May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

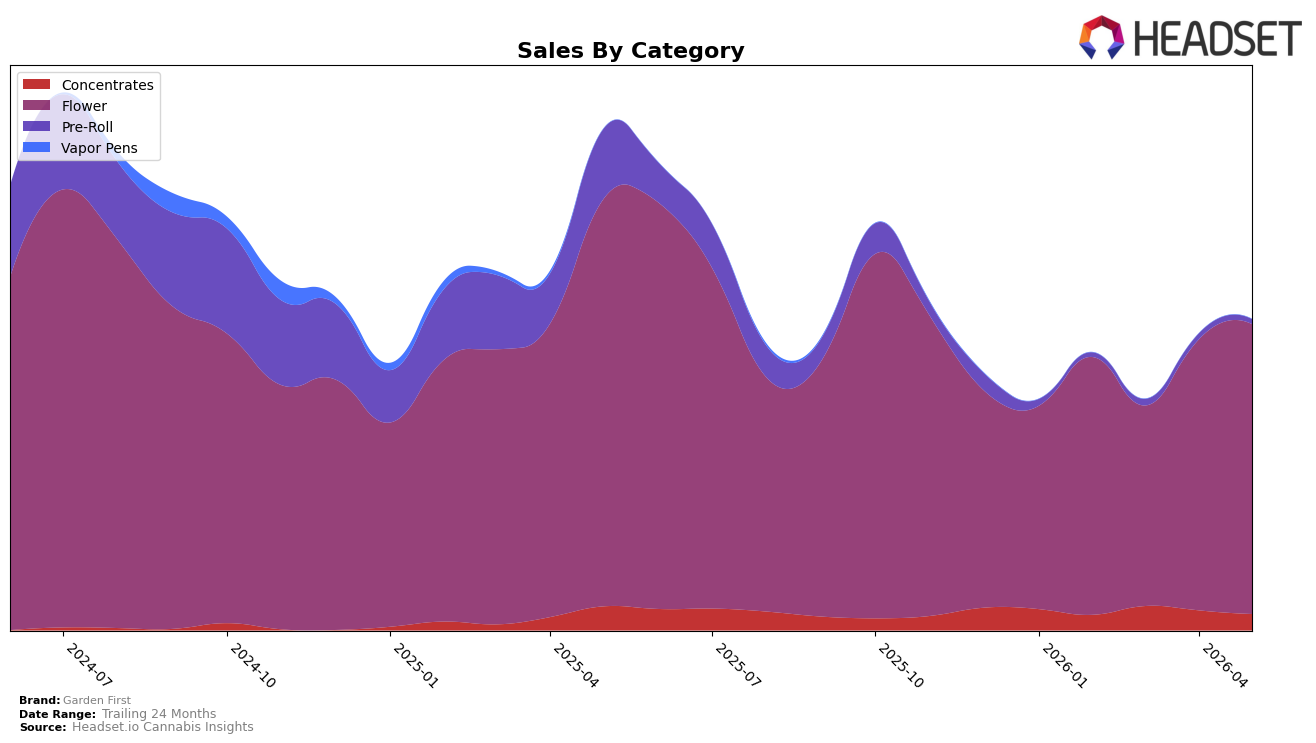

In May 2026, Garden First concentrated 93.31% of sales in Flower, where category sales were down 28.86% year over year but up 7.07% month over month, while Concentrates held 5.20% share with a 32.13% YoY decline and an 18.53% MoM drop. Pre-Roll shrank to 1.49% share after a 93.40% YoY fall and an 18.64% MoM decline, pushing overall brand sales down 38.04% YoY even as the brand’s average price rose 2.70% YoY; within Flower, the average price sat at $14.49. Garden First’s rank at 25th in Flower in Oregon indicates reliance on a single category for visibility, with the MoM lift in Flower partially offsetting sharper MoM pullbacks in Concentrates and Pre-Roll, implying short-term stabilization depends on sustaining Flower’s recent MoM momentum while arresting mix erosion elsewhere.

The shift toward a heavier Flower mix alongside a 7.07% MoM rebound, contrasted with double‑digit MoM declines of 18.53% in Concentrates and 18.64% in Pre-Roll, implies Garden First is trading depth for breadth, prioritizing a category where it holds a 25th rank but risking incremental reach loss in smaller formats. With category-level YoY contractions of 28.86% in Flower and 32.13% in Concentrates contributing to a 38.04% YoY brand decline, the 2.70% YoY increase in average price suggests pricing held as volumes contracted, which may support margin but tightens elasticity headroom; the implication is that near-term positioning hinges on reinforcing Flower velocity while selectively rebuilding presence in Concentrates to prevent further share concentration risk.

Competitive Landscape

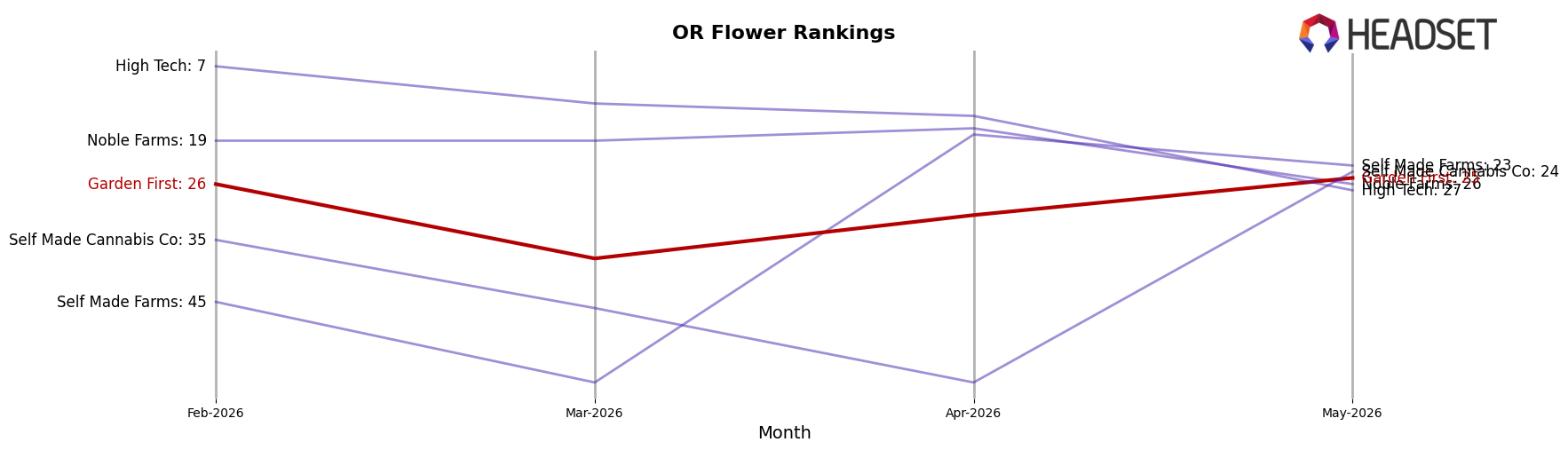

Garden First sits at rank #25 in OR Flower in May 2026, down 7 positions year over year from #18, while its 3-month position at #26 indicates only a 1-rank improvement into May; by contrast, Grown Rogue moved up from #7 to #2 as sales grew 51.1% year over year and Otis Garden climbed from #20 to #5 with 101.4% YoY sales growth. The brand’s peak at #15 in July 2024 versus the current #25 in May 2026, alongside Bald Peak holding near the top despite a 12.6% YoY sales decline at #3 and PRUF Cultivar / PRŪF Cultivar steady at #1 with 23.9% YoY growth, implies Garden First is being outpaced at the point of sale and must regain share in a tier where upward mobility is happening quickly.

Notable Products

Gelato Cake (1g) posted the largest month-over-month surge at +133.7%, while Lime Dawg (Bulk) climbed +61.7% and reached rank 7, indicating momentum in both single-gram and bulk formats. In contrast, Golden Goat (Bulk) fell -77.5% to rank 3, and Classic Watermelon Haze (1g) slid -1.9% yet held rank 1, suggesting a reshuffle within the top tier. Four of the top ten are Flower SKUs, including two bulk entries among the top nine and a pre-roll presence at rank 5, pointing to a tilt toward bulk-led basket building with selective trial via pre-rolls. The mix implies Garden First is leaning into replenishment-driven bulk and high-velocity 1g Flower to anchor share while culling weaker bulk strains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.