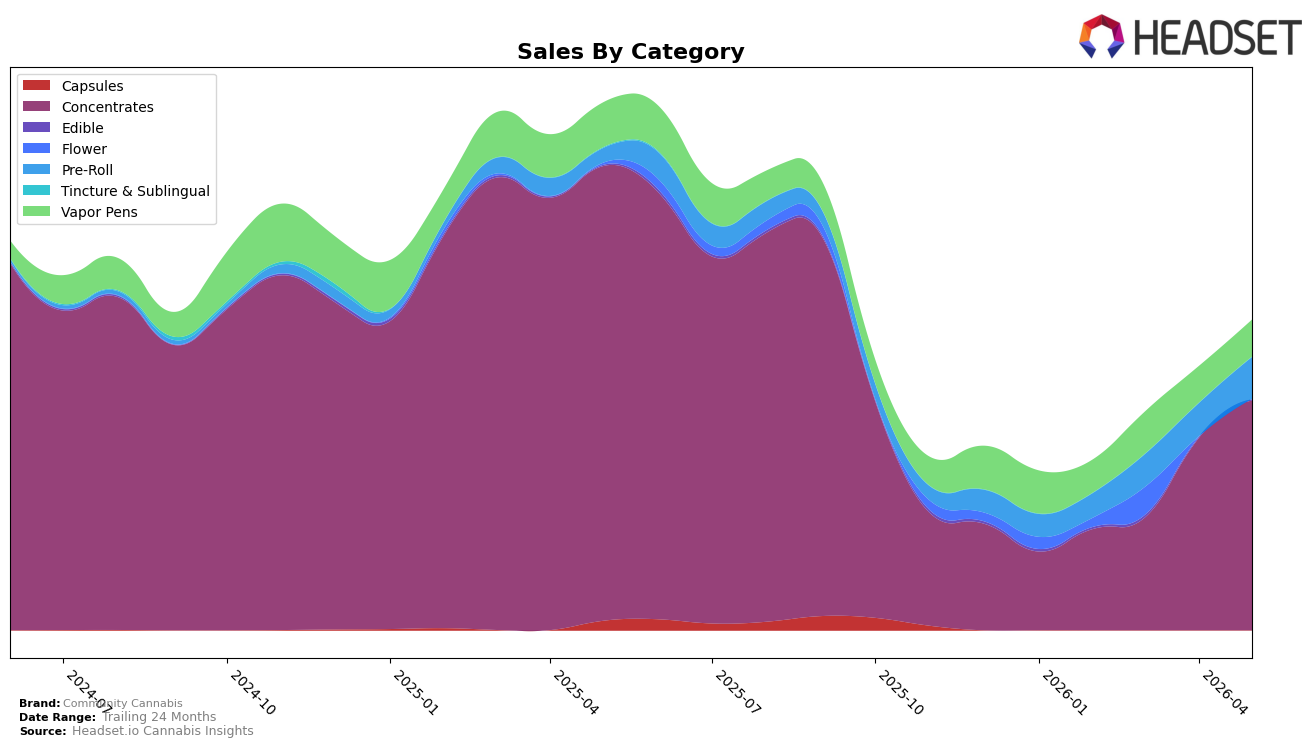

Community Cannabis concentrated 74.38% of May 2026 sales in Concentrates (rank 20 in California), where sales fell 49.56% year over year but rose 19.48% month over month, while Vapor Pens held 11.87% share with a 17.76% YoY decline and a 0.73% MoM uptick. Pre-Roll expanded to 13.46% share on 190.57% YoY growth and 26.57% MoM growth, and Edible, though just 0.29% share, advanced 13.09% YoY and 22.24% MoM; taken together with a 37.56% YoY drop in average price to $23.48, the mix shows reliance on a recovering Concentrates base alongside faster-growing, lower-priced Pre-Roll. The pattern implies a pivot opportunity: sustained MoM gains in Concentrates and Pre-Roll can offset the brand’s overall 41.37% YoY sales decline if mix continues shifting toward categories with triple-digit YoY or double-digit MoM increases.

With Concentrates still three-quarters of volume yet down 49.56% YoY versus Pre-Roll up 190.57% YoY, the brand’s positioning is tilting from a single-category anchor toward a two-pillar strategy where Pre-Roll and steady Vapor Pens (+0.73% MoM) provide volatility buffering. The 19.48% MoM rebound in Concentrates coupled with 26.57% MoM in Pre-Roll indicates near-term elasticity to price and format, and the category split suggests emphasizing accessible pack sizes in Pre-Roll while selectively defending rank 20 in California Concentrates; this mix shift implies Community Cannabis can trade some share of wallet from high-ticket Concentrates to higher-velocity Pre-Roll to stabilize monthly comps while rebuilding depth in its top category.

Competitive Landscape

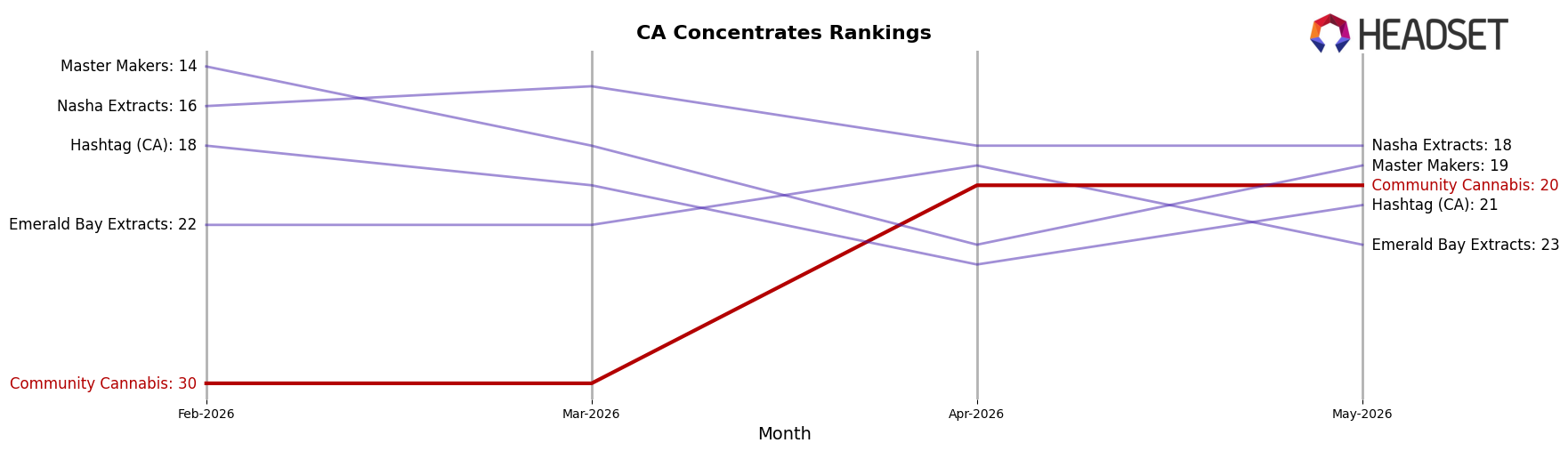

Community Cannabis ranks #20 in CA Concentrates in May 2026, down 11 positions year over year from #9, and up 10 ranks since February 2026 when it was #30; this sits well below its peak of #8 in April 2025 and trails category leaders with contrasting momentum. Raw Garden holds #1 with a 0-rank YoY change and sales up 11.3%, while Community Cannabis’s YoY rank slide of 11 contrasts with STIIIZY at #2, which kept its position year over year despite a 23.8% sales decline. Against mid-tier movers, 710 Labs improved its rank from #4 to #3 with sales down 1.8%, and Punch Extracts / Punch Edibles slipped from #3 to #4 alongside a 29.9% sales contraction; these mixed shifts indicate that Community Cannabis’s recovery from #30 to #20 over three months is momentum-driven but not yet durable enough to reverse the 11-position YoY decline.

Notable Products

Bird Watchers Blunt 2-Pack (2g) posted the sharpest move in May 2026 with a +74.2% month-over-month surge and reached rank 2, while Honey Grapes Cold Cure Live Rosin (1g) fell -40.2% and slid to rank 9. Purple Hills Pre-Roll 2-Pack (2g) held rank 1 with +11.2% MoM growth, and Blue Milk Cold Cure Live Rosin (1g) dropped -34.6% to rank 4. Four of the top ten are Concentrates SKUs, yet the two highest ranks are Pre-Rolls, implying a pivot toward accessible inhalables even as premium rosin volatility persists.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.