Where to Buy

FENO is stocked at 25 licensed dispensaries across Arizona, with the deepest coverage in Tucson, Phoenix, Chandler, Glendale, and Avondale. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

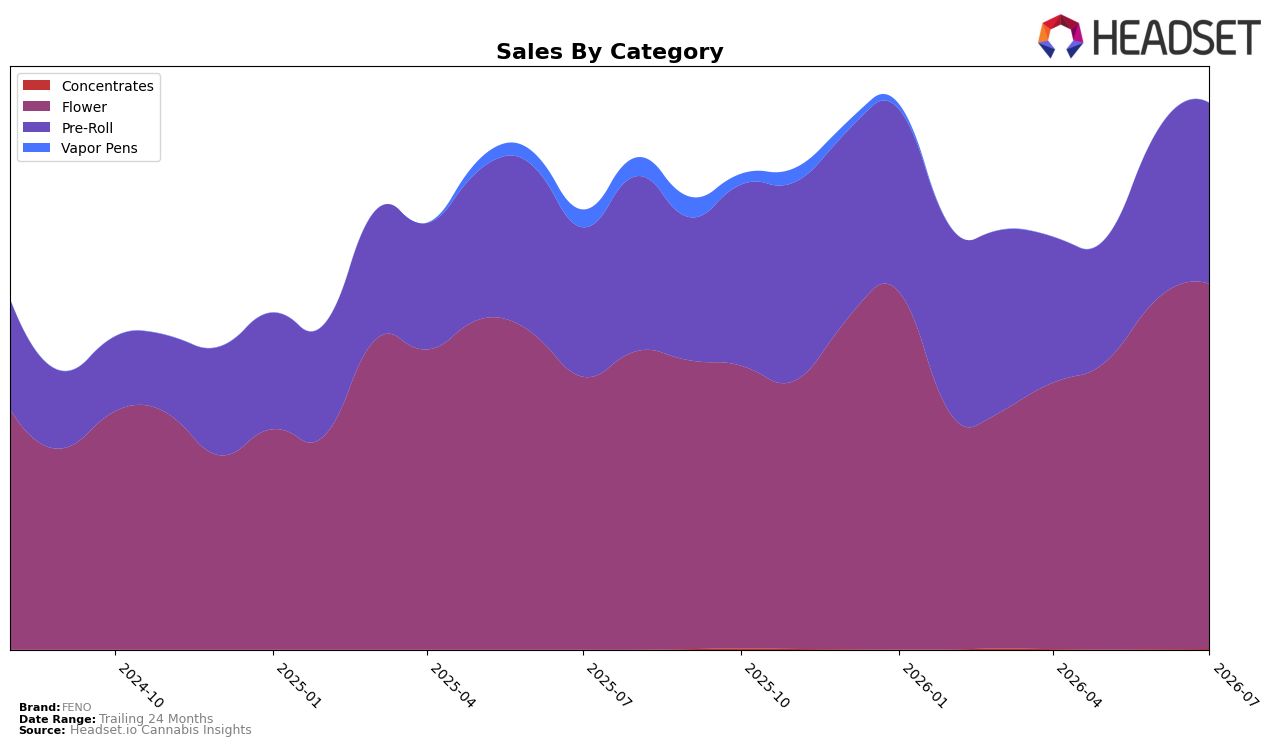

Market Insights Snapshot

FENO’s category mix in July 2026 tilted toward Flower at 66.81% share with year-over-year growth of 33.83% and month-over-month growth of 4.04%, while Pre-Roll held 33.06% share with 21.06% year-over-year growth and 7.36% month-over-month growth; Concentrates remained marginal at 0.13% share despite a 44.25% month-over-month lift. Overall brand sales rose 24.32% year over year as average price fell 5.33%, and Flower’s rank in Arizona stood at 16. The pattern implies FENO is leaning into volume-led gains in Flower and Pre-Roll, using lower average prices alongside rising mix weights to expand throughput without diluting the Flower anchor that supports state-level ranking.

With Flower at 66.81% share and ranking 16 in Arizona, and Pre-Roll at 33.06% share growing 7.36% month over month, the brand’s mix concentrates on two adjacent inhalable formats while keeping Concentrates at 0.13%. The combination of a 5.33% average price decline and 24.32% year-over-year sales growth in July 2026 suggests a price-to-volume trade that reinforces Flower’s shelf presence while allowing Pre-Roll to absorb incremental demand, implying FENO is positioning as a value-accessible inhalables specialist rather than diversifying into small, premium niches.

Competitive Landscape

FENO is ranked #16 in AZ Flower in July 2026, improving 11 positions from #27 year over year, and climbing 12 ranks from #28 in April 2026 to its peak at #16 in July 2026; this places the brand outside the top 15 while leaders like Just Flower held #1 with a 21.8% year-over-year sales increase and Brown Bag advanced from #5 to #4 alongside a 79.0% year-over-year lift. Against mid-tier rivals, Fenix slipped from #4 to #5 with a 6.9% year-over-year sales decline while FENO moved from #27 to #16, and Find. held #2 with a 0.7% year-over-year uptick, indicating FENO’s rank gains are outpacing brands with flat or negative growth but still lagging the acceleration seen among top-5 climbers; the trajectory implies FENO has transitioned from lower-tier visibility toward a competitive mid-pack position, with further share capture needed to cross into the top 10.

Notable Products

Big MC (5.5g) posted the standout movement with a 90.9% month-over-month surge to rank 2, while Crescendo Pre-Roll 5-Pack (3.5g) slipped 13.5% to rank 5, creating a widening gap between Flower and Pre-Roll momentum. Culiacancito Pre-Roll 5-Pack (3.5g) held rank 1 with a 23.4% gain and Grape Gas Pre-Roll 5-Pack (3.5g) climbed 31.9% at rank 4, yet five of the top ten are Pre-Roll SKUs, indicating depth but slower velocity at the category’s middle. With Jenny Kush (5.5g) entering at rank 8 and $51,392, Flower now accounts for three of the top eight positions and the only >50% mover, implying FENO’s product mix is tilting toward larger-pack Flower as the primary growth engine in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.