May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

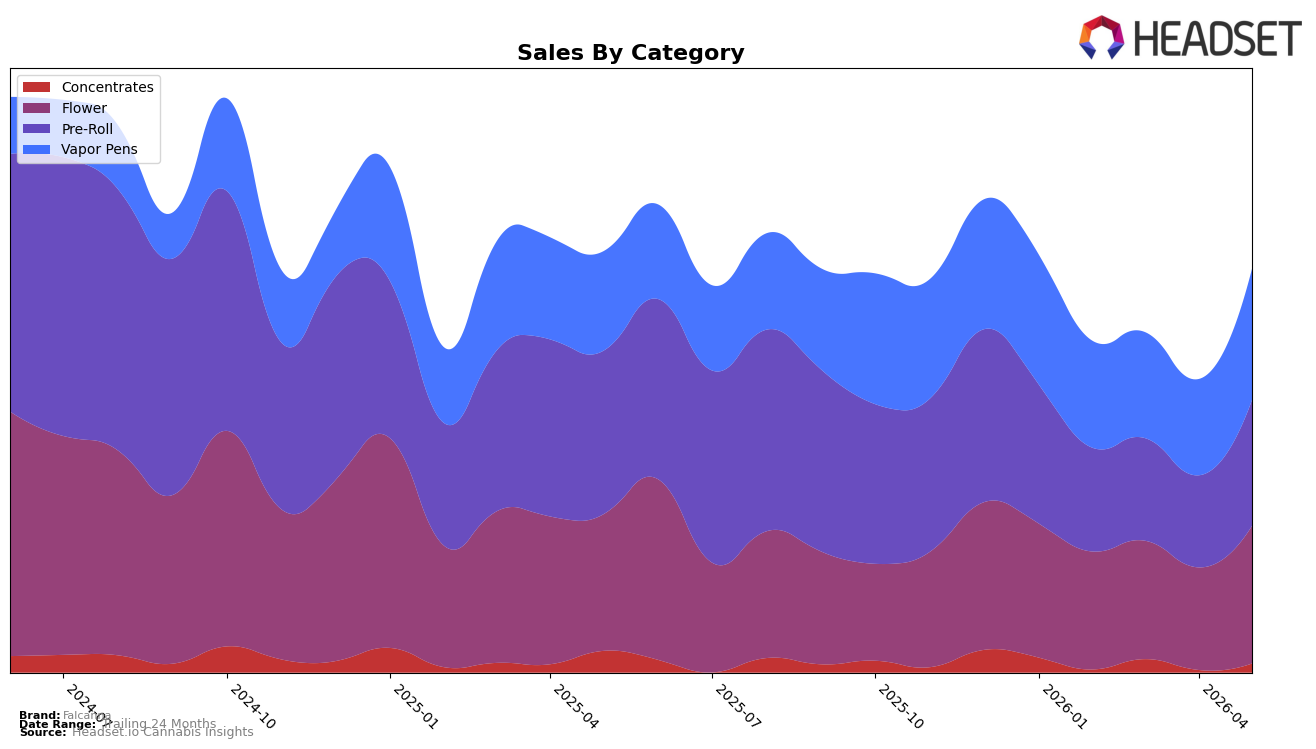

In May 2026, Falcanna’s mix concentrated in Flower at 30.53% share and Vapor Pens at 29.57% share, with Pre-Roll close behind at 28.75%, while Concentrates held 11.15% share; within this, Flower grew 20.96% MoM and 0.52% YoY as Vapor Pens advanced 21.72% MoM and 19.31% YoY. Pre-Roll slipped 16.49% YoY despite a 21.54% MoM uptick, and Concentrates declined 14.64% YoY with a 9.59% MoM lift; the brand’s average price fell 2.98% YoY to $14.68 even as the top-category Flower averaged $21.39. The pattern implies Falcanna is reallocating volume toward higher-velocity inhalables—especially Vapor Pens—while offsetting Pre-Roll’s YoY drag with short-term MoM gains, a shift that can stabilize total sales despite a brand-level YoY decline of 2.58%.

Positioning-wise, a 44 rank in Flower in Washington alongside a 19.31% YoY rise in Vapor Pens suggests Falcanna’s near-term edge rests more in cartridges than in dried bud, while Pre-Roll’s 16.49% YoY contraction indicates weakening pull for value-led formats even with a $9.19 average price. With Vapor Pens at 29.57% mix and Flower just ahead at 30.53%, the brand sits on a near-dual core, and the simultaneous 20%+ MoM surges in both Vapor Pens and Flower point to a merchandising and assortment stance that leans into faster-turn premium inhalables rather than expanding lower-margin Pre-Rolls or slower Concentrates. The implication is that defending share will depend on reinforcing the Vapor Pens proposition and selective Flower differentiation rather than chasing Pre-Roll volume, using the current price architecture to trade consumers into categories showing 20.96%–21.72% MoM momentum.

Competitive Landscape

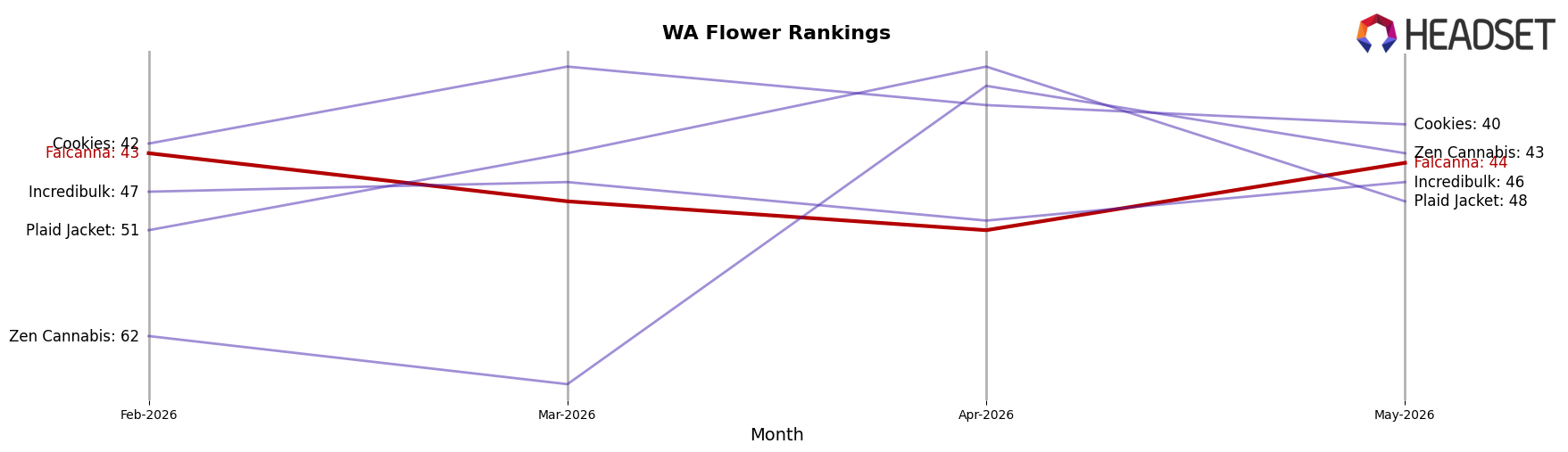

Falcanna sits at rank #44 in WA Flower in May 2026, down 1 spot year over year from #43, and flat versus February 2026 at #43; this contrasts with Lifted Cannabis Co climbing from #7 to #3 and posting a 16.9% YoY sales increase, while Legends held #2 with a 26.8% YoY sales decline. The brand’s current position is 15 ranks below its peak at #29 in June 2024, and it now trails the category leader Phat Panda at #1 despite that competitor’s 7.7% YoY contraction; taken together, the 1-rank YoY slip and the 15-rank gap from peak imply a drift toward the middle tier unless there is a near-term share recovery.

Notable Products

Deep Sea Live Resin HTE Ceramic Cartridge (1g) posted the single largest movement in May 2026 with a 53.3% month-over-month gain and climbed into rank 9, while Deep Sea Pre-Roll 2-Pack (1.2g) fell 8.5% MoM and sat at rank 8. Diesel Thai Pre-Roll 2-Pack (1.2g) rose 43.0% MoM to rank 1 and Candy Queen Live Resin Cartridge (1g) advanced 29.2% MoM at rank 6, yet Vapor Pens collectively occupied three of the top ten with double-digit gains including a $12,893 month total for Deep Sea Live Resin HTE Ceramic Cartridge (1g). With seven of the top ten labeled as Pre-Roll SKUs but the fastest growth concentrated in Vapor Pens, the mix implies Falcanna is pivoting toward higher-velocity cartridges as the incremental volume engine while keeping Pre-Rolls as rank-stabilizing anchors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.