Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

22Red is stocked at 47 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Mesa, Tucson, Glendale, and Tempe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

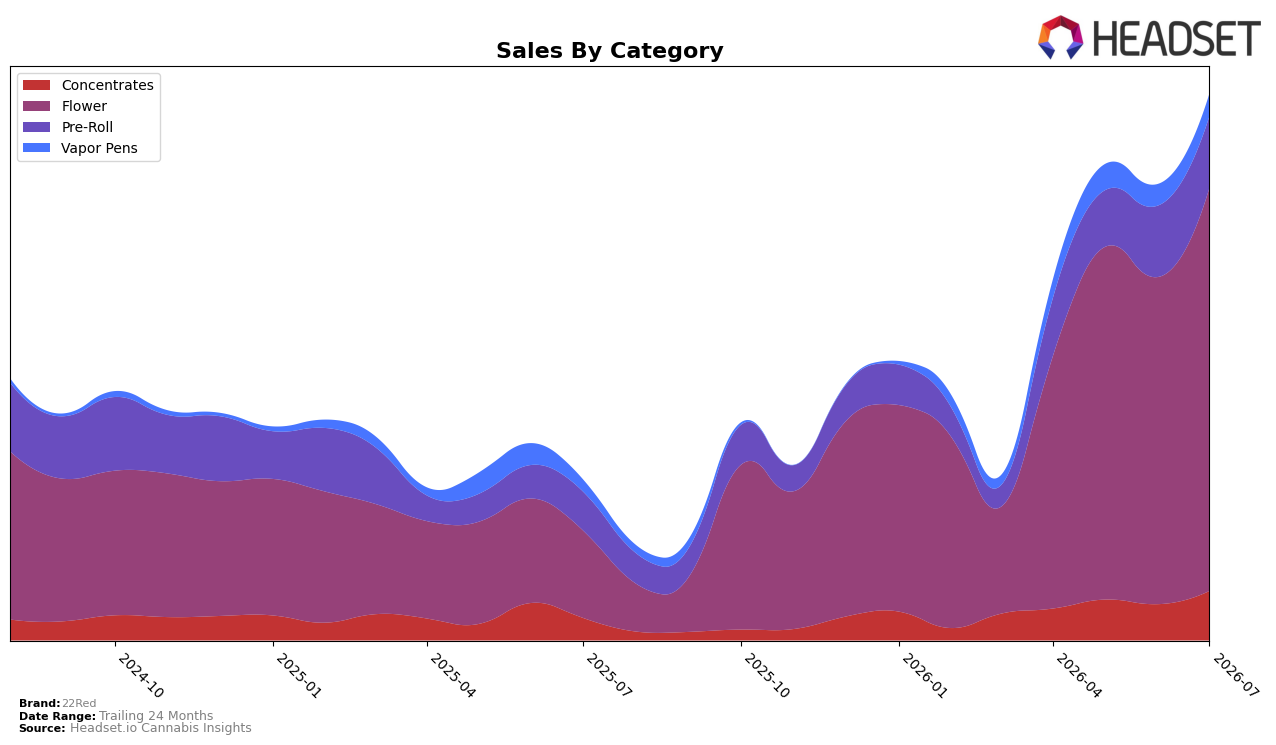

In July 2026, 22Red’s category mix concentrated heavily in Flower at 73.56% share with year-over-year growth of 359.97% and month-over-month expansion of 23.17%, while Pre-Roll held 13.14% share with 83.62% YoY and 0.35% MoM, and Concentrates accounted for 9.10% share with 118.14% YoY and 36.03% MoM; Vapor Pens rounded out the mix at 4.20% share with 83.61% YoY and 4.76% MoM. Average price rose 13.02% YoY to $20.32 even as the top state Arizona anchored a Flower-led profile and the brand ranked 8 in Flower, implying that scale is being driven by higher-priced Flower (average item $34.44) alongside measured Pre-Roll stability, and that July 2026 momentum hinges on sustaining double-digit MoM gains in Flower and Concentrates.

The shift toward Flower’s 73.56% share combined with Concentrates’ 36.03% MoM surge and Pre-Roll’s flat 0.35% MoM indicates a portfolio tilting toward potency-forward and basket-size-accretive formats rather than volume-chasing multipacks, which supports price elevation and trade-up behavior. With rank 8 in Arizona Flower and total brand sales up 237.77% YoY, the mix suggests 22Red’s defensible positioning is to lean into premium Flower while using Concentrates’ triple-digit 118.14% YoY to buffer cyclical dips, implying a strategy to prioritize depth in Flower and selective assortment in Pre-Roll/Vapor Pens to maintain share without diluting price.

Competitive Landscape

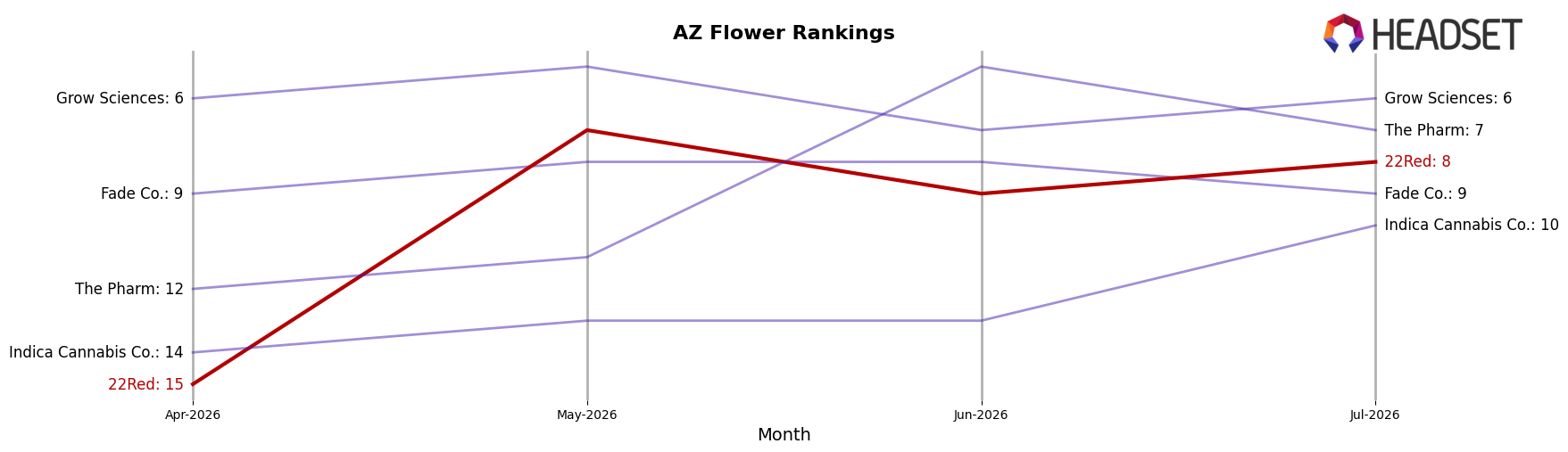

22Red sits at rank #8 in AZ Flower in July 2026 after climbing 22 positions year over year from #30, while also improving 7 spots from April 2026’s #15 and briefly peaking at #7 in May 2026; in contrast, Just Flower holds #1 with a +21.8% YoY sales gain and Fenix is at #5 with a -6.9% YoY sales decline, indicating 22Red’s recent ascent is occurring alongside both expanding and contracting rivals. This upward compression from #30 to #8 within twelve months and from #15 to #8 over three months implies 22Red is transitioning from mid-pack volatility toward a stable top-10 foothold if it sustains momentum against leaders.

Notable Products

Gelato 41 (14g) delivered the standout movement in July 2026 with a 253.7% month-over-month surge to rank 5, while BCC x Jealousy (3.5g) slid 17.0% to rank 3. Mr. Jack Pre-Roll (1g) advanced 46.3% to rank 2, and BCC x Jealousy Pre-Roll (1g) held rank 1 with a 22.0% lift. Four of the top ten are Flower SKUs and four are Pre-Rolls, and that split alongside the outsized 14g gains implies a pivot toward larger-pack Flower driving basket consolidation over single-stick velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.