Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Gold Rush (MO) is stocked at 13 licensed dispensaries across Missouri, Oklahoma, and Mississippi, 8 of them in Missouri, with the deepest coverage in Cassville, Kansas City, Maryland Heights, O'Fallon, and Riverside. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

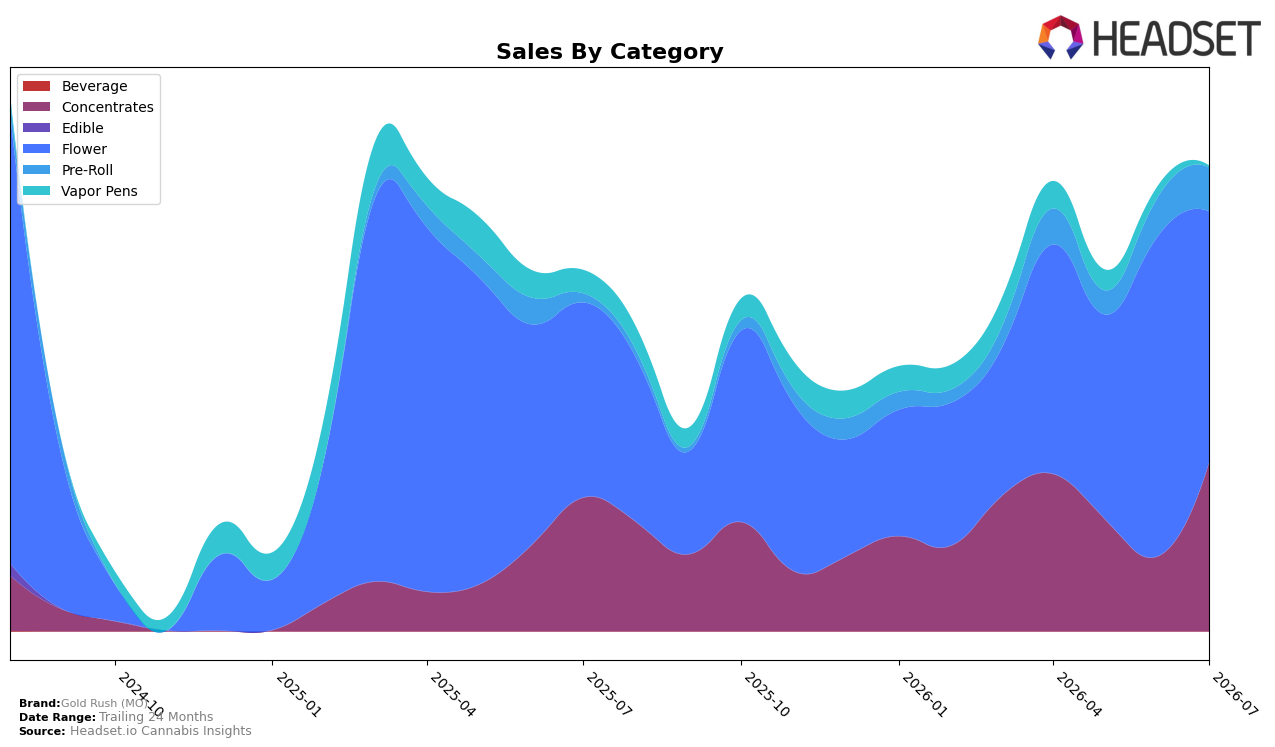

Gold Rush (MO) concentrated over half of July 2026 sales in Flower at 54.03% share, with Flower up 28.84% year over year but down 21.47% month over month, while Concentrates reached 36.26% share on 26.31% YoY growth and a 125.73% MoM surge; meanwhile, Pre-Roll expanded to 9.39% share with 393.82% YoY and 12.88% MoM gains as Vapor Pens slid to 0.32% share on a 93.58% YoY and 86.64% MoM decline. Despite an overall brand sales YoY increase of 28.99% and an average price drop of 33.34% to $24.51, the mix indicates substitution away from Vapor Pens and a reweighting toward Concentrates and Pre-Roll, implying price-led volume capture while Flower retrenched month over month.

These shifts position Gold Rush (MO) to lean into value-oriented inhalables, with Concentrates’ 125.73% MoM jump and Pre-Roll’s 9.39% share suggesting basket entry and trade-down dynamics, while Flower’s 21.47% MoM pullback alongside a 28.84% YoY gain points to episodic volatility rather than category exit. Holding the number 45 rank in Flower in Missouri and concentrating 90.29% of sales across Flower and Concentrates, the brand is tilting toward formats that can defend share via lower price points and promotional elasticity, implying that sustained growth will come from reinforcing Concentrates and Pre-Roll while stabilizing Flower to prevent rank leakage.

Competitive Landscape

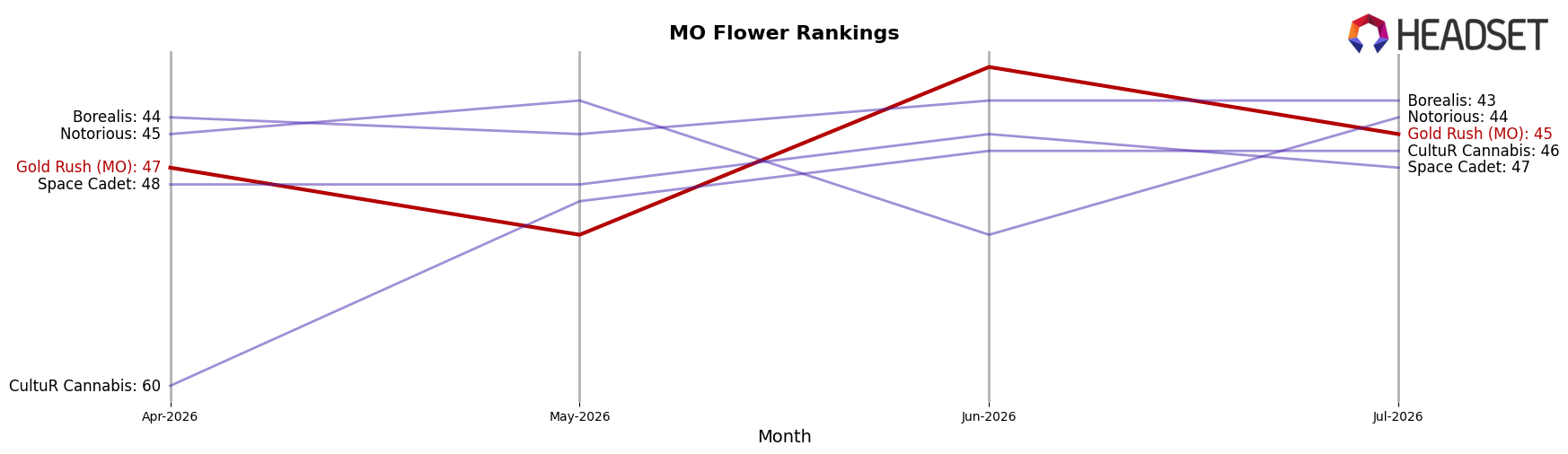

Gold Rush (MO) sits at rank #45 in MO Flower for July 2026, improving 7 positions from #52 year over year, while slipping 2 spots from #47 in April 2026; the brand remains 9 places below its peak at #36 from August 2024. In the same period, Flora Farms held #1 with a -1.3% YoY sales change and Sinse Cannabis advanced from #4 to #2 with +9.0% YoY sales growth, indicating competitors are consolidating share even as top-tier growth slows. This mix of a 7-rank YoY climb alongside a 2-rank recent dip implies Gold Rush (MO) is recovering structurally but must address short-term slippage to sustain upward mobility in a tier where leaders are either holding (#1) or rising (#4 to #2).

Notable Products

With no month-over-month swings above +50% or below -10% in July 2026, the most directional movement is incremental: Apples and Bananas Pre-Roll (1g) inched up +5.2% to rank 7 while King Cherry Sugar Wax (1g) slipped -3.7% at rank 10, implying stability rather than volatility. The top three ranks are all Pre-Roll SKUs at positions 1, 2, and 3, and with a fourth Pre-Roll at rank 7 this concentration suggests a pre-roll-led traffic strategy even as Concentrates occupy ranks 4, 5, 9, and 10. Flower maintains mid-pack presence at ranks 6 and 8, with King Cherry #10 (7g) up +8.1% and Banana Foster (7g) anchoring volume near the middle, indicating balanced basket roles across formats. The pattern implies Gold Rush (MO) is leaning into Pre-Roll visibility for share capture while using Concentrates and 7g Flower to preserve ticket size and mitigate category risk.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.