Apr-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

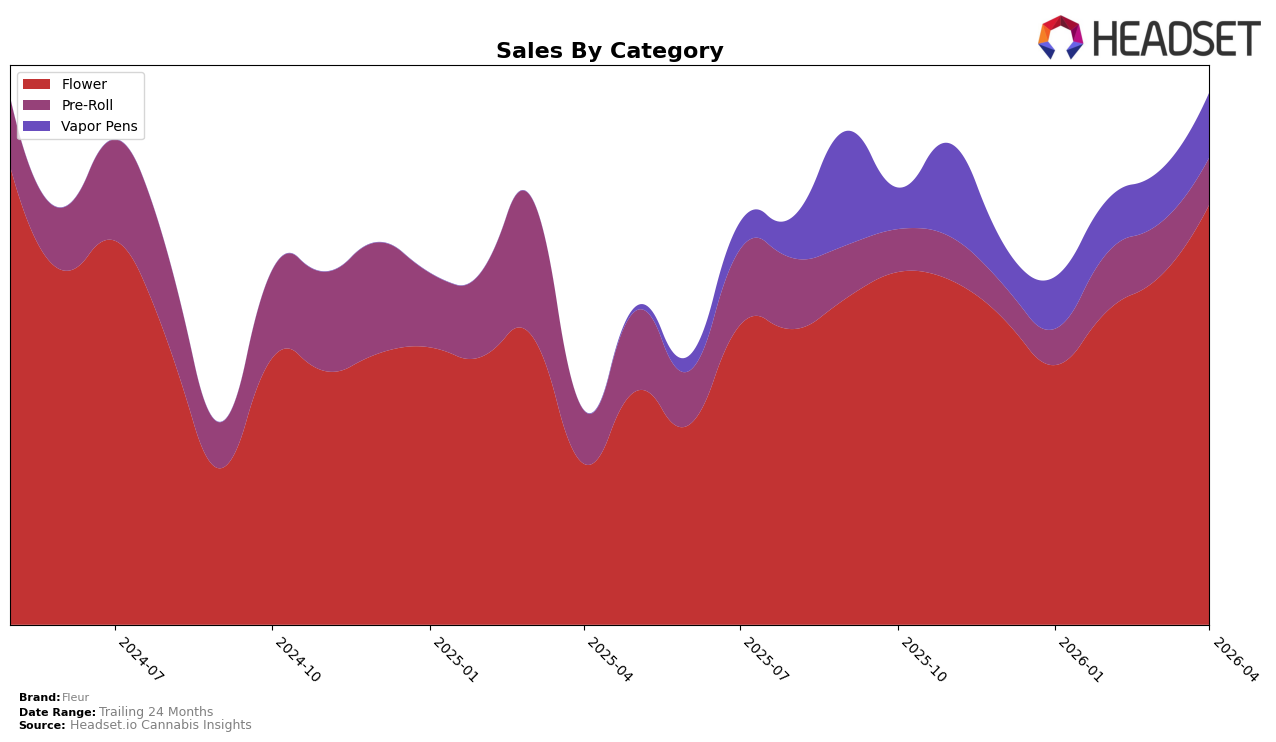

Fleur has shown a notable upward trajectory in the Nevada market, particularly within the Flower category. Starting the year outside the top 30, Fleur managed to climb to the 29th position by April 2026. This rise is indicative of a positive momentum, as evidenced by the increase in sales from January to April. However, in the Pre-Roll category, Fleur's performance has been less consistent, fluctuating between ranks 45 and 58, and remaining outside the top 30 throughout the first four months of the year. This suggests that while Fleur is gaining traction in Flower, it might need to strategize differently for Pre-Rolls to capture a larger market share.

In the Vapor Pens category, Fleur has maintained a steady presence, hovering around the 50th position in Nevada. While this consistency indicates a stable foothold, it also highlights the challenge Fleur faces in breaking into the top 30. The slight improvement in sales from March to April may signal the beginning of a positive trend, but it remains to be seen if this will translate into a higher ranking. For those interested in the nuances of Fleur's market strategies and potential areas for growth, further analysis would be beneficial.

Competitive Landscape

In the Nevada flower category, Fleur has shown a promising upward trajectory in its rankings over the first four months of 2026. Starting from a rank of 42 in January, Fleur improved its position to 29 by April. This positive trend is reflected in its sales, which have steadily increased each month, culminating in a notable rise by April. In contrast, Polaris MMJ experienced a decline in rank, dropping out of the top 20 by March, which coincides with a significant decrease in sales. Meanwhile, Safety Meeting made a remarkable leap from rank 44 in January to 26 in April, with a corresponding surge in sales, indicating a strong competitive presence. High Heads maintained a relatively stable position but saw a slight dip in April, while Range demonstrated a significant improvement, climbing from rank 64 in January to 27 in April. Fleur's consistent improvement in rank and sales amidst these competitive dynamics highlights its growing influence in the Nevada flower market.

Notable Products

In April 2026, Fleur's top-performing product was Bushido OG (3.5g) in the Flower category, maintaining its number one rank consistently from January through April, with a notable sales figure of 2511. Pixie Stick (3.5g) also in the Flower category, held the second position, demonstrating a recovery from a dip in February to regain its spot from March. Grape Monster (3.5g) secured the third rank, showing consistent performance since February. Grape Monster Pre-Roll (1g) achieved the fourth rank, marking its return to the top ranks after being absent in March. Tiger Head (3.5g), a new entrant, debuted at the fifth position, indicating a promising start.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.